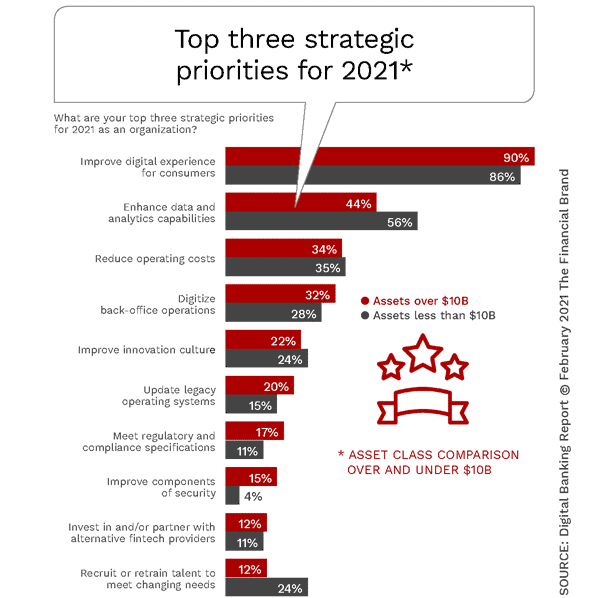

Having digital functionality for all aspects of banking is no longer optional. While many small and mid-sized financial institutions hesitated to invest in digital, Covid-19 forced the entire industry to provide consumers digital options where they did not exist previously. As consumers shifted their entire daily lives to digital channels, expectations for digital experiences rose exponentially almost overnight.

Simply providing digital capabilities was no longer enough. Consumers wanted engagement to be as fast and easy as the leading big tech and fintech companies. Leading banks and credit unions have focused on reducing the friction for online and mobile account opening, loan applications, transfer of funds, and other essential interactions by reducing the steps that had always been a component of in-person banking.

As physical branches have begun to open, financial institutions are also beginning to reinvent in-branch experiences, reducing friction and considering new ways for consumers to interact with branch personnel. Since it is not expected that branch traffic will ever return to pre-pandemic levels, organizations are also testing different roles for existing employees, focusing on how teams can be used to humanize digital experiences beyond the branch. One way this is being done is to use data and analytics to create personalized product and service recommendations that can be delivered by branch personnel in real time, supplementing other channel messages.

To find out how the definition of customer experience (CX) has changed since the pandemic, and how banks and credit unions can adjust to the new expectations of consumers, I interviewed Jay Baer. As the founder of Convince & Convert, Jay is one of the foremost leaders in the world of customer experience and marketing.

During this interview, Jay discusses how financial institutions need to reset their strategies around improving CX in a digital world or else lose business to non-traditional financial services providers. He shares insights about how the competition has expanded, and how consumers understand what is possible.

In reference to the impact of the pandemic, Baer states, “Anything that requires an extra bit of time, thinking, or effort to overcome, customers have very little patience for nowadays. In a world where everything has been turned asunder, the last thing consumers want to do is spend 10 minutes filling out screens to open an account or to search for the submit button. People just don’t care what your organizational challenges are to make things easy.”

Read More: The Evolution of Banking

The Importance of Exceptional CX

For more than seven years, financial institutions of all sizes have consistently ranked ‘improving the customer experience’ as their top objective as part of the Retail Banking Trends and Priorities research published annually by the Digital Banking Report. Despite this perennial top ranking, consumers do not see the banking industry in the same light. In fact, more consumers than ever are ‘testing the waters’ with alternative providers and have downgraded their level of trust in traditional banking organizations.

The value of a strong customer experience is based on the opportunity to generate more and better customer relationships and to avoid losing relationships due to lower customer satisfaction. With so many options available to consumers, the ability to grow – or abandon – an existing relationship is as quick as a push of a button on a mobile device. In many cases, an existing relationship isn’t closed completely, but new accounts are opened and relationships built with alternative providers.

Excellent customer experiences are built with a combination of several integrated components, including: personalization and relevance, seamless omnichannel engagement, customer care (ability to provide answers and resolve issues), digital simplicity and speed, fairness and transparency, and even the way employees are treated. These components are not all inclusive, though.

