Top Brand Experts Identify 5 Critical Issues Facing Bank Marketers

Tech-enabled niche competitors are putting pressure on traditional financial institutions to adapt their products, messaging and culture to a very different mix of consumer views and expectations — and do it without abandoning core ethical and trust values. Customer loyalty is at stake, but in the view of these experts, the opportunities are as big as the risks.

By Bill Streeter, , former Editor-in-Chief at The Financial Brand

Simple Subscribe

Subscribe Now!

Brand is one of the most misunderstood concepts in business, but also the single most important thing to grasp. And yet, even now, many in banking miss the full significance of brand.

There’s a tendency to lean toward messaging, logo and taglines when talking about brand, or to focus on products, advertising or pricing.

As covered in articles on The Financial Brand, people use brands as a form of mental shorthand, to summarize all the things that pop into their minds when they think about a company or a product. Try it out: What comes to mind when you think of Southwest Airlines, Apple, Walmart, Ally Bank, Wells Fargo?

Every interaction with consumers influences how they think about you. Each represents an opportunity to build or reinforce your brand. That’s why all the emphasis in recent years on “experience” is so important. Ultimately brand is about what you do, not what you say.

Melanie McShane, Senior Director of Strategy at brand consultancy Siegel+Gale, made a very telling observation during an interview: “The most important thing about brand is what people say about you when you’re not in the room.”

Difficult to measure, but that’s the real deal.

“Products come and go, branches, networks and bankers come and go,” says McShane. “But the brand is the consistent relationship with a customer. You want to nurture that — it’s at the heart of the organization.”

Great points. But what will help take them from a distant goal to a tangible reality that banks and credit unions can build on? To find out, The Financial Brand spoke with McShane and also with Robert Passikoff, Founder and President of Brand Keys, both experienced brand professionals at respected firms, in separate interviews.

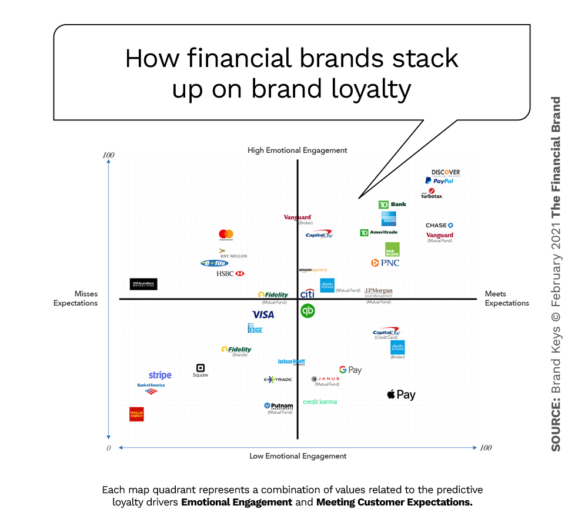

Just prior to the conversations, Siegel+Gale issued its annual list of brand predictions for 2021. Likewise, Brand Keys released its 2021 Customer Loyalty Engagement Index. The index identifies “emotional engagement” and “customer expectation” as the two primary drivers of customer brand loyalty for financial institutions and other brands.

The comments of these two brand experts point to five broad areas that bank and credit union marketers must address.

Trend 1. The Growing Importance of ‘Inclusion’ as a Brand Factor

The social unrest that roiled the U.S. in 2020 did not go unnoticed by financial institutions. Various messages of support and commitments to fairness from banks and credit unions appeared in social media and other advertising mediums. To McShane, however, there remains a disconnect between the experience that someone may have as a customer versus what they may see in an ad.

“Many communities within the general population have not only been underserved by financial institutions,” she maintains, “they’ve actually been mis-served — sold products that weren’t appropriate for them or charged rates that varied according to their race or their orientation.”

“What we’re finding is that consumers are comparing not just within financial services,” McShane state, “they’re comparing their experiences across various business sectors. They’re demanding that brands not only recognize them, but treat them with respect.”

The consultant points to a growing list of new financial brands specifically targeting such communities, including Daylight, a LGBTQ-owned bank and First Women’s Bank.

While minority- and women-owned banks have not faired well historically, McShane believes that today’s technology allows these niche players to scale much faster. In addition, many of the barriers to people switching institutions are being removed, she maintains.

“You’ve got this kind of cocktail of consumers’ being able to switch providers more easily, having higher expectations and having better choices. All of which is something that financial institutions need to be thinking about.”

