In a relatively short timeframe, shopping for a banking provider or banking product has gone from something largely based on physical location to a digitally-driven process. While human relationships are still influential in the buying process, consumers today research an average of nine different sources of information over a 60-90 day period when shopping for a financial product, according to the Digital Growth Institute.

As branch banking has given way to online and mobile banking, consumers must now wade through a surplus of choices — many of them related to the emergence of digital disruptors in the banking space. With higher expectations, much room has been left for disappointment when consumers compare the innovative experiences of startups with those of most traditional providers.

Desperate to catch up, financial brands end up pumping tons of money into paid media campaigns and referral programs in hopes of filling the sales funnel. But with a limited number of net new prospects in the market, this tactic has become exceedingly expensive, costing larger banks upwards of $2,000 for a single customer, as reported by Tearsheet.

Under increasing pressure to grow revenue, how can financial institutions win over consumers without having acquisition costs continue to snowball?

Marrying Customer Acquisition With Personalization

While keeping customer acquisition cost (CAC) units low may not be feasible for most financial services providers, especially the larger ones, there is much that can be done pre- and post-click, to optimize the experience for a user. An analysis by Boston Consulting Group found the impact of personalization to be significant in improving marketing efficiencies within banking, generating as much as $50 million in revenue for retail banks, alone, by tailoring things such as product offers and pricing.

That figure may just scratch the surface, as there are many other strategies that can be used to lift engagement and maximize results. Below are five examples bank and credit union marketers should consider.

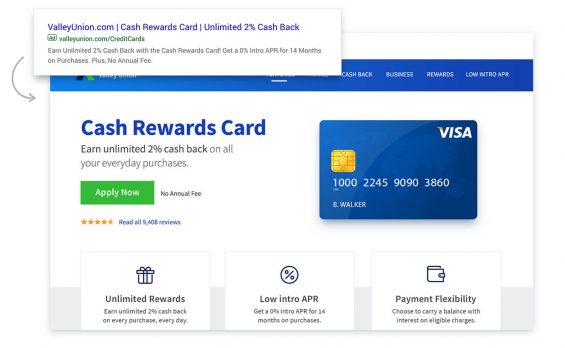

1. Match Landing Page Messaging With Ad Copy

Akin to a consumer receiving a print offer to redeem at their local bank only to be met by branch representatives lacking information or context, serving ad copy inconsistent with the landing page experience is one of the quickest ways to deter conversions.

Continuity is crucial during the initial moments in a relationship with a prospective customer, so marketers need to ensure when an individual arrives at a site from an affiliate link or is referred via a certain marketing campaign — the next interaction corresponds accordingly, as illustrated below.

URL parameters and campaign data can be leveraged to identify the original advertisement served to the user in order to match the appropriate landing page messaging in real time.

Read More:

- For Impact, Banking Emails Grow More Targeted and More Creative

- 4 Digital Challenges Financial Marketers Must Overcome Immediately

- Personalization in Banking Can’t Be Disguised as Cross-Selling

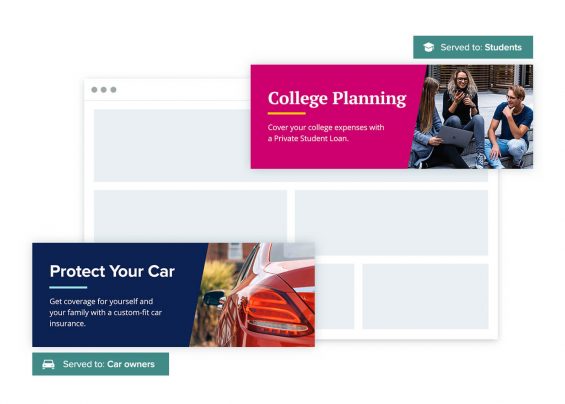

2. Change The Landing Page Experience For Different Segments

The more a landing page connects with consumers, the more likely it is to convert. Finance marketers, therefore, need to reconsider how often generic experiences make their way into new campaigns. Catchall landing pages may be easier to implement, but usually end up generating lower-yielding results, wasting valuable media spend and time.

Instead, all available data should be leveraged to establish buyer personas, from which unique landing pages can then be served and optimized per audience. Here is a simulated landing page showing how a banner experience can be personalized for two audience segments.

Beyond basic demographics, the consumers’ location, weather, device type, affinities, and more, can all be used to segment new and anonymous users. Once known, more behavioral insights such as browsing history and interest displayed in certain products or services can be layered in.

