The banking industry is in transition, with a need to increase revenues, decrease costs and improve the consumer experience. As digital engagement becomes the norm, the banking industry is becoming a consumer-to-business (C2B) industry, with customer experience standards being set by Google, Apple, Facebook, and Amazon (GAFA). In some instances, these large technology giants have begun to offer competing financial services such as mobile payments, digital wallets, P2P and even lending services.

In the C2B era, consumers are increasingly in control, engaging with financial and non-financial organization when and where they want to, often creating value in new ways including product reviews, word of mouth and referrals. As the GAFA giants and other smaller fintech firms become more relevant in consumer’s lives, they are also collecting insight that makes their potential engagement capabilities even stronger. Traditional banking organizations must respond.

According to the Accenture report, “Beyond the Everyday Bank: The GAFA Banking Approach“, “The goal for banks is to be relevant at all times, for all financial and non-financial services, with consistent and fulfilling customer experiences in both the digital and physical spaces. Accomplishing this will require building partnerships, including those with financial technology companies (fintech start-ups), and leveraging the power of real-time analytics.”

The risk of not taking proactive action and leveraging advanced analytics is the prospect of becoming a back-office utility for technology giants or new entrants. According to Accenture, by 2020, different business models could impact up to 80% of existing banking revenues. Revenue streams with a high degree of impact could include checking accounts, consumer finance, cash management, and small- and medium-enterprise (SME) payments.

Read More: The End of Banking as Usual

5 Key Role(s) to Get Closer to the Consumer

Accenture believes that banking organizations can learn from the GAFA approach about the innovative ways in which to become a greater part of their customers’ lives. Operating in one or several of the following roles should be consiidered:

- Relationship Player: The banking firm owns the relationship with customers, leveraging relationships with the large GAFA networks and fintech start-ups to provide financial and non-financial solutions. In some cases, the services offered may extend beyond services offered by the financial institution.

- Platform Provider: The financial institution provides an open platform for sellers, buyers, and content providers to interact, create and sell products and services and share value.

- Core Financial Services Utility/Manufacturer: The traditional role of banking, including the development and packaging of traditional financial services.

- Innovation Playmaker: The bank or credit union supports fintech innovation by investing in incubators, accelerators, and venture funds, providing capital for new ventures.

- Digital ID Enabler: The financial institution becomes the primary access point to digital commerce. This may include central authentication, digital IDs and privacy control with potential monetization of digitalized personal data.

The Evolving Business Model of Banking

Banking needs to change the way they deliver (and consumers perceive) financial services. Business models need to evolve beyond traditional banking services to include alternative business opportunities that leverage the relationships, insights and consumer needs already in place and the opportunities of the future. According to Accenture, “The goal is to quickly develop a viable response to emerging digital disruptors while managing strategic risk to avoid the loss of revenues to those disruptors.”

According to Piercarlo Gera, Senior Managing Director, Accenture Distribution & Marketing Services, banking needs to answer key strategic questions including:

- What is the total investment for the digital agenda?

- How should that budget be allocated to “GO Digital” initiatives (businesses chosen for focus) and “BE Digital” initiatives (enabling and optimizing the overall enterprise)?

- For both GO Digital and BE Digital initiatives, what are the priority items?

- Should the bank go it alone or partner up with financial technology (fintech) providers?

“GO Digital” Business Opportunities

There are three major GO Digital sets of platform/businesses that Accenture believes banking should consider within the GAFA banking portfolio:

- Digitally powered financial platforms: Banks could offer physical and digital platforms for different segments that provide an easy and simple experience. Advisory platforms, small business platforms or retail banking platforms could be developed for ease of engagement. Examples are JP Morgan Chase’s OnDeck partnership or TD Bank’s and other financial organizations’ partnership with Moven.

- Offer lifestage services: Partner with non-financial service providers to become an integral part of a consumer’s life in a contextual manner using available insights. Adapting to real-time changes in needs surrounding housing, health, travel and purchases, data is utilized to proactively respond to potential non-financial needs.

- New businesses: Development of new businesses that can enter new markets, monetize unused branch space or customer insights, new small business or blockchain services, venture or strategic investments in new businesses.

By expanding business opportunities, digital interactions will increase along with the depth of insights into consumer behavior and needs. This will enable a deeper relationship with the consumer, placing the banking organization at the center of a consumer’s daily life.

“BE Digital” Enablers

To expand the products and services offered and become central to a consumer’s daily life, financial institutions need the following four enablers according to Accenture:

- Digital culture: There is a large divide between ‘saying’ and ‘doing’. What is required is a digital culture that transcends the organization. According to Accenture, “It is important to establish an environment where new, important positions—such as data scientist, digital architects, community advocacy builder, and even storytellers – can flourish.

- ‘Liquid’ CRM engagement: In a real-time environment, the engagement must occur at virtually the same time as insights are captured. This is the definition of personalized contextual engagement. Those who hesitate, lose.

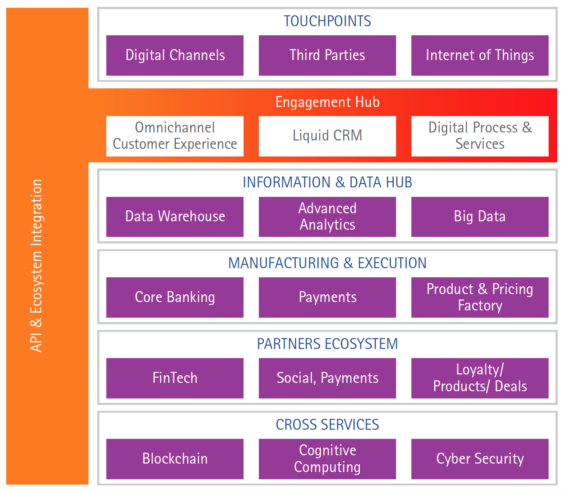

- Digital IT architecture: The IT architecture of the future needs need to be liquid (highly decoupled and made of granular components to be created/customized in an agile way), intelligent (embedding robotics and cognitive computing to accelerate the process digitization), connected (API-driven, enabling banks to integrate easily with third parties and partners), and smart (using distributed consensus ledgers and smart contracts to enable real-time transactions without intermediaries and at much lower costs).

- End-to-end process digitalization: Beyond the digitization of front-office functions, the digitization of back office processes and tasks.

The Impact of a GAFA Approach

By learning from and applying the approach of the GAFA firms (Google, Apple, Facebook and Amazon), costs can be reduced while revenue opportunities multiply. Using these larger technology firms as a guide, banking can do better at being accessible 24/7, in real time, leveraging consumer insights to provide contextual financial and non-financial solutions. According to Accenture, “For banking executives, this means focusing their investment strategies and creating new business models—based on a portfolio of businesses and selection of roles to play—that will multiply interactions with customers, generating valuable data and driving cross- and up-selling opportunities.” Of greatest importance is to act quickly and decisively since playing catch-up gets more difficult by the day.