— Melanie McShane, Siegel+Gale

McShane says that in the conversations her firm is having with clients sustainability, diversity and inclusion are all “near the top of the list.”

Reality Check:

Shouldn’t branding be more about timeless human issues?

McShane responds that CSR issues have moved away from being seen purely as political issues to being human and commercial issues.

Robert Passikoff, however, says that while the key drivers of brand loyalty do change over time, certain values have not changed significantly for financial institutions. These are trust, confidence and ethics.

“Corporate social responsibility (CSR) is generally a value that people factor in,” Passikoff maintains, “but it’s less important than trust or privacy issues, for example, which are big contributors to brand loyalty in banking.” Things like inclusiveness and sustainability don’t factor in that much, in his view, or at least not across the board. They are more relevant to Gen Z, he agrees, but less so with Boomers or even Millennials.

Trend 2. Meeting Expectations is a Brand Must

As noted above, Brand Keys research found that, the ability to meet fast-changing consumer expectations is one of two key drivers of brand loyalty. The firm states that consumer expectations are rising 22% a year. That rate has accelerated, driven by innovations in many product categories, not just banking, Passikoff explains.

“Product categories are not walls. Yes, banking is different than selling online shoes, but there’s no one out there that’s just a consumer of banking.”

— Robert Passikoff, Brand Keys

One changed expectation, he points out, is speed of response. People think, “Since someone else will get back to me in an hour, why are you taking a day?” Because people were forced to bank mostly online as branches were restricted during COVID, their expectation was that things would be much quicker digitally, says Passikoff. But that was not always the case with many financial institutions.

“‘Expectation’ is the gap between what consumers desire and what brands deliver,” Passikoff states. Recognizing that gap, however — if it is identified accurately —provides banks and credit unions with an opportunity to close it.

“That’s what innovation is all about,” says Passikoff. “Brands that are able to do that will do very well.”

The financial brands in the upper right-hand quadrant of the chart below excelled at meeting expectations in addition to creating emotional engagement.

Trend 3. Importance of Emotional Connections

In a world where the majority of consumer interactions are becoming digital, McShane says that financial brands and other companies she’s working with are asking, “How can we make sure there is an emotional layer in the digital experience that we’re providing?” They recognize they can no longer rely solely on the in-person interactions to deliver that personalized, warm, “I understand you” experience, she adds.

Much like tele-medicine, McShane expects to see a lot more human experiences inside digital banking interfaces.

Passikoff gives two examples of how emotions factor into brand engagement in banking. With fees, the rational value is “How much is the fee?” The emotional value, he says, is how a person sees themselves as being smart in managing their finances.

The second example relates to the advanced digital apps that some banks and credit unions now provide. Equally important as specific features is the emotional perspective of “My time is valuable, so I don’t want to waste it going through some clunky banking process.” The application must work intuitively.

Trend 4. Never Take Loyalty for Granted

Based on many years of research, Passikoff states that loyal customers are six times more likely to behave positively towards a brand. That can include being less likely to leave for a better offer and being much more willing to give an institution the benefit of the doubt in difficult circumstances.

“That well of forgiveness is not bottomless, however,” observes Passikoff. He cites Wells Fargo as a prime example. The bank’s series of client abuse disclosures has left it low on the loyalty index chart shown above, and has clearly impacted its momentum over several years.

Despite the benefits of loyalty, marketers must recognize that having loyal customers doesn’t mean that they are not going to try something else.

“Novelty will get people’s attention,” Passikoff states. “The pandemic has opened people’s eyes to many other options.” That has led to huge increases in the number of users of fintechs such as Chime and Robinhood.

What financial marketers should expect to see is a much more segmented banking sector, says Passikoff, as people find that a new financial application works better for them than what they have at another institution. As a result, more consumers will maintain multiple financial relationships, where before they had just one or two.

Trend 5: A Return to Core Tenets

Dealing with the above brand trends will prove challenging for financial institutions that are still wrestling with the shift from product centric to customer centric organizations, but McShane believes this period of transformation — as much cultural as digital — will ultimately help propel banking to a newly creative position.

In fact, she feels the biggest area of differentiation could be a return to some of the core tenets of banking that have fallen by the wayside during the long run-up to digital banking. She describes this as “deep personalization and the type of relationship you can have as a result of really knowing somebody, understanding them and showing them that respect that I spoke of before.” Much of it of course will be done online or by mobile device, but in a way that’s proactive, yet not annoying or salesy.

“It’s an exciting time to be innovating in the banking industry,” McShane concludes.