Anyone who’s ever struggled to lay their hands on cash or a card while sitting behind the wheel of a car at a McDonald’s drive-up window will appreciate this: In Brazil, drive-up customers can simply say: “I’m paying with Sem Parar,” when they finish ordering. “Sem Parar” (it means “nonstop” in Portuguese) is the Brazilian electronic toll-pass system. McDonalds partnered with payment systems vendor Fleetcor to use the toll-pass system as the means for consumers to pay by voice.

Voice pay is just one of two transformative developments rolling through the payments world. The other trend that’s opening big potential opportunities for retail banking providers is the suddenly awakened U.S. contactless card market. The contactless trend is happening now, while voice pay is a little further down the road. But both are important for the development of the retail payments business.

Voice Pay: Can You Hear Me Now?

If you had any doubts as to whether smart speakers such as Amazon’s Echo and Google Home are a passing fad, new data from NPR and Edison Research should sweep them away. The organizations revealed that the number of smart speakers in U.S. households grew by 78% to 118.5 million devices in one year — from December 2017 to December 2018. Of the 14 million U.S. consumers who bought one during the 2018 holiday season, just over half were adding the device to one or more existing smart speakers.

The research also uncovered that one out of three smart speaker owners use the device several times a day and one out of four use it “nearly every day” (music remains the chief use at this point). Interestingly, 16% admit they never use it.

