Banks and credit unions have often agonized over where to focus first: their products or their brand. Some institutions believe that over time, their products will eventually define their brand while others believe they should work backwards. In the end, we have seen organizations appear where their products and their brands are nearly indistinguishable.

Numerous fintechs have emerged to serve the specific needs of certain populations with targeted product offerings such as checking and savings, prepaid cards, peer-to-peer payments, paycheck advances and mobile investing.

Even though these fintechs have now increasingly penetrated the market, banks and credit unions would be remiss to concede on certain competitive segments and should instead, focus on their own product, experience and innovation while leveraging their established brands and market presence.

When developing a strategy to reach various populations, financial institutions should consider integrating three main pillars into their plan:

- Tailored products

- Technology

- Financial education

1. Tailored Credit Card Products

A credit card can be a fundamental product in engaging individuals looking to build credit over time, eventually leading to increased credit. Individuals may have trouble getting approved for a standard unsecured credit card if they find that their credit score is below 650, either from having a limited financial history or past credit problems. One option may be a secured card to build credit if they pay their card payments according to terms.

A bank or credit union may consider a tailored secured credit card product to help people build their credit scores. The customer puts down a security deposit for the account, which typically determines the credit limit. Once the cardholder completes a set number of on-time payments, the cardholder may begin to establish a healthy credit history, providing the opportunity to open an unsecured card relationship in the future.

Secured cards have become more competitive and appealing with many offering rewards, graduation strategies and full integration into a financial services provider’s digital infrastructure. These graduation strategies may help with long-term member retention as well, given the positive reinforcement of good behaviors.

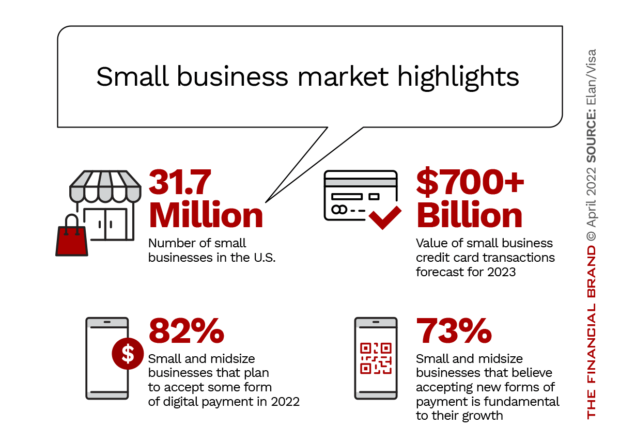

Another segment that banks and credit unions may consider for a tailored product is small business. Small businesses want different things from a credit card product including:

- The ability to manage transactions, category spend and line sizes,

- Robust reporting with integration into financial management tools,

- Specialized servicing functions,

- Flexible underwriting,

- Tiered rewards or smart tiering of rewards.

Given the wide variety of needs consumers and small businesses may have when it comes to credit cards and credit building products, it’s important that banks and credit unions offer a complete suite of credit card products that can meet numerous needs, including building credit, offering rewards and convenient, digitally enabled payments. It may not be enough to simply offer one or two credit card options.

As financial institutions review their credit card acquisition strategies, they should position their product offerings to attract small businesses. Products may include loan products of small business investments, merchant processing capabilities, business focused checking/debit solutions and depending on scale, either corporate or small business payment products.

In all cases, adding features to these products that focus on digital first, making payment acceptance easier, helping businesses better manage their accounts payable/receivable, expense tracking/control or cash flow management/forecasting, can help a bank or credit union build deeper relationships with small businesses.

2. The Right Mobile Technology

Digital technology is rapidly increasing in importance and developing accessible technology is one way for financial institutions to eliminate barriers to engage selected populations. As of February 2021, 85% of U.S. adults had a smart phone, making mobile and web features an essential opportunity to reach a broader community. These individuals may not live close to a branch or have easy access to transportation to get to a physical location.

Forty-one percent of consumers say that mobile apps are their primary means of banking, making mobile technology a top priority for banks and credit unions. Use of online banking (mobile and web) continues to rise and has increased pre- to post-pandemic by 13%. This is an 11% increase on mobile apps alone. In 2020, 88% of general-purpose card applications were submitted digitally. (All statistics sourced from the report listed at the end of the article.)

Mobile apps should contain all the capabilities members and customers need to complete critical banking functions without having to visit a branch including:

- Ability to check balance and make a payment,

- DIY servicing such as setting travel notifications and enrolling in paperless statements,

- Options to set up and manage account alerts, request a balance transfer and view account statements,

- Fraud monitoring capabilities like transaction disputes and lock/unlock card for transacting,

- Review rewards earned and redeem easily.

3. Financial Education Tools

Access to comprehensive and easy-to understand financial information is an obstacle for many cardmembers, particularly those who have avoided traditional banking, but also serve as an opportunity for banks and credit unions to make financial resources accessible and readily available.

When it comes to financial education in 2020, over one in ten (13%) U.S. adults admit they are “not very” or “not at all” confident in their knowledge of personal finance. This figure has risen each year since 2017 (8% in 2017, 10% in 2018 and 12% in 2019).

Findings from a report by Elan and PYMNTS highlight that consumers have a desire to engage with financial institutions to build better credit but may not know how, or where, to start. Financial education tools, available online and in app, should cover a variety of topics, including, but not limited to:

- Cardholder’s current credit score, factors that determine it and tips to improve their rating,

- Best practices for when and how to use credit cards to build credit,

- Ideas on how to manage loans and budget savings,

- Tips to protect financial information from cybersecurity threats, including a clear outline of when and how a financial institution would contact a customer for information.

When developing an approach to reach any population, banks and credit unions should consider these strategies with an emphasis on strong credit card offerings. Whether your institution is exploring a partnership credit card program to support your efforts, or starting from scratch, Elan is ready to help you succeed and grow.

Sources for all statistics mentioned in this article can be found in the full report from Elan.

About Elan Financial Services

Elan partners with more than 250 credit unions and offers an outsourced credit card program for consumer and business accounts of all sizes. Our dedication to our partners, growth philosophy and investment in evolving technology continues to make us a leader in the industry. For more information, visit www.cupartnership.com.