The 50+ generation of consumers is the most financial challenged in history. Numbering more than 110 million in America alone, they are confronting a future of complex options and less financial confidence than any previous generation. With most either entering retirement, or already in a post-employment phase, decisions this generation makes today will impact not only their life, but the financial lives of their children who may be forced to support them.

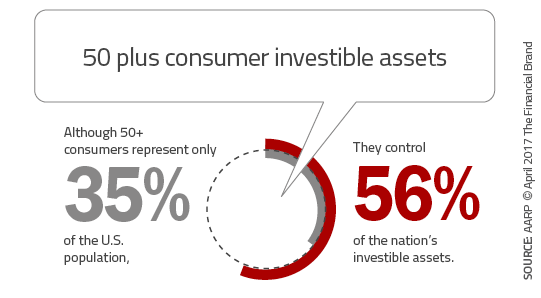

Although the 50+ segment represents only 35% of the entire U.S. population, they control more than half of the nation’s investable assets. The people in this generation are heavy users of almost all financial services, holding balances in their accounts that are coveted by banks, credit unions, insurers, financial planners and wealth managers. They are also the fastest growing segment of digital product users, becoming comfortable with the online and mobile solutions that other generations already depend on.

Most importantly, the 50+ generation is a huge segment with significant needs that are currently unfilled. And with future generations (including Millennials), not having faced these challenges to date, but directly impacted by the outcome of their parent’s financial decisions, meeting the needs of the 50+ consumer has the potential of impacting the banking loyalty of their children.

A Generation Under Stress

The 2017 Financial Innovation Frontiers report, published by AARP, states that 70% of consumers 50+ are a decade or less away from the traditional retirement age of 65. Unfortunately, many are far from prepared for this next stage of their life.

According to the report, “The 50+ consumer is straining to cope with debt, racing to catch up on saving, and worrying they must scale back their retirement dreams. They have good savings habits, yet they don’t know where or how to start tightening their belts.” While this generation may have a foot in traditional banking, they are open to new financial tools and alternative financial services when the solutions of the past don’t meet their needs.

The last thing this generation wants is to be a burden to others around them … especially their children. Unfortunately, in many situations, the amount saved for retirement may not be enough to live a comfortable life in light of modest market returns and a lengthening lifespan.

While most would not be considered ‘digital natives’, they own and use online and mobile tools more each day. Like all consumers, they use these digital tools to search for financial solutions. According to the AARP research, there are 7 primary stress factors each aging consumer faces:

- The impact of unexpected expenses and financial emergencies. These are made more severe in households where there was a higher standard of living pre-retirement.

- The realities of caregiving for parents. Many consumers over the age of 50 are financially responsible for their parents. The concern of being in the same position in the future is stressful.

- The burden of student loans. Many 50+ consumers are bearing the burden of student loans for their children, their grandchildren, and sometimes even themselves.

- The lack of savings for retirement. The shift from defined-benefit plans to 401(k)s and other defined contribution plans has created an entire generation of households with less funds than needed for the future.

- The rising cost of healthcare. The combination of longer life expectancy and more complex healthcare options makes shopping for, and managing, healthcare costs more difficult than ever.

- The complexity of financial products. The changing array and complexity of financial solutions can be overwhelming for most consumers. Combined with changing tax regulations and new fintech players, the ability to manage financial holdings optimally is difficult.

- The lack of tailored and helpful digital tools. While most in the 50+ segment are relatively proficient at searching the internet on digital devices for consumer goods, doing the same for financial services is far from easy. Leveraging digital devices for managing finances is even tougher.

While there have been dozens of new digital savings tools introduced in the past few years, virtually all have been geared to the Millennial generation, with decades left until retirement. What has been missing are tools that address the vastly shorter asset accumulation timeline faced by 50+ consumers as well as digital tools that simplify a much more complex portfolio of services held by this generation.

A Generation With Massive Potential

According to AARP, consumers 50 and over will generate $116.8 billion in revenue in 2017, including revenue from checking and savings accounts, credit cards and consumer lending. AARP expects that revenues from this segment will reach $123.7 billion by 2021.

Increasingly, 50+ consumers are also using alternative financial services. AARP estimates that the 50+ segment will spend $15.3 billion in the alternative financial services sector by the end of 2017, with a growth rate of 4.25% annually through 2021.

The reason for the shift away from legacy products is that traditional banking services are no longer able to meet all the needs of the 50+ cohort … hence, the segment is forced to seek services from alternative providers. These new fintech firms are even siphoning off revenues from traditional product categories like checking, credit card and lending products.

Bottom line, serving the 50+ consumer segment can have massive payoffs.

Despite the opportunity, few fintech innovations have been introduced that could simplify this challenging financial journey. This is why AARP has been holding their own innovation competitions outside the current array of industry events. AARP’s 2017 Financial Innovation Frontiers study emphasizes the tremendous need for trusted financial innovations that can guide the 50+ consumer as they spend, save, borrow, invest, insure, and plan their financial lives.