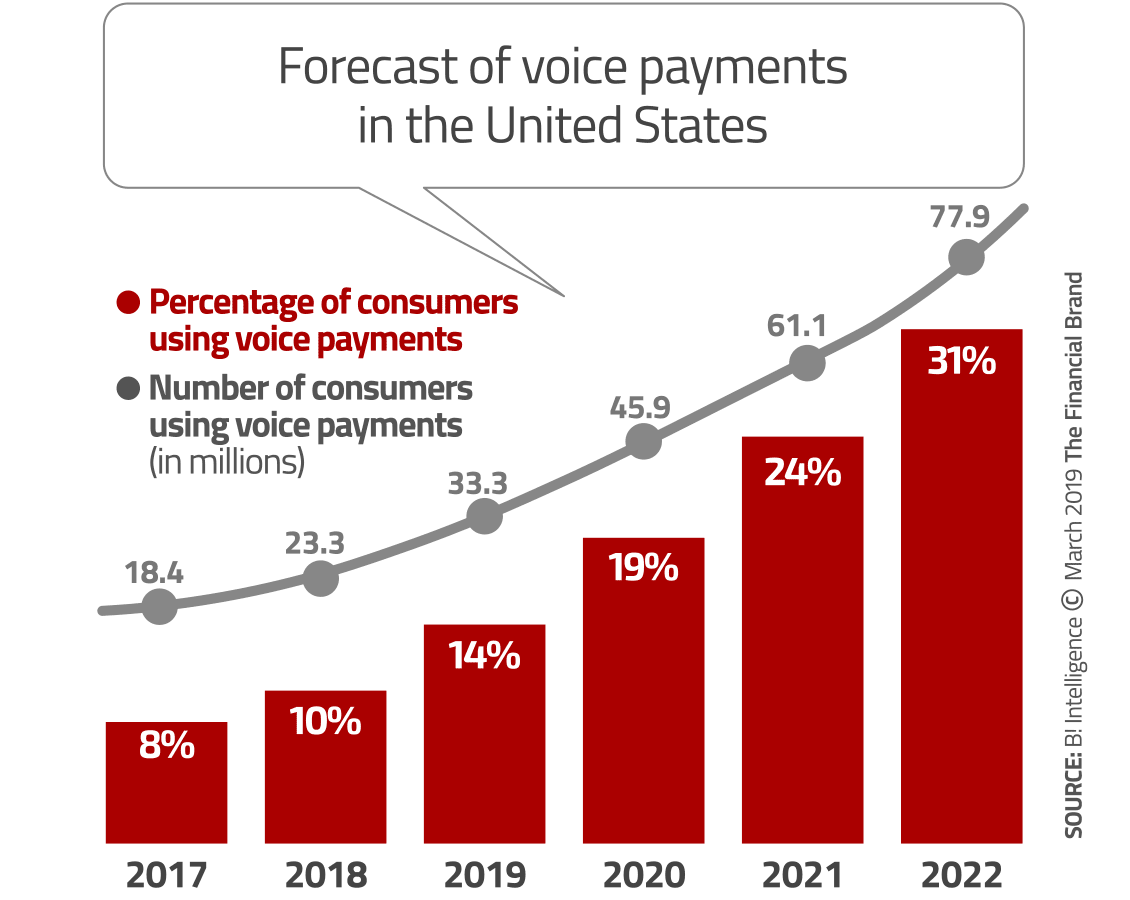

Smart speakers already are being used for payments. As Business Insider notes, Siri can help users make P2P transfers with Venmo, Alexa can pay off Capital One credit cards bills, and Google Assistant can let users shop with their voice from nearby stores. BI predicts that usage of voice payments in the U.S. will grow from 18.4 million users (8% of the U.S. adult population) in 2017 to an estimated 77.9 million users (31%) by 2022.

Juniper predicts Internet of Things (IoT) payments — which includes voice payments — will grow 75% a year from $24.5 billion in 2018 to $410 billion in 2023. Even though the research firm expects 80% of those transactions to be made using smartphones or tablets, that leaves 20% for voice-powered devices including smart speakers and in-vehicle payments.

Based on such anticipated growth, it’s clear why megabanks including Bank of America, Capital One, and USAA among others have been rolling out conversational interfaces.

Contactless Cards: What’s Old Is New Again

The slow adoption rate of mobile wallets like Apple Pay and Google Pay has opened the door wide for a product that the wallets were supposed to make obsolete: plastic cards.

Not just your basic chip/swipe card, however, but contactless cards that, ironically, use the same near-field communication (NFC) technology used by most mobile wallets.

Contactless cards are dominant outside the U.S., comprising 40% of face-to-face transactions in the U.K., Europe and Canada, and 50% in some markets, according to Auriemma Group. In the U.S., early efforts at contactless cards failed to catch on, and the technology (as used in cards) remained practically dormant.

Contactless cards, often referred to by issuers as “tap-and-go” or “tap-and-pay,” typically are used for small, everyday transactions such as coffee and fast food. One reason they’ve proven so popular around the world — and likely will in the U.S. once they’re in consumers’ hands — is ease of use. Consumers needn’t hand over their card, or swipe or dip it. Just tapping the payment terminal or placing the card within one to two inches of it gets it done.

Contactless card transaction times run about two seconds, compared with chip cards that can take up to 10 seconds to process. Better than when first rolled out, but still long. Consumers have gotten used to the lag time, now, but once they’ve experienced two-second payments, they won’t look back, many observers believe.

Auriemma analysts caution that many consumers are unfamiliar with the technology and may be turned off if their first attempt fails. Therefore, consumer education is key.

What’s Driving The Rise in Tap-And-Pay Card Interest

Visa CEO Alfred Kelly, Jr., predicts that up to 100 million contactless Visa cards could be issued by U.S. member banks in 2019. JPMorgan Chase, the number one credit card issuer in the U.S., announced that all Chase credit cards will have contactless functionality by the first half of 2019, with its debit cards to follow in the second half. New Chase customers are receiving NFC-enabled cards, as are existing cardholders when their cards are up for renewal.

Another impetus for contactless cards is that transit systems are adopting them for fare payments. New York City’s transit system, with millions of daily riders, will begin using the cards in 2019. In addition, the U.S. Payments Forum reports that active NFC-enabled terminals have reached nearly 20% penetration in U.S. merchants, and that the pace of adoption is increasing.

Bloomberg reports that 30% of the top 100 merchants, including Walmart, don’t accept contactless payments. However many large chains have embraced the technology including McDonald’s, Starbucks, Subway, Trader Joe’s, Walgreens, and Whole Foods.

Visa CEO Alfred Kelly says more than half of in-store payments made on Costco’s cobranded Citi Visa card were contactless within months of when the capability was enabled in August 2018.

Mastercard says it has agreements with bank partners that will bring contactless cards to two-thirds of its customers with two years, according to The Financial Times. In addition to Chase, Capital One and American Express are also issuing contactless cards, Bloomberg reports.

Even though contactless cards are more expensive to issue than EMV chip cards, according to Auriemma, these tap-and-pay cards could be a big plus for bank and credit card issuers. A.T. Kearney estimates in a report that U.S. banks could generate $2.4 billion in incremental card-related profit by transitioning to contactless cards, and could eliminate $22.2 billion worth of mainly cash-handling expenses, as the cards further reduce the use of cash.