Banks are falling short on important aspects of the customer experience, and are increasingly vulnerable to competition from new banking providers, according to the “2014 Global Consumer Banking Survey” from Ernst & Young.

The extensive survey, which encompassed 35,642 consumers from 43 different countries, examines 31 core elements of consumers’ banking expectations and preferences. Rather than look at just the traditional parameters like age, geography and income, the report groups consumers into consumer segments sharing behavioral characteristics, products, channel preference and reasons for trust. In a very efficient 48 pages — crammed full of charts, graphs, facts and insights — the report explores a wide range of subjects pertinent to financial marketers: how to segment banking consumers, people’s banking preferences, retail channel delivery, and a host of other issues.

Take a good, long look at the report. You won’t regret it.

Wooing Fickle and Flighty Consumers

“Bank consumers remain with their current provider through inertia.”

— Heidi Boyle, EY Financial Services

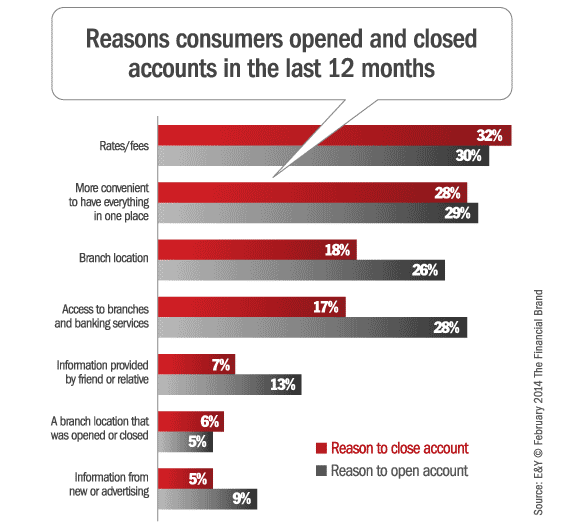

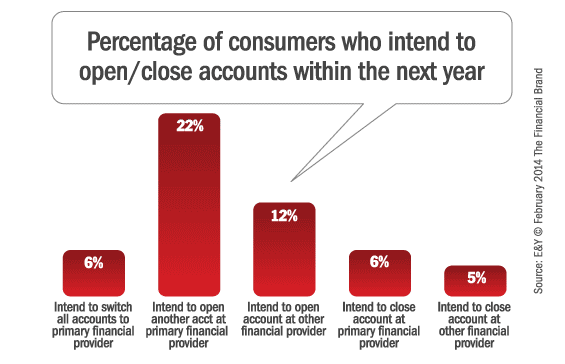

52% of consumers have opened or closed at least one banking product in the past year, and 40% plan to do so in the next 12 months. Of the 60% of respondents not planning to close or move their accounts, it is not necessarily because they are confident that they are with the right provider: 22% of those who plan to maintain their current relationships feel all companies are the same. 17% say it is just too difficult or time consuming to change.

Reality Check: That means one out of every six consumers would dump their bank if they could.

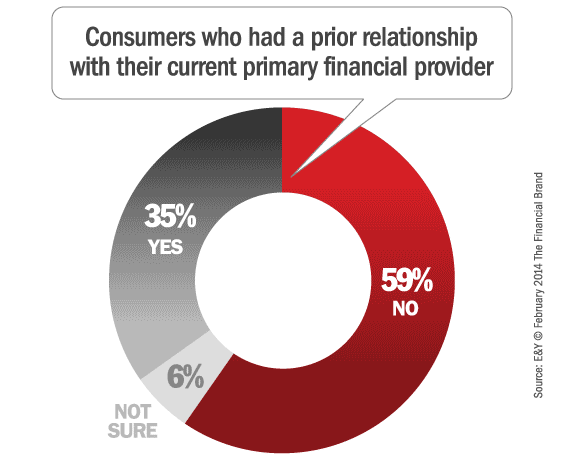

When asked whether consumers had accounts or services with a bank or credit union before that institution became their primary financial provider, only 35% of respondents reported that this was the case. This suggests they are very receptive to exploring and establishing relationships with new providers. Apparently their current providers aren’t getting the job done.

Consumers don’t believe that established banks enjoy any real advantage over newer players in the banking space, even when it comes to providing advice on heady financial matters like investments and retirement. More than 30% of respondents said alternative banking providers are better able than traditional banks to improve how consumers conduct business and reach their financial goals.

“Traditional banks are performing well on basics like branch access and ATM availability but they are most vulnerable in areas with the highest growth potential,” Boyle points out. “There is real opportunity for alternative providers to dominate the digital offering, personalize the experience and become primary providers.”

