In response to the pressing needs of cutting costs, improving monetization of services and increasing their retail banking customer base, JPMorgan Chase is building an entirely new digital banking organization. As consumers shift their banking preferences to online and mobile solutions (even if they are offered by non-bank technology firms), Chase wants to be the digital bank of preference — especially for millennials.

According to a 111-page Chase strategic report and a 33-page in-depth analysis from CB Insights, this focus on “Mobile First, Digital Everything” is having positive results. Over the past three years, Chase has grown their active digital customer base by ten million customers to 48 million total and their active mobile customer base also by ten million customers to 32 million total. They are also embracing a banking ecosystem strategy, where a vast array of products and services are offered across various platforms with low (or no) fees.

A Digital Banking Ecosystem

To support the objective of being the largest digital bank, Chase is focusing on building a new digital banking ecosystem that supports all of their product and service offerings and is positioned to compete more effectively in the future. The foundation of this digital journey was to improve the new account opening process so that a branch visit was no longer needed.

This is a major step forward in a competitive landscape that offers few traditional institutions that support an end-to-end digital account opening process. According to the 74-page report 2017 Account Opening and Onboarding Benchmarking Study, published by the Digital Banking Report, less than 25% of institutions offer this mobile capability. Chase executives mention that the new account opening process, while taking less than four minutes, still has more friction than they prefer, and that future improvements will be made.

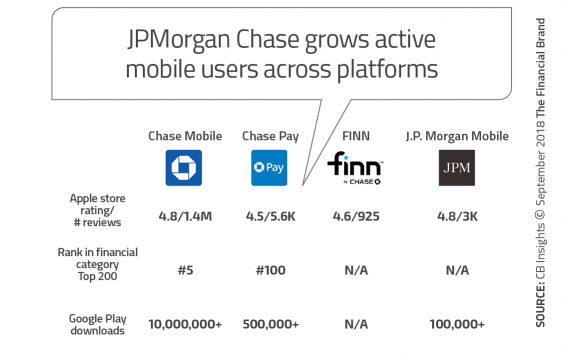

Unlike many financial institutions, Chase offers multiple mobile banking apps for consumers. These include Chase Mobile, Finn, and JPMorgan Mobile, all of which appeal to different customer segments. ChasePay is also highly popular with consumers wanting to make payments with their phone.

Read More: How Chase Bank is Tackling Top Digital & Mobile Challenges

Chase Mobile is similar to most financial institution’s mobile banking app, allowing consumers to make deposits, initiate payments, and monitor accounts on a mobile phone. New functionality for Chase Mobile includes the ability to make cardless ATM transactions using a mobile device and text banking.

Finn is Chase’s mobile-only bank that was developed to target millennials, as well as consumers who don’t live close to a Chase branch. It is run separately from the rest of the bank, and is in response to the fintech digital solutions being introduced worldwide. The completely free app includes checking, savings, budgeting capability, and a savings tool that uses artificial intelligence or pre-set transfer requests to shift money between accounts. The app also supports person-to-person payments, bill pay and an option to “send a check” after being digitally authorized.

JPM Mobile is a digital wealth management app that enables clients to monitor portfolios, manage balances, and access business news. Similar to Chase Mobile, the app is meant to serve the most wealthy of Chase’s client base with a focus on investment portfolio management.

ChasePay is the bank’s digital wallet. As opposed to making payments the way Apple Pay, Venmo or Zelle do, ChasePay uses QR-codes to make payments with Chase a credit card, debit card, or prepaid card. While this type of payment app is relatively uncommon in the U.S., it mirrors what is gaining vast acceptance overseas, especially in China.

Beyond traditional banking products, Chase has also partnered with outside providers to offer digital solutions in other product categories:

- Chase Business Quick Capital – Powered by OnDeck

- Chase Digital Mortgage – Powered by Roostify

- Chase Auto Direct – Powered by TrueCar

Read More: 7 Essentials of Digital Banking Transformation Success

Why Digital Matters

The rationale for investing in digital is covered in the 111-page Chase strategic report. The report references Deloitte research findings that 57% of millennials would change their financial institution for a better tech platform, while 65% of customers would leave a financial institution if the digital channels are not integrated. They report also references Novantas research showing that “digital convenience” has become more important than “locational convenience.”

Other reasons mentioned by Chase for why digital matters include:

- Higher Net Promoter Score (+19%)

- Higher retention rates (+10ppts)

- Higher card spend (+118%)

- Higher deposit and investment share of wallet (+40%)

- Improved efficiencies

Payments Everywhere, with Massive Reward Points

Investing in their payment network for more than a decade, Chase has unequaled reach in the marketplace, with merchant partnerships, payment service acquisitions, differentiated product offers, co-brand partnerships and the highest volume real-time payment network with Zelle and Chase QuickPay.

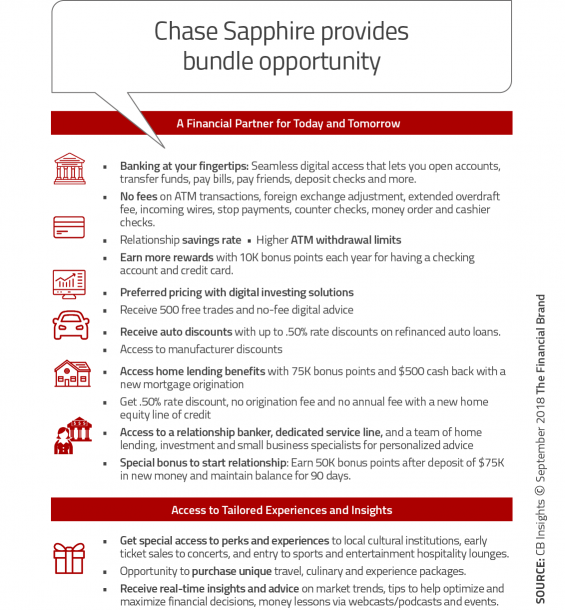

The result has been a 75% active payments user rate, 48 million cardholder base, more than 50% of Zelle transactions, greater than 70% mobile wallet integration and a 22% credit card market share. Much of this growth has occurred due to unique rewards and the growing Sapphire brand.

With Chase Sapphire consumers pay one of two annual fees (Preferred $95, Reserve $450), and receive credit card rewards and access to the Chase Sapphire club. As an ongoing strategy, Chase leverages its credit card business as a starting point for expanded account penetration. Similar to Amazon Prime, the bank plans to expand this network and provide members with free financial products and services.

According to CB Insights, Chase offered a 100,000-point sign-up bonus for its Chase Sapphire credit card which resulted in thousands of new customers. While the bank incurred a $200,000 loss because of the promotion, it was considered a success in generating lifetime Sapphire Rewards customers.

Points are an ongoing currency that Chase can leverage to expand relationships and encourage positive activity. According to Chase, the Sapphire product has a greater than 90% renewal rate, with the potential to support an ecosystem beyond financial services.

The Branch is Not Dead at Chase

Despite a commitment to a “digital everything” strategy, Chase continues to build branches. With a nationwide footprint, Chase is focused on building branches to fill in their current distribution and replace current branches.

Chase has indicated that they will open 400 new branch locations over the next five years. With over 5,000 retail branches currently, Chase’s overall network has shrunk slightly over the past few years. Part of the strategy is to serve higher net worth customers as well as providing “branch billboards” to support marketing efforts. In a way, it is the same strategy used by Whole Foods in the placement of stores in wealthy markets. According to Chase, 75% of deposit growth comes from customers who use its branches.

Read More: Sustaining Digital Banking Channels’ Explosive Growth

A Long-Term Strategy for Growth

Traditionally, financial institutions plan for performance on quarterly cycles. Chase has adopted a long-term strategy, taking the steps needed to become a more competitive digital bank. Their strategy is to build an ecosystem with products and services built internally and developed with partners.

With this strategy, Chase will be in a better position to compete on a global basis across alternative platforms and channels.