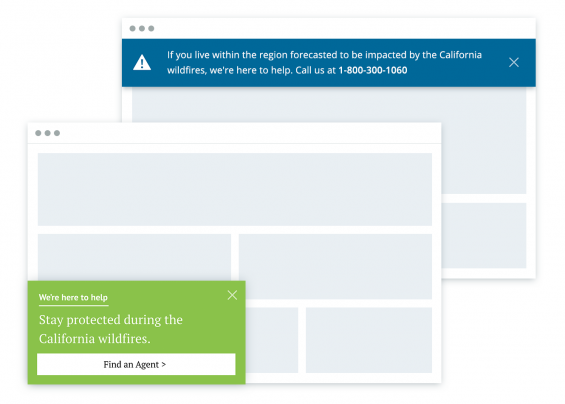

3. Test The Best Way to Frame An Offer

Banking brands will never know what works best for a target audience unless they A/B test different elements of an offer. From language to design, calls-to-action, and even the format (overlay vs on-page banner vs notification, etc.), continuous testing and iteration is key to presenting the right message in the right context or to the right cohort.

Multiple variations can be served simultaneously to determine the best combinations according to specific objectives, whether it be to increase applications, deposit growth, or wallet share. No single variation can resonate with all users, meaning long-term acquisition success relies heavily on experimentation. Below is a simple illustration of to calls to action with for the same theme — insurance in this case.

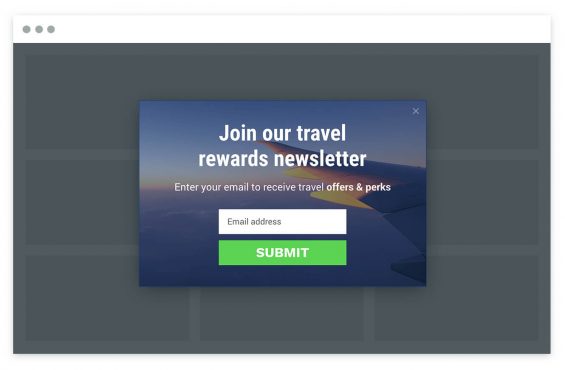

4. Move The Email Capture Higher Up The Funnel

An email address is one of the most valuable pieces of data a bank or credit union can obtain from a consumer. With it, a door opens to continue developing the relationship long after the individual has left the site. It is also critical to their identification across channels, devices, and even physical locations.

By introducing the email signup experience earlier in the consumer journey, financial marketers can accelerate the speed by which they are able to deliver more highly-personalized interactions. Much like offers and promotions, these should be battle tested to determine what works for particular subsets of visitors — some may convert more quickly out of immediacy and need, while others need a bit more incentivizing to encourage sharing their contact info.

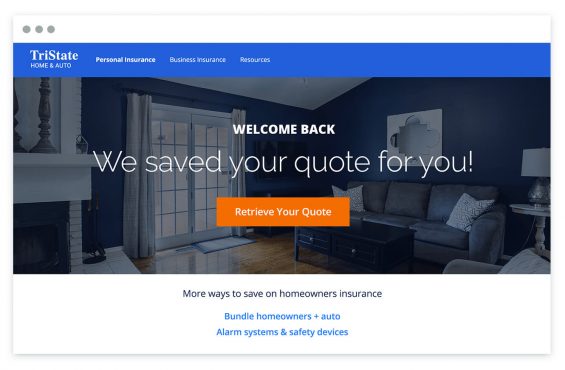

5. Bring The User Back to Context

Given how much research consumers commit to when shopping for a financial product or service, most aren’t likely to make a decision on their first visit. This means financial marketers can and should expect a high degree of site abandonment during the initial steps of the decision process. With articles, recommendations, reviews, and terms to weigh, prospects will be in a haze of information, providing the perfect opportunity to offer relief.

Using data collected from previous interactions and browsing history, prospects can be brought back into context via triggered emails or personalized messages directing them to pick up where they left off — a service in and of itself. Remembering the key benefits associated with a particular product or promotion, consumers will be one step closer to sealing the deal.

Personalization’s Gift to The Top of The Funnel

Customer acquisition cost is dependent on more than just a financial institution’s efforts to bring users into the sales funnel, it’s about how well they convert upon arrival. By optimizing the on-site experience, marketers can achieve greater results and value from their campaigns, acquire customers at the lowest overall cost while remaining ROI positive, and reinvest the money earned back into revenue-generating initiatives.