Why should banks and credit unions focus on humanizing banking? Much of our world treats individuals like numbers, with minimal concern for the person behind the digits. Consumers want to spend their limited time on the people, experiences and things they find to be valuable. Financial institutions need to demonstrate their value for customers by personalizing engagements and interactions and building deeper connections.

No matter how quickly organizations delve into much needed digital transformation by using apps, CRMs, IVRs and chatbots, financial institutions cannot replace human-to-human connection for the pivotal moments people are expecting it — the consultative advice for those very important life moments.

Customers Who Feel Valued Stay, Spend and Advocate

With the increasing pressure from new entrants into the world of finance, banks, credit unions, wealth management firms and tax preparation companies all need to return to the crux of effective customer engagements: the emotion behind the experience through deeper relationships with prospective and existing customers.

Keep in Mind:

People want to be emotionally connected to their financial institution, yet only one in five consumers actually feel such a connection.

A Gallup research study found that the emotional connection is what keeps people coming back, with fully engaged consumers netting an incremental 23% revenue. However, that same research showed that only one in five people are actually emotionally connected to their primary banking provider.

You Can’t Manage What You Can’t Measure

We regularly discuss industry trends, upcoming challenges and internal processes with banking executives. It is surprising how seldom financial institutions track basic metrics to measure prospect and customer engagements.

Understanding what your meeting no-show rate is, how many walk-ins you have at each location per hour per day, what channel is most popular for which question, and what services are in highest demand, means your team understands how, when and where your most valuable engagements are happening and which areas require more attention.

Measuring engagement goes beyond a simple tally of how often a customer logs into a mobile app, calls into the call center, or visits a branch. Financial institutions need to be able to connect each of these touchpoints across all channels to records in a CRM tool to begin painting a picture of how an individual behaves as well as track how they want to be engaged with in the future.

Using technology is the only way financial institutions can begin to measure the engagements between staff and customers. Using analytical tools like Hubspot, Pardot and Google to track the customer behavior through digital channels, then pairing that up with vendors for the in-branch and appointment-based analytics, means the entire customer engagement journey is mapped. From the initial search query in Google, all the way through submitted paperwork via your central banking platform and customer records management like Salesforce.

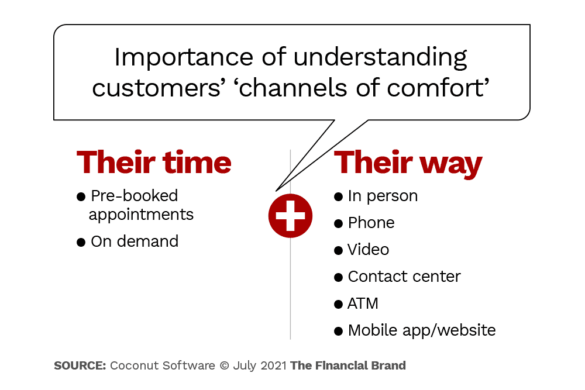

Engage In Individuals’ ‘Channels of Comfort’

Your customers have preferred channels — what we call ‘channels of comfort’ — that vary individual to individual, and can change based on the query they are trying to resolve. These channels include mobile apps, call center support, social media, ATMs, phone appointments, video conferences and face to face meetings in-branch, with most individuals using between three and four channels.

When customers are able to select and use their channel of comfort, their engagement improves significantly. Engaged customers spend more money and are more likely to stay with their bank and credit union. Research has shown that there is a serious mismatch between how financial institutions service customers and how those customers want to be served.

38% of respondents to a recent survey wanted a personal relationship with their financial instititution but only had a digital one, or vice versa, which resulted in them being less likely to fully engage with their banking provider by 47% compared to those whose preferences were being met.

Once you’ve established how those individuals want to be supported in their channel of comfort, determine what technology and processes are required in order to service them in those channels. The “thought that matters” concept only will take your customer experience so far — backing it up with operational execution to solve their queries is the only way to create true engagement.

In one of our studies, we found that 25% of banking executives are focusing on personalization in their engagements, meaning they’re asking customers how they want to be helped. What about those other 75% of executives? Are those financial institutions assuming they know what those customers want?

Or even worse, perhaps they don’t care enough to diversify their offerings into a variety of channels in the first place.