Read More: Room for Improvement – Consumers Expect More From Financial Institutions

Channel Preferences, Usage & Satisfaction

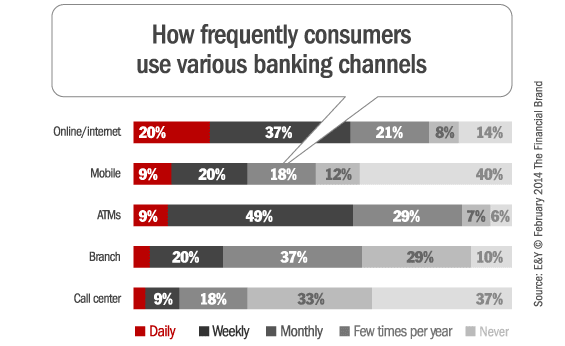

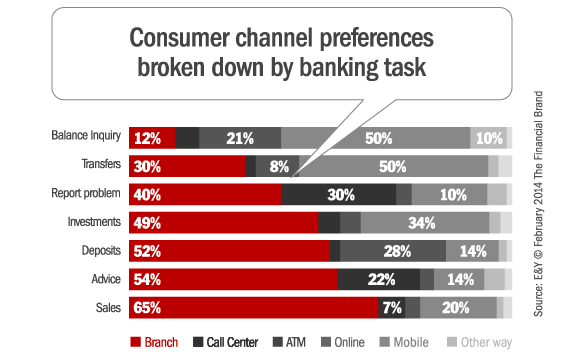

Consumers have many channels to choose from, and vary their selection depending on access, experience and basis, respondents reported using the internet most combined with weekly usage, people use the online and ATM channels far more frequently than any others.

Complaints Pour In… How Are You Coping?

“Improving how they deal with resolving problems or complaints will be critical if banks are to continue to win confidence and build trust.”

— Heidi Boyle, EY Financial Services

Approximately one-third of bank consumers contacted their bank about a problem in the past 12 months. One quarter say they are “very satisfied” with how their issue was resolved, while 42% feel “satisfied” and a third feeling “less than satisfied” with the outcome. Of consumers who were very satisfied, 58% gave the bank more business, while 32% of consumers very dissatisfied with the problem-resolution experience closed some or all of their accounts.

Reality Check: The formula for consumer complaints and how you handle them is simple. Fix problems = relationship retained and more revenue. Don’t fix problems = lost relationship, lost revenue.

Transparency about fees, charges and guidance on how to avoid them are consistently one of the biggest issues for banks across the globe to tackle. They represent 15% of all problems reported, and are second only to denials of credit/loan requests.

“Banks need to get better at communicating their fees and charges with their consumers,” Boyle says. “The good news is that solving a problem or addressing a complaint creates a critical interaction and a customer’s business.”

Read More: Google Data Reveals Banking Trends

3 Key Improvement Areas for Banks

E&Y’s “2014 Global Consumer Banking Survey” identifies three key improvement areas for banks.

1. Make banking simple and clear. Consumers are constantly flooded with information and struggle to understand choices, charges and changes. To make banking easy for consumerss, banks should be transparent and concise around fees, rates, services and other communications.

People depend on web, mobile, social media, telephone and in-person channels, so banks should offer an omni-channel experience that combines both traditional and digital banking. To stay competitive, financial institutions need to continue building channel capabilities to provide seamless 24/7, real-time access to banking.

2. Help people make the right financial decisions. Many consumers want help developing their financial plans and goals. The banks that provide that advice are likely to grow their businesses. More than 70% of respondents say they would increase business with their provider if advisory services improved. Banks have the opportunity to create a mutual exchange of value by personalizing the experience, based on a holistic perspective of the customer’s unique situation and needs.

Banks can augment this experience by leveraging both internal and external resources. This could include a skilled network of financial advisors, data about what similar consumers have spent and personal financial management tools that help people save, invest and spend more wisely.

3. Be proactive in anticipating and solving problems. Effective problem solving is vital to any bank-customer relationship. Problems are inevitable, but survey data shows that there is astounding upside if people are satisfied with their problem resolution versus a downward spiral in trust and business if dissatisfied. Making it easy for customers to raise issues, equipping the front line to handle certain problems and escalate others, explaining why the issue occurred and following up to ensure resolution is complete are crucial to successfully handling problems.

Bonus Download: 227 PowerPoint Infographics for Financial Marketers