According to research findings released by NTT DATA Services, voice-enabled virtual assistants such as Amazon’s Alexa and Apple’s Siri will play a central role in the future interactions consumers will have with their banking providers.

The study, which encompassed some 1,100 U.S. adults, set out to determine how happy people are with the digital customer experience (DCX) offered by financial institutions, and what consumers want from the DCX of the future.

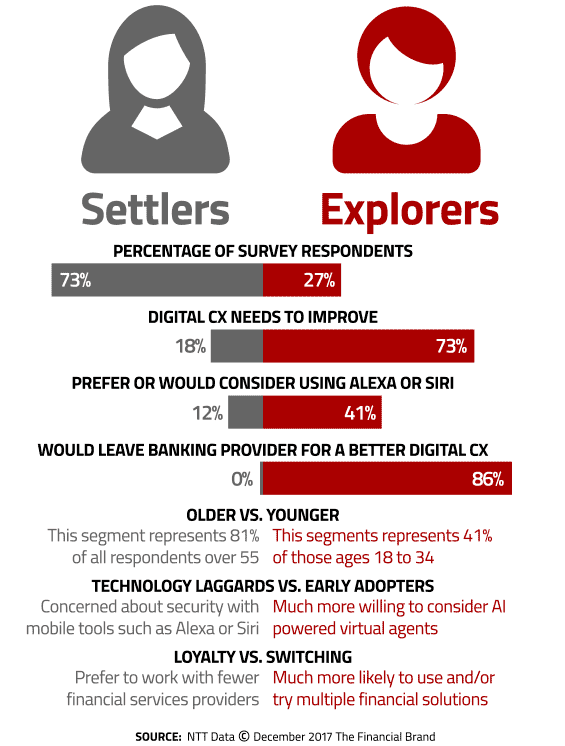

Researchers divided respondents into two categories:

1. “Settlers” – Those comfortable settling for the status quo. These “Settlers” are people who occasionally use mobile banking, and value an interface that is both fast and intuitive. They don’t need a bunch of bells and whistles; they just want a fast and simple experience that allows them to accomplish their objective(s) quickly, without having to learn anything new or figure things out. Because they are less demanding and less inquisitive than other consumers, they are more loyal to their banking provider.

2. “Explorers” – Those who want more from their digital banking experience. These “Explorers” are much more likely to switch banking providers because they aren’t satisfied with the DCX offered by banks and credit unions today. They are habitual mobile users, and therefore have higher expectations. They want an experience that is more personalized — one based on their preferences and prior interactions — and are looking for a level of support that is more customized and intelligent.

41% of Explorers say they would either prefer- or consider using AI-powered agents like Alexa or Siri as part of their banking experience. These digitally-savvy consumers are more likely to switch to financial providers offering such technologies.

Settlers, on the other hand, are typically older consumers using mobile banking tools and services less often, expressed concern about security when it comes to voice-assisted digital agents. Only 12% say they would be open to using something like Alexa or Siri for banking.

While the number of Settlers in the study vastly outweigh the number of Explorers, the age distribution of these segments mean that the future of digital banking will clearly center around Explorers.

“Explorers are the most important customer segment for financial services, as they pose a sizable opportunity for growth and customer retention,” explains Lisa Woodley, VP of CX/Financial Services Consulting at NTT DATA Services. “These Explorers are habitual mobile users, valuing tools, advice and proactive reminders from their financial services providers.”

Read More: Voice Payments Emerge as Tech Giants Compete for Voice-First Commerce

Voice-Enabled Agents Aren’t Just For Megabanks

Some smaller community banks and credit unions might assume that voice-enabled virtual assistants are only available to the financial industry’s biggest players. But there are solutions that actually put such technologies within reach of most banking providers, regardless of size.

Consider Enrichment Federal Credit Union, a $456 million institution with nine branches in Tennessee. Despite serving only 42,000 members, Enrichment FCU has become one of the first credit unions in the U.S. to roll out a banking solution for Alexa users. The credit union’s members can perform transaction-based functions, such as executing transfers between accounts, making loan payments, accessing balances, and looking up account histories — all using voice commands secured by a single sign on.

The options available Enrichment FCU’s members exceed what any other financial institutions can do with Alexa thus far. While other institutions allow customers to query for general information (e.g., loan rates or credit card balances), Enrichment FCU enables users to access all of their credit union accounts, including checking, savings, auto loans, mortgages, and credit cards. It also offers educational audio clips on critical topics such as security and financial literacy.

Room For Improvement: The Digital Banking Experience

Customer satisfaction with the digital experience offered by financial institutions is tepid at best. Only 16% of respondents say they are totally satisfied with their banking provider’s DCX. The top four most annoying aspects of the digital experience offered by banks and credit unions today include:

- Not being able to accomplish what the consumer wanted to do

- Options provided are not relevant

- Having time being wasted by tasks that take too long

- Having to enter the same information multiple times in a single transaction

The research emphasizes just how important it is for financial institutions to deliver a digital experience that is simple, streamlined, quick and intuitive. Respondents’ top three most important criteria for a best-in-class DCX include:

- Easy to understand (68%)

- Minimal effort required to gain access to digital tools (62%)

- Speed to complete financial transactions (49%)

The study also revealed that a more personalized DCX is a must — particularly for Explorers, who expect strategic financial guidance to help them reach their financial goals. Three out of four want their banking provider to connect the dots between their income, expenses and savings (e.g., PFM tools). Two thirds would like their bank or credit union to act as their “financial conscience” — the voice of reason on major overall spending decisions, there to advise them against purchases that will undermine their budget or savings goals. 61% say they would be comfortable if their financial institution intervened and prevented them from making a major (and potentially reckless) purchase.

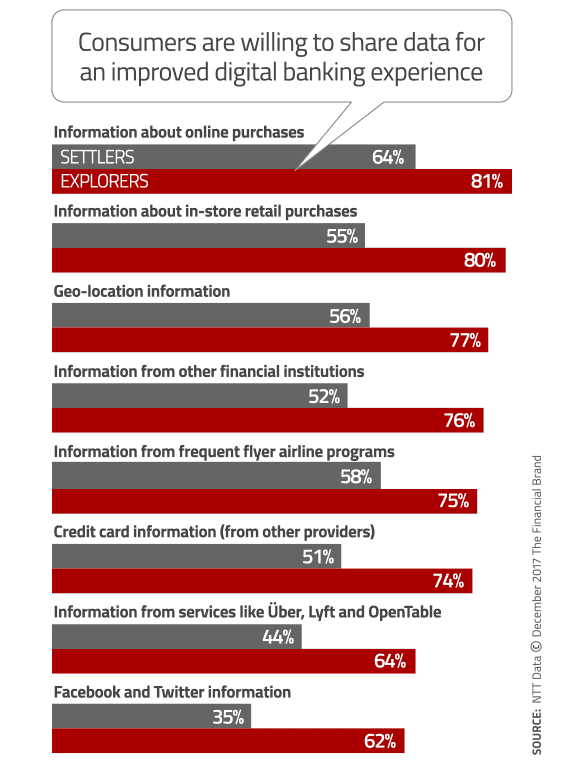

Consumers say they are also willing to provide access to a wide range of personal data for an improved DCX. They would share data as long as it enabled advice on spending, insurance products/coverage, and lending solutions that help them meet their financial objectives. Consumers claim they are willing to grant their bank or credit union access to information about their online purchases, Facebook activities, and Uber habits.