Many believe we are in the midst of a fourth industrial revolution. The first industrial revolution (18th and 19th centuries) moved us from a prominence of farming to a more industrial existence and the introduction of steam engines. The second industrial revolution (1870 – 1914) was a period of industrial expansion and mass production. The third industrial revolution (1980s – today) moved us from mechanical devices to digital technologies. The fourth industrial revolution is taking shape today, characterized by a range of new technologies such as robotics, artificial intelligence (AI), quantum computing, biotechnology, the Internet of things (IoT) and autonomous vehicles.

As we have moved from one industrial revolution to the next, we have seen business growth shift as a result. We have witnessed prominent firms upended by new players, industries gaining or decreasing in importance, and even entire nations generating exceptional growth at the expense of historical leaders.

“The banking industry has never changed as quickly as it is today, yet it will never change this slowly again.”

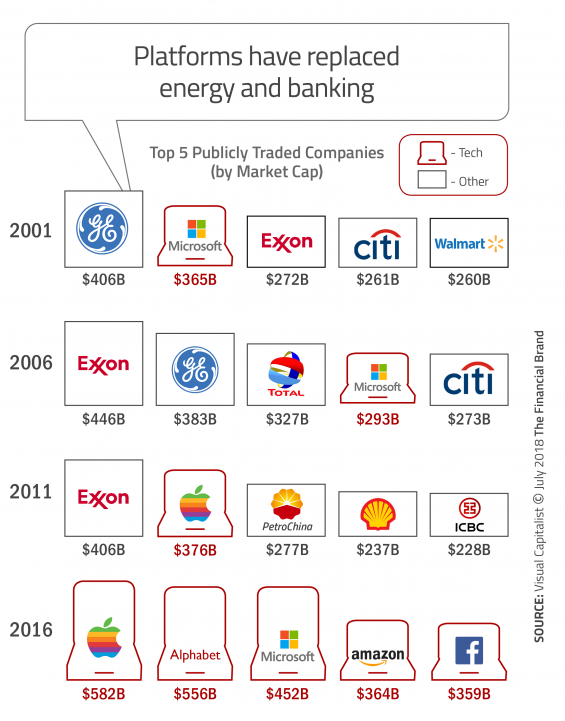

As an example, we only need to look at how the top five publicly traded companies by market capitalization have changed between 2001 and 2016. In this relatively short period of time, technology firms have completely replaced the energy and banking leaders of the past. The same type of disruption has occurred within industries.

Financial institutions of all sizes and their leaders must embrace these changes, and accept the risks that come with them. The reward for taking calculated risks takes form as both profit and success — only possible if you are part of this transformation.

In many cases, change may result in a complete disruption of the way banking organizations conduct business and the career choices we make. To better understand the change upon us, we need to understand many of the underlying factors that are causing this change.

The Emergence of Platform Players

Clearly the fourth industrial revolution is putting many traditional business models at risk. In banking, while organizations were able to perform basic functions for decades with increasingly antiquated back office systems, new digital technologies and increasing consumer expectations are making many banking models obsolete.

In response to the changing marketplace, many new players have entered the competitive battlefield and new ecosystems are emerging. The most important change across all industries is the power of platform players such as Google, Amazon, Facebook and Apple and the ‘platformification’ of industries. According to Praxent, these platforms all have the same elements in common:

- They are information enabled, with data and advanced analytics improving personalization and contextual awareness and increasing customer value.

- They leverage outside talents and assets, without the need to own assets as much as the ability to deliver best-in-class solutions to customers.

- They benefit from social sharing and feedback, creating communities of like users and engagement beyond transactions.

