Rumors surrounding the death of physical branches have left many banks financial institutions scrambling to find the right mix of delivery channels. Along with predictions of smaller branch footprints in the future, experts have emphasized the need to rethink the function and role branches will play moving forward.

But what if you could just drop a portable branch off in high-traffