The transformation of retail banking has only just begun, with the pace of change only getting faster. The focus on digital delivery goes beyond online and mobile banking apps to the core of the entire banking operations. Without back-office modernization, the front-facing digital technologies will eventually fail to deliver the experiences expected by today’s consumer.

Leading banks and credit unions are investing heavily in digital banking technology, improving how consumers use mobile, web or digital platforms to access banking services. The application of big data, advanced analytics and new digital solutions are being combined with modern design elements to simplify a consumer’s life and potentially expand beyond financial services. According to a Forbes survey on banking customer engagement from late 2016, 86% of financial institutions indicated that digital solutions represented their top technology investments.

The largest U.S. banks are leading the pack when it comes to investment in digital channels. While the pace of digital banking growth has slowed somewhat over the last few years, the number of consumers using digital channels continues to increase. Much of this is due to improved customer experiences as well as heavy marketing that continuously reminds consumers of the benefits of adding additional digital services (bill pay, P2P payments, remote deposit capture, direct deposit, etc.).

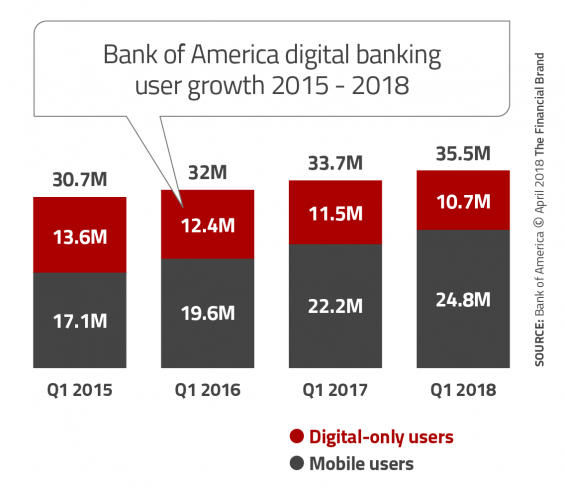

Bank of America Continues to Achieve Strong Digital Growth

Technology remains a top priority for Bank of America as it invests $3 billion annually in technological initiatives. In the most recent earnings report, BofA reported 24.8 million active mobile banking users, up 12% from the first quarter of 2017. The bank’s active digital users jumped from 33.7 million to 35.5 million users, with mobile transactions now accounting for 24% of all transactions. According to the bank, these transactions are equal to 1,280 banking offices.

Mobile channel usage rose 32% YoY to reach 1.38 billion mobile logins during the quarter. In addition, 28.6 million P2P payments were processed through Zelle, which was up 130% over the same quarter in 2017. Possibly most impressive was that 26% of all consumer banking sales occurred through digital channels at Bank of America and that close to 450K digital appointments were set in the first quarter.

Read More:

- Six Strategic Keys To Becoming a Mobile-Centric Bank

- Are Banks and Credit Unions Prepared for a New Mobile Era?

Digital Innovations Driven by Customer Expectations

More than simply putting lipstick on a pig, Bank of America has committed to continuous innovation to meet digital consumer needs. For instance, the bank launched an app that lets consumers to apply for a mortgage on the bank’s mobile app or online – potentially receiving conditional approval within a day.

Applicants can personalize their loan terms, lock in interest rates, and ‘save and resume’ an application in process. Users also have access to a platform designed to track loans, monitor user actions, upload documents and review and acknowledge disclosures from a smartphone.

“The new Digital Mortgage Experience is about … making things easy, intuitive, simple and fast,” Michelle Moore, head of digital banking at BofA, said in a statement. “It’s the latest example of our high-tech, high-touch approach to serving clients.”

Other technology advances include adding contactless ATM functionality, introducing peopleless financial service centers, expanding P2P payment options and rolling out a digital car-shopping service. Most recently, the bank added Erica, a virtual financial assistant, to the BofA mobile app in March.

Digital Innovations Driven by Customer Expectations

It doesn’t matter if you invest in digital and mobile banking or build innovations if the consumer experience isn’t good. To make matters more challenging, mobile banking users don’t compare their digital experience with the experience in a branch. They compare mobile banking to the experience received on non-financial services apps like Amazon, Uber, Best Buy and other leaders in digital engagement.

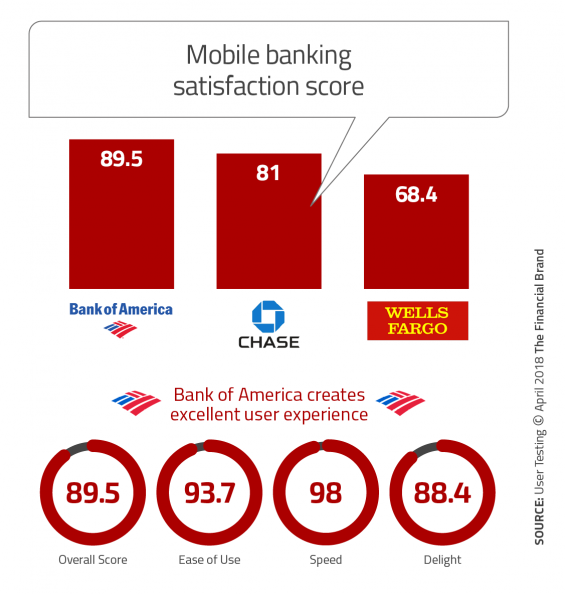

Research on the mobile experiences of the three largest U.S. banks was done by UserTesting to understand what frustrates or delights mobile banking customers. Three hundred mobile banking customers evaluated their banks’ mobile apps based on five key CX factors that improve ROI and increase loyalty: Ease of Use, Speed, Credibility, Aesthetics, and Delight.

Bank of America earned the highest ratings overall, with the speed at which customers could perform typical banking tasks being the highest rated quality. The navigation within the mobile app was smooth, and most functions were found in expected locations. Participants said they could complete most tasks within one minute.

Overall, UserTesting found that when it came to common tasks, like viewing an account balance or transferring money from one account to another, participants were satisfied with the experience at all large banks. However, when it came to more intricate inquiries – like setting up a fraud alert—all three banks fell short. Poor experiences with these tasks hurt the participants’ perception of the entire app.

Aesthetics refers to customers’ perception of the visual design of an app. According to UserTesting, “Today, customers expect well-established banks to have modern, attractive, and professional-looking visual branding. With 1 in 4 users abandoning an app after the first use, aesthetics are a key factor in priming banking customers for a positive experience.” For both Chase and Wells Fargo, the best rated CX attribute was Aesthetics. Bank of America was not far behind.

Aesthetics refers to customers’ perception of the visual design of an app. According to UserTesting, “Today, customers expect well-established banks to have modern, attractive, and professional-looking visual branding. With 1 in 4 users abandoning an app after the first use, aesthetics are a key factor in priming banking customers for a positive experience.” For both Chase and Wells Fargo, the best rated CX attribute was Aesthetics. Bank of America was not far behind.

As mentioned, digital consumers compare their mobile banking experience to other mobile experiences outside banking. These standards are reflected in the overall low scores for Delight reported for all three banks. “The key to delighting customers comes from continuously gathering human insights”, said UserTesting. “Understanding where to assist or delight banking customers in their journey will empower banks to provide them with an experience that not only meets but exceeds expectations.

Replicating the Success of Bank of America

Not every bank can invest the amount of money Bank of America does in technology and digital applications. That said, the ability to closely follow a digital leader like Bank of America is not a bad strategy (especially given the ‘sanle’s pace of many banking organizations). The key is to let Bank of America invest in the R&D to develop and test new applications and designs and follow their lead.

In addition, prioritize your digital investment to maximize the positive impact on the greatest number of consumers. As illustrated by the study done by UserTesting, this may involve the elimination of frustrations as much as the addition of functionality.

Allowing a consumer to open a new account online and with a mobile app without requiring a branch visit is a great example of eliminating a frustration. In addition, being able to access capabilities like viewing past statements, transferring funds with a single click, or simplifying the process of setting up a fraud alert all will improve mobile banking account growth and engagement.

Finally, all of the largest banks are aggressive in their communication to customers about the benefits of mobile banking. They use email, text alerts, online marketing and even direct mail to reinforce the use of digital channels.

Banks and credit unions of all sizes can improve their mobile app experience by listening to their customers and members. A relatively minor change to an app’s navigation, or simplifying functionality, could change a consumer’s entire perception of the digital or mobile app and of your brand overall.