As more and more consumers use digital applications to make their daily life easier, the importance of being the ‘go to’ payments solution for mobile or online payments has never been more important. Banks and credit unions must avoid a mentality of ‘build it and they will come’. Instead, ongoing product development and continuous marketing reinforcement is required to increase both usage and engagement of payment solutions.

There is no question that financial institutions are facing increasing pressure from alternative payment providers that are using their payment solutions to upend your current customer and member base. In conjunction with Comperemedia, we are providing visual examples of some of the best payment solution marketing that we have seen recently in our physical and digital mailboxes. These examples should help get the creative juices flowing, providing financial marketers ideas that positively impact payment transactions.

Marketplace Overview

Comperemedia provides excellent tools to enable financial institutions to track both market trends and strategies from financial services organizations of all sizes, including all product and service categories. Some of the recent trends notices in the digital payments space include:

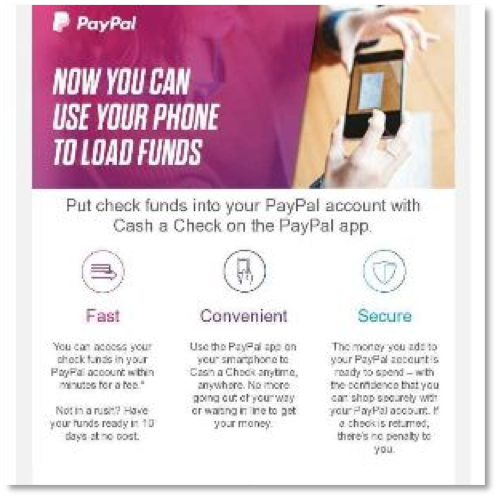

- PayPal Continues Innovation and Growth – PayPal has introduced new substitutes for traditional payment and deposit products, allowing consumers and businesses to hold funds for future purchases within the PayPal app. 40% of consumers have used PayPal as an online payment option, far more than any other provider.

- Retailers Going Solo – Major retailers are offering rewards to pay using in-house mobile wallets increasing loyalty while leaving traditional banking organizations on the sideline.

- Simplicity Messaging – Alternative solution providers are focusing on an ease & convenience message for digital payments. To compete with PayPal and other alternative solutions, banks and credit unions should embrace security as the primary benefit.

- Smaller Institutions Get Leverage – With the availability of Zelle, ApplePay and other digital payment partnership opportunities, small banks and credit unions can now use messaging similar to that of major banks.

- Personalized Messaging – Banks and credit unions should encourage adoption and usage by making incentives more personalized based on usage patterns, demographics and geography, including real-time localized offers.

- Adoption of Mobile Payments Remains Low – Despite a lot of noise within the industry, only 15% of consumers indicate they have used at least one of the three top mobile wallets.

- Security is Key to Adoption – According to Comperemedia, 43% of consumers don’t trust the security of mobile banking apps.

PayPal Moves Beyond Payments

While traditional banks are pushing for consumers to adopt their mobile payment solutions, PayPal is expanding their positioning from an online payments provider into credit cards and deposit services. Based on Comperemedia tracking, PayPal has been heavily promoting digital wallet usage over the past 12 months, inviting consumers to add accounts to their mobile wallets for in-store and in-app purchases.

With this capability, a PayPal customer can transfer and deposit funds, make purchases, and maintain a balance online with the platform (similar to what is offered by Starbucks, Amazon, etc.). This ‘walled garden’ minimize the user’s exposure to potential fraud, leaving a traditional bank out of the loop entirely.

I covered this phenomenon and how it has completely changed my perspective on who is my primary small business financial institution in this article.

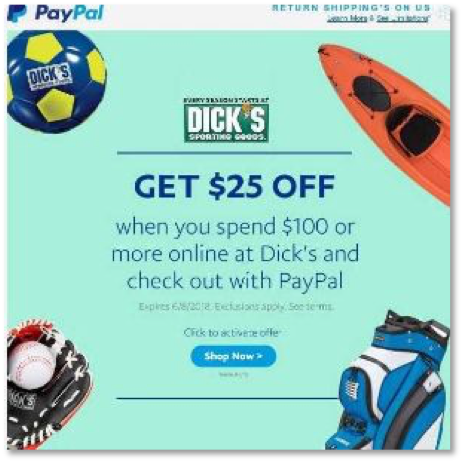

PayPal is also using the ‘spend-and-get’ offers seen from traditional credit card issuers. In one example, PayPal offered users a $25 discount when spending $100 at Dick’s Sporting Goods and using the payment platform at check out.

Read More:

- Digital Payments Approaching Universal Acceptance

- Banking Providers Fail to Sell Benefits of Mobile Banking and Payments

- How Banks Can Snag More Wallet Share In The Next 12 Months

Payment Networks Compete with PayPal

To defend payments turf against power tech firms like PayPal and Amazon Pay, payment networks are moving towards single-click payment options. According to Comperemedia, “Visa, Mastercard, and American Express all offer customers fast, seamless payment options for mobile and digital payments.”

Issuers are also using loyalty campaigns to encourage cardholders to make a card the default payment option within specific merchants and digital wallets. Special offers are used to drive action, but campaigns also highlight convenience or position doing so as a way to earn rewards faster, states Comperemedia in their analysis.

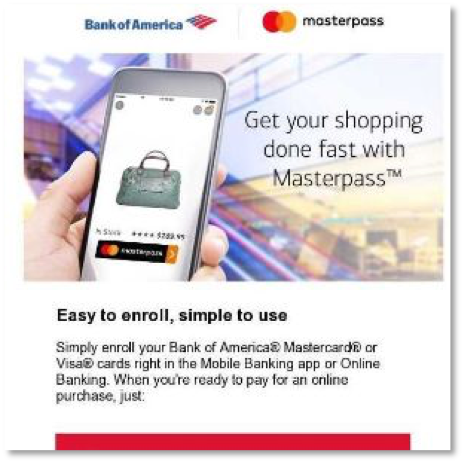

Bank of America encouraged cardholders to enroll in Masterpass to “Get your shopping done fast.” Sent in November, the campaign sought to engage customers ahead of the holiday shopping season.

In other examples, Wells Fargo promoted Visa Checkout with an email offer for a $10 statement credit when paying with the platform at participating merchants. The campaign listed Pizza Hut, Zulily, and StubHub.

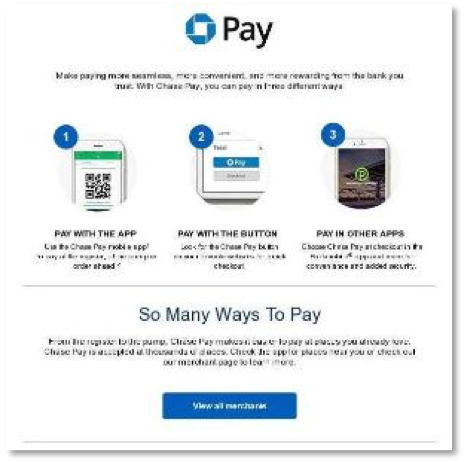

Finally, Chase promoted Chase Pay as a “more seamless, more convenient, and more rewarding” payment platform in an email highlighting mobile, one-click, and in-app purchasing capabilities.

Changing Established Payment Behavior

Once a consumer has listed a credit or debit card as the default payment option with an online retailer or service provider, it is much more difficult to change behavior. This is because the consumer has already determined how to save themselves time at checkout by listing their ‘favorite’ payment option.

To change behavior many organizations have used digital marketing to encourage consumers to replace their current one-click payment partner with an alternative ‘card’. Remember, the longer a consumer or small business uses a specific payment option, the harder it will be to change behavior. Some of the marketing examples below go directly at some of the payment platforms.