We Are in an Era of ‘Empathy Deficit’

Before computers and mobile devices, the way a business succeeded was often by providing a personalized experience that was centered on treating customers with kindness, dignity, respect and empathy. This was the default setting that revolved around the face-to-face experience people had in a corner market, retail store, gas station and financial institution. While computers and digital devices were intended to automate this level of customer care, the impact was often the opposite.

Jay Baer, founder of Convince & Convert

“Somewhere along the way we lost our way, and now we find ourselves in an era of empathy deficit in business, in life, and certainly in politics, treating one another with kindness, respect, empathy and humanity is no longer the default setting,” stated Baer. “This reduction in personalized care is an enormous opportunity for financial institutions, however, because many customers do not expect, nor do they anticipate, that you will treat them with that human touch.”

Until recently, consumers simply expected a lower level of customer experience from their financial institution. Baer thinks the acceptance of less than exceptional experiences is changing though. “People used to say things like, ‘You know what? That’s a pretty good experience for a bank.’ Nobody says that anymore because they don’t care what industry you’re in.”

Reality Check:

73% of consumers now say that an experience with one organization changes their expectations for all other organizations.

“The Apple card is a great example. Apple is an organization that is well known globally for making things easy and sanding off rough edges. Now, they have a credit card that can be applied for on four screens, and as little as three pieces of information – in less than a minute. It’s not that huge of a stretch to say, ‘how about opening an Apple checking or Apple savings account with a single click?’ Apple has set the standard for all industries.”

Read More: The Future of Customer Experience in Banking is Personalized

Customer Expectations are Permanently Altered

When you look at customer expectations, they obviously changed tremendously since the pandemic began. Many financial institutions are wondering if the changes we have seen will be permanent.

“Everything from a digital transformation standpoint was going to happen anyway. It just happened five years faster than it was going to. I’ve never, ever, ever in my whole career seen customer expectations move backward. So, customer expectations aren’t going to revert to historical norms. They just may not ratchet up again quite as quickly as they might have since Covid.

One of the most significant shifts in expectations has been around speed and simplicity. From ordering groceries from a phone, to using a mobile device to deposit a check, consumers are enticed by apps that can save them time and make their lives easier. “Think about Amazon one click, which didn’t use to exist. You can now buy almost anything without going to a website – directly from your phone – in seconds. But it is often very complicated to make something simple.”

For most financial institutions, the challenge is often built into the organization. There is the desire to exceed customer expectation, but legacy technology, processes and even leadership holds the organization back. As Baer explains, “The challenge with banking and financial services is that you’ve got an ‘experience balloon’ that both the bank and consumer want to go higher. But the balloon is tied to legacy strings, including software, processes, and even a recalcitrant board of directors. Organizations need to commit to go get some scissors.”

Read More: Now is the Time for Intelligent Digital Banking Experiences

The Importance of Brand and Purpose

While 2020 will be most remembered for the pandemic that gripped the world, there were other crises that multiplied the impact on consumers and businesses. The pandemic resulted in lost jobs and closed businesses, a heightened awareness of how climate can be altered quicker than anyone imagined, and how social issues can raise expectations of brand responsibility to the communities they serve.

Beyond speed, simplicity, transparency and cost, consumers are increasingly wanting to do business with organizations that have made commitments that are in alignment with beliefs they have themselves. Brands seen to be stalling or acting out of alignment to what they say in public will be called out, and suffer the financial consequences. Of heightened importance are issues surrounding economic and social inequities, diversity in the workplace, support of small businesses, a commitment to the environment, among others.

Key Fact:

49% of consumers have boycotted brands that have different values than theirs (Ford and Harris Insights).

“People are making buying decisions more than ever based on criteria that are not price dependent. They’re making decisions based on brand values. People care about what companies stand for in a way that is unprecedented in the history of the United States,” stated Baer. “But you still need to get the basics right. Every brand has a set of brand values until they screw up something basic, and then the customer doesn’t care what the brand values are”

There are examples of brands that have taken positions that have resulted in lost customers, but gained them loyalty among aligned constituents. “Nike was one that really got everybody to open their eyes,” Baer mentioned. “It is a massive global corporation that is embracing a particular set of values … that is costing them customers. But it’s obviously gaining them more customers because the stock price is way up and their results are way up.”