Different Activities Require Different Levels of Support

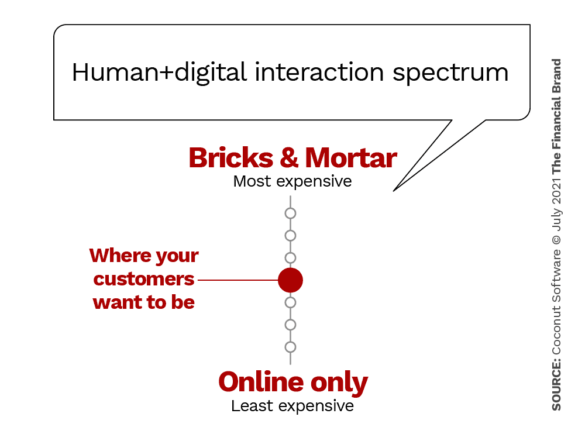

Coconut Software commissioned several studies in 2020 to better understand how banking customers want to engage with their institution. Our research found that customers and prospects want to be met somewhere in the middle of the digital/bricks and mortar continuum — encouraged to use digital options when low-value transactions can be completed, but welcomed into their local branches when advisory and life milestone discussions need to happen.

After all, money represents their dreams, their kids’ future, and is a reflection of their hard work.

Physical branches and the personal interactions they facilitate are still important for large and complex banking transactions, such as renegotiating a mortgage or taking out a business loan. On the other hand, many consumers are now doing smaller transactions like checking their balance and making deposits by using ATMs and banking apps. It is imperative for financial institution leaders to know when to automate and when to humanize interactions.

What to Aim For:

Banks and credit unions cannot focus solely on the digital experience, nor can they ignore consumer demand for mobile apps and online banking. Instead, banking providers should be seeking a balance between the two.

Match the level of support you provide to the level of complexity for that request. Don’t make opening a checking account more difficult than it needs to be, and see if you can support that activity through a less expensive channel, like a chatbot on your website. That way, you can focus your highly trained and highly paid in-person staff for truly advisory type support.

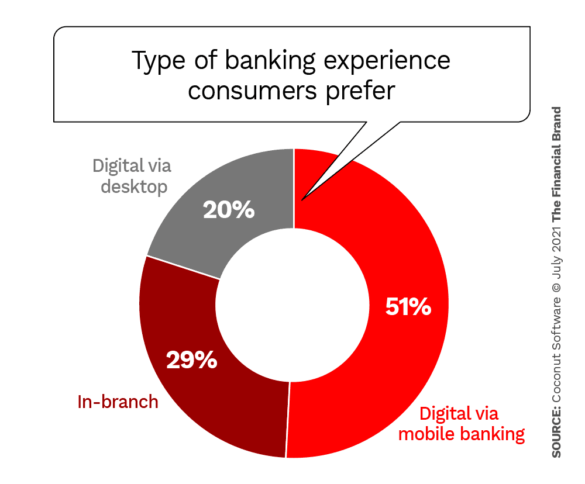

The chart above was created from a report we commissioned with Future Branches that asked banking customers their thoughts on how they prefer to bank with their financial institution. It showcases that the majority (51%) of individuals prefer a digital experience through a mobile app, followed by in-branch at 29%, and finally a desktop digital experience at 20%.

But the most interesting part is that 71% of those same respondents believe it’s important to build a relationship with banking personnel. What does this truly mean? For those transactional, day to day activities, consumers like the digital option. But when it comes to larger and more complex transactions, like buying a house or investing lottery winnings, people want to leverage the expertise and advisory services of your staff in branch.

Naturally, customer preferences must be weighed against the cost of supporting the various channels of comfort with significant differences in the expenses between them. Having someone book an appointment to deposit a single check into their checking account is a high cost for a low value transaction that easily could be automated through taking a picture on a mobile device via an app.

However for high value, consultative type of services like wealth management, insurance policies or mortgage negotiations that signify a significant transfer of funds or key life milestone, an in-person or virtual face to face prebooked appointment makes sense.

It’s absolutely imperative that you ask your prospective and current customers how they want to be helped, instead of assuming. After all, moving consumers from channels they prefer to use, to ones they do not, lowers their engagement and satisfaction: key reasons why people leave their financial institution.

The Key to Growth

Humanizing banking needs to become a transformative shift in how financial institutions engage with their customers in order to improve the experience and by extension, their market share.

A Winning Strategy:

It isn’t enough to endlessly create new channels for new products. Customers expect their experience between and across channels will be consistent, simple and valuable.

Improving your customer engagement is necessary to gain and retain market and share of wallet. Engaged customers are key to growth in 2021 and beyond, especially considering the complete digital transformation currently underway in the financial services space.

Ideally, banks, credit unions, wealth management firms and tax preparation companies will be able to bridge the digital and physical channels to create a seamless banking experience, with little friction for people when they move from online to bricks and mortar, then back again.

If your financial institution gets a good handle on these considerations, you’ll be well positioned to balance between digital and physical, providing consistent value to your customers. And treating them like humans.