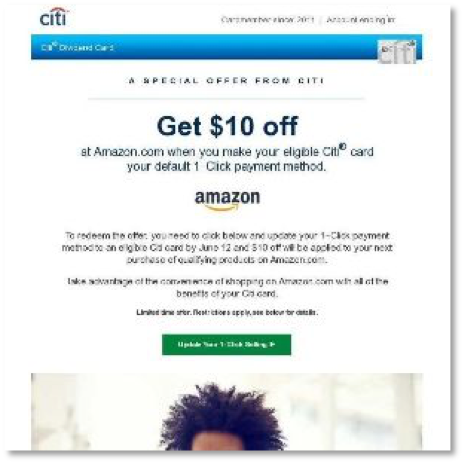

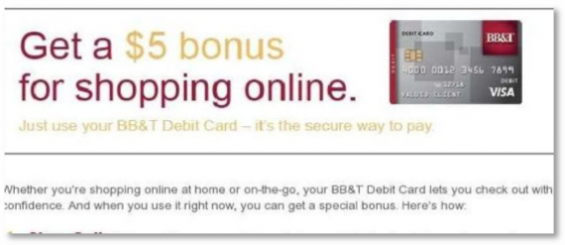

Citibank offered customers a $10 discount at Amazon.com after making their Citi card a “default 1-Click payment method” on the site. The campaign highlighted” the convenience of shopping on Amazon.com,” but listed no further benefits. A missed opportunity potentially?

Chase Sapphire cardholders were encouraged to set the Chase card “as the default payment for a consumer’s favorite apps, mobile wallet, online merchants, or monthly bills” in order to “earn more points on every purchase.” A great offer to consumers already familiar with the Chase Sapphire card.

Smaller Banks and Credit Unions Compete

The largest financial institutions encourage their customer bases to adopt new mobile payment options by emphasizing the speed and security of using digital technology. Some encourage use through discounts or special promotions at major retailers.

In response, smaller, regional banks and credit unions have leveraged both of these strategies when making mobile payment options available to their customers and members. As smaller organizations participate in the same digital payment networks as the ‘big guys’, they have an opportunity to compete for ‘top-of-wallet’ status by offering highly demographic or geographically targeted offers to encourage usage at local or national merchants.

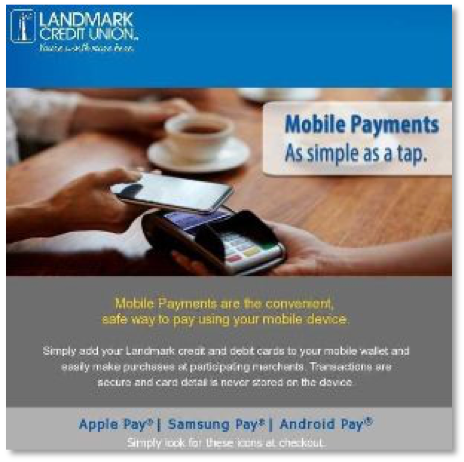

Landmark Credit Union encouraged members to add their cards to their preferred mobile wallet in the email below. Messaging focused on convenience and security of the payment option, listing Apple Pay, Samsung Pay, and Android Pay.

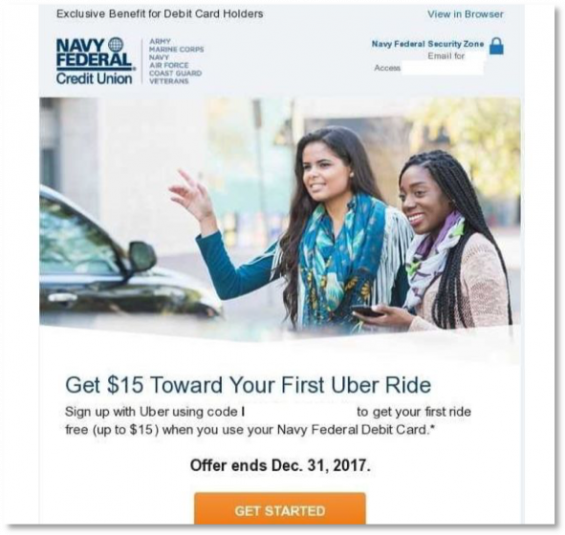

Providing Incentives for Digital Engagement

Some financial institutions have used incentives and accelerated rewards to encourage adoption on rideshare platforms and subscription services.

Financial service providers of all sizes will continue to compete aggressively for top-of-digital-wallet position with incentives and an emphasize on the convenience and security of digital payment methods. While the uptake has been modest, the opportunity (and threat) in the future is significant due to the importance of ongoing digital engagement with financial services organizations.

Beyond just traditional banks, credit unions and new non-traditional payment providers, major merchants have started to build and promote mobile payment methods of their own. Obviously, the stakes are significant, with competition from all sectors increasing. This is all happening as the consumer is expecting frictionless payments for all transactions, following the lead of rideshare and subscription services.