The United States Postal Service is re-introducing a catalog of financial services it once offered decades ago as a part of a new pilot program.

To get it off the ground, the service rolled out the program mid-September 2021 in four cities: Washington, D.C.; Falls Church, Va.; Baltimore and The Bronx, New York. The new program is part of a 10-year plan USPS announced earlier in 2021, NBC notes.

The Postal Service is working in partnership with American Postal Workers Union (APWU) on the banking pilot. Union President Mark Dimondstein told NBC the test run was “a small step in a very positive direction.” He explained why:

“We view expanded services as a win for the people of the country, a win for the Postal Service itself, because it will bring in new revenue, and, of course, a win for the postal workers who are extremely dedicated to the mission.”

The Postal Service’s pilot program, currently only includes paycheck-cashing services so far, where consumers can exchange their paycheck or cash business checks — which cannot exceed $500 — for single-use Visa gift cards, according to The American Prospect.

In the future, the program could also include:

- Check cashing

- Bill paying

- ATM access

- Expanded wire transfers

- Improved money orders

The venture has amassed plenty of criticism from some politicians and banking trade groups who are frustrated that the government thinks there is a need or a place for the postal service in the banking industry.

Adversaries of Postal Banking

Pat Toomey, Republican Senator from Pennsylvania, is a firm opponent of postal service banking, albeit not the only one. During the American Bankers Association’s Washington Summit, Toomey was asked about his thoughts on legislation which would allow the Federal Reserve to offer banking accts through USPS.

“It’s a very bad idea,” he said, explaining that he is not at all discrediting the efficiency of the post office.

“They have a tough job to do,” Toomey continued. “But even if they were the most competent, professional and best-run organization on the planet, I would not have them in the banking business. We have banks. The idea that the government is going to do a better job is just laughable.”

“I would have to work very hard for a long time to come up with a worse idea than having the government become a national bank executed through the post office.”

— Senator Pat Toomey (R-PA.)

Paul Merski, chief lobbyist for the Independent Community Bankers of America (ICBA), agrees with Toomey, arguing the “Postal Service is in no way, shape or form equipped to compete in the financial services space.”

“This is just a bad idea that doesn’t seem to want to go away,” Merski said, as reported by NBC. “The post office is having trouble financially keeping up with just the delivery of mail and losing billions of dollars year after year for over a decade now. You should not have a repurposing of the post office to do financial services — financial services have never been more complex.”

Other trade groups, such as the Consumer Bankers Association (CBA), the ABA and the NCUA have also publicly voiced their disapproval for the program, advocating that banks and credit unions are already prepared to safely and effectively provide banking services.

“The well-regulated, well-supervised American financial services system requires banks to have policies, procedures and controls to ensure adequate risk management, regulatory compliance, consumer protection, and privacy protection — areas the U.S. Postal Service has little to no knowledge of,” says CBA spokesperson Billy Rielly, as reported by Banking Dive. Policymakers should instead be encouraging financial institutions to innovate in the financial inclusion space, Rielly said.

Read More:

- Regulators’ Revenge: Fintechs’ Success Spurs Calls for More Oversight

- Will New Administration Rewrite the Rules on Banking Mergers?

- Biden’s Banking Watchdogs Could Create Real Headaches for the Industry

Second Time the Charm?

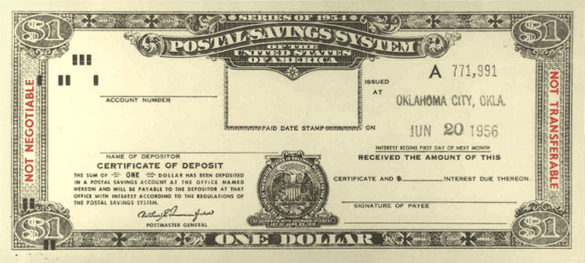

This is not the first time around that the U.S will have tried out a postal banking service. Congress first established a similar program in 1910 — called the Postal Savings System — which was officially launched the following year and advertised as a good opportunity for immigrants.

“The legislation aimed to get money out of hiding, attract the savings of immigrants accustomed to saving at Post Offices in their native countries, provide safe depositories for people who had lost confidence in banks, and furnish more convenient depositories for working people,” according to the USPS. The peak of postal banking was in 1947 when deposits reached $3.4 billion.

It was in the years following World War II, when banks, now with FDIC insurance, offered higher rates of interest, that eventually led to the termination of the Postal Savings System. In 1966, regulators abolished postal banking completely, outside of money orders.

Although the current Postal System is the butt of many jokes and has seen its business undercut by overnight delivery and email, and its service quality deteriorate, at one time, postal banking, “was in fact so central to our banking system that it was almost the alternative to federal deposit insurance, and served as such from 1911 until 1933,” as recounted in a short history in Slate.

Will a Budding Trend Develop?

For every critic of the post office bank, there is an advocate campaigning to re-jumpstart the program.

The loudest arguments as of late have come from New York Democratic Senator Kirsten Gillibrand who in 2020 introduced a bill called the Postal Banking Act, which would bring back financial services offered through the post office. Then, a year later, she partnered up with Senators Kaptur (D-OH), Ocasio-Cortez (D-NY), and Pascrell (D-NJ) to set aside $6 million to support a postal banking pilot program.

And they’re certainly not the only ones. One of the primary missions of Senate Banking Committee Chairman Sherrod Brown (D-OH) has been to advocate for the creation of bank accounts through the USPS.

“The goal has to be to reorient our economy from Wall Street wealth to the dignity of work,” he said, as reported by SPGlobal.

In March 2021, Brown introduced a bill which would allow people to set up a “digital dollar wallet” — coined a ‘FedAccount.’ In essence, the FedAccount would be a free bank account for people to receive money, make payments and take out cash — available at banks and post offices alike.

While the United States long ago abandoned banking through the national post office, the rest of the world continued to offer postal financial programs. The postal workers union reports that, as of 2018, 91% of global postal services offer financial services in one fashion or another, serving populations exceeding 1.5 billion people. Additionally, McKinsey found in an analysis of 54 global markets that more than half of all postal carriers are “well positioned to enter the financial-services market.”

Catering To The Underbanked

Overall, the foundational argument for the postal banking system is that it provides financial services to the populations that are unbanked or underbanked in the United States. While less than 6% of the population are completely underbanked, according to the FDIC, that still is approximately 7.1 million households.

The University of Michigan emphasized in a May 2021 report that, even while there are large groups of people who may not have an easy access to banks, many of them can find a post office. The report went on to explain that the need for easily accessible financial institutions became especially clear following the pressure of the pandemic, which highlighted the limitations of private financial institutions.

“Postal banking through USPS retail locations could uniquely serve communities that larger private banks have ignored and that smaller community banks have struggled to reach,” the report reads.

Read More: ‘Public Bank’ Growth Will Draw Key Consumer Groups from Private Sector

The university reports there are some states which could benefit more from these postal financial services than others. For instance, the report says that 94% of California census tracts have a post office retail location but not a community bank branch, in addition to 90% of Arizona and 87% of Idaho. [Emphasis added.]

Digital transformation has a stake in this, the report reads, as mobile and online options are inadequate for any person who cannot get access to internet services via a computer or cell phone.

“It’s a case of market failure where the banking industry is not interested in serving these people because they’re not profitable enough and where the Postal Service, because it is a government service, can step in and help with that market failure and ensure those services are available,” says Christopher Shaw, who wrote “Money, Power, and the People: The American Struggle to Make Banking Democratic.”