How Financial Innovations Can Help

The 2017 Financial Innovation Frontiers study from AARP highlighted five key areas where innovators can have a transformative impact on the 50+ generation:

- Remove friction from the user experience. As is true with the banking industry in general, all processes and channels must be simplified. Digital development with older generations in mind will also improve the experience for younger consumers. The concept of “If you built it, they will come,” doesn’t apply to financial services for older consumers. Financial product learning tools are needed to emphasize the benefits of using new innovations.

- Improve customer service. Connect the 50+ consumer with advisors during key financial moments, helping consumers to become financially independent.

- Proactively deliver personalized insight and advice. As with the industry in general, using data to deliver personalized solutions is the key to success. Personalizing in the context of healthcare costs, retirement savings, risk tolerance and the unexpected is more important to this segment than any other.

- Transform financial anxiety into digital empowerment. Help consumers use new digital tools to their advantage including budgeting, automated savings, expense management, etc.

- Influence regulatory change and financial policy. Encourage healthy digital disruption in consumer protection, privacy, new market entrants and all areas of compliance and regulation.

The Next Digital Generation

Just because the 50+ consumer segment has been slower to embrace digital technologies doesn’t mean they are against change. Instead, they have more experience using current financial solutions than other generations, and most digital solutions are not significant improvements over what they currently use. There is no better example than mobile payments, where current solutions are more convenient than a digital solution not accepted universally.

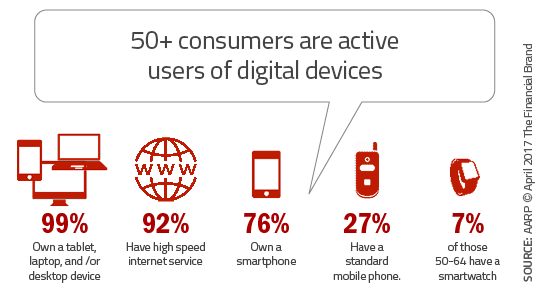

“Today, 99% of 50+ consumers own a tablet, laptop, or a desktop device,” states the AARP study. “Even the 70+ seniors are tech-enabled, with virtually all owning a computer and 54% toting a smartphone. When it comes to technology, they adapted to it, adopted it, demanded it, and made it an essential part of American life.”

A Generation Afraid to Ask for Help

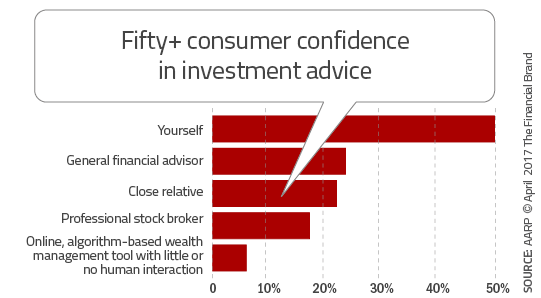

Given the extensiveness of financial holdings of the 50+ generation and the anxiety over the future, you would think that the majority of this segment would use outside advice and tools to help them aleve the financial stress. Interestingly, the typical 50+ Consumer handles his or her own financial planning and seldom seeks comprehensive professional services according to the AARP study.

Part of this phenomenon may be caused by the perceived elite nature of wealth management and advisory services. “Financial advisors are for the rich,” may be a common refrain. The other option may be similar to why a patient most in need hesitates to see a physician … the desire to avoid being embarrassed by bad news. Part of the reason may simply be a lack of trust in options they are familiar with. These are the exact reasons why easy-to-use digital money management solutions are needed for this segment.

“Many [50+ consumers] doubt their financial decision-making, have failed to take basic steps to save, and don’t seek help from pros. These contradictions amount to an opportunity for financial innovation that helps self-directed 50+ Consumers make wiser choices,” says the AARP report.

Consumers in the 50+ category have not taken fundamental planning steps, according to AARP. In the past five years, only 7% have created a five-year financial plan, and only 9% plan to do so in the next five years. Similarly, just 10% of 50+ consumers have opened a savings account intended for emergency purposes, and only 9% plan to open an account for this purpose.

A Way to Attract 50+ Consumers and Millennials

It is hard to believe the emphasis that the banking industry places on the Millennial generation when there is such a significant opportunity with the 50+ consumer. Not only does the older cohort have unmet needs, but they have more value to the financial services industry than any other segment.

While the 50+ consumer segment has been somewhat hesitant to use digital technology, most of the burden for that phenomenon rests with the industry that focuses more on saving costs than improving digital experiences.

“The financial services industry must rethink how it delivers financial services,” states the report. “It must devise a way to proactively engage customers more deeply and powerfully. It must use digital tools to put the ‘personal’ into ‘personal finance’ with one-to-one insight, advice, and recommendations.”

What is missed in most conversations regarding the 50+ consumer is that Millennials have a vested interest in the financial well being of their parents. If the financial services industry does not help make the 50+ consumer more secure, the burden will transfer to the younger generations.

When looking for a digital solution for consumers close to retirement, there is no reason why the solutions can’t engage the entire family. Doing so will not only result in a more loyal 50+ consumer, it may also result in a loyal (and more financially valuable) Millennial customer