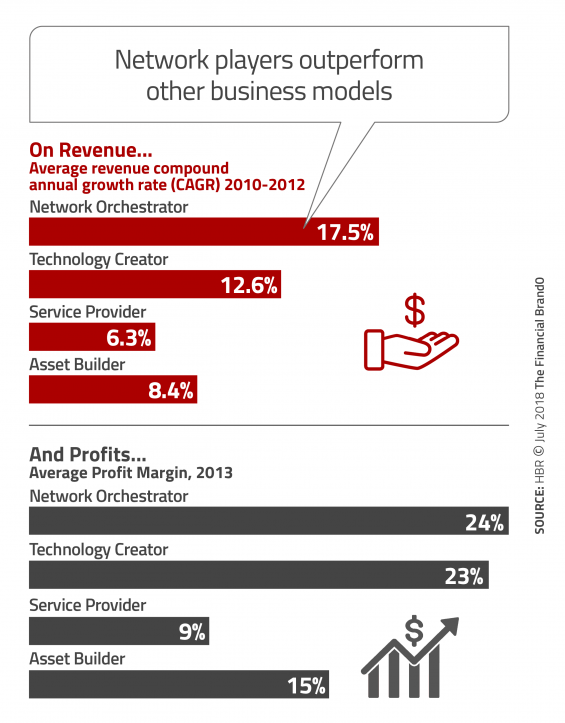

According to MIT Sloan, there is a growing connection between platform organizations and AI/machine learning, since platform organizations have shown a strong ability to innovate and to quickly learn and apply new technology. It was also found that platform organizations are typically data rich and have the talent required to successfully deploy AI and machine-learning programs.

New Options for Business Models

In response to the power of the platform structure, banking organization have several options for future growth. All involve a change in structure and focus, but all could be a way to remain relative during a period of marketplace disruption.

- Open your existing organization to external providers of services. This is already being done by most organizations who partner with firms ranging from Fiserv to Apple Pay. In the future, this model will require greater leverage of outside providers that bring best-in-class services under one roof.

- Build off of another platform. Similar to a retailer leveraging Amazon for sales, this model places an organizations products and services on a third-party platform.

- Produce your own standalone platform. While potentially too costly, this provides the dual benefit of control and exclusivity. There is still the ability to bring other solutions to the platform.

- Serve a micromarket. Serving a single segment in a way that is scaleable, this may be a retrenchment for many organizations that also requires best-in-class solutions.

A Changing Workforce

Generational differences within an organization can be both an opportunity and a threat. Most banking organizations include a combination of Baby Boomers, Gen-X employees and Millennials. The prominence and organizational positioning of any of these generations often defines the culture and ability to embrace change within an organization.

Millennials are the most diverse generation yet, having many of the skills required to transform organizations and support the new banking ecosystem. This generation also has different values, expectations, and work habits than previous generations.

“Banking providers must be willing to embrace change, take risks and disrupt themselves (repeatedly) to keep pace with marketplace changes.”

On the other end of the spectrum, while Baby Boomers may have experiences that serve an organization well, they can also hinder growth if they lack the desire to embrace change, take risks and disrupt the status quo individually and as an organization.

The future of work will reflect the reality that knowledge has overthrown capital as the most important organizational resource. It is also the resource that is currently is shortest supply due to accelerating demand for coders, analysts, etc.

A New Form of Value Creation

In a platform economy, there is a preference of providing access to solutions as opposed to actually owning all of the solutions. This can make it possible for organizations of any size to build partnerships that can create value. In some instances, this sharing network can also allow people to share resources with one another, reducing operating costs. Many firms will find this necessary to get the skills needed to better leverage data and apply advanced analytics.

The business impact of moving to a platform model goes well beyond a banking ecosystem with third-party products and solutions. Research from the MIT Initiative on the Digital Economy (IDE) showed that on average, companies that open their application program interface (API) to outside organizations see a 4% rise in market capitalization. This is a result of lower research, development and operational costs at the same time as increased sales.

A Small Bank Advantage

When open banking, platforms, sharing economy, etc. are mentioned, the conversation usually focuses on the most prominent examples, such as the biggest tech firms (GAFA), or some of the new sharing economy examples of AirBnB or Uber.

This ignores the reality that smaller firms may be better positioned to succeed than their larger counterparts. Smaller banks are already partnering with many outside providers to deliver the majority of their solutions to consumers. In addition, the personal relationships these firms have with their customers and members can make the introduction of new solutions from outside providers more seamless.

That doesn’t mean that the path to success is an easy one. First and foremost, for most small (and large) banking organizations, the existing culture will need to change. In addition, banks and credit unions of all sizes must be able to attract, develop and retain individuals who can add value to the existing organization and the new business model. This may mean hiring new people or partnering with firms that can provide the skills needed.

At the core of this transformation will be the ability to leverage consumer data. Artificial intelligence (AI) will become increasingly important, not just for major ecosystem owners like Amazon and Google, but for organizations of all sizes.

Finally, to take advantage of this significant opportunity, financial institutions must be willing to embrace change, take risks and disrupt themselves (repeatedly) to keep pace with marketplace changes. Remember, the banking industry has never changed as quickly as it is today, yet it will never change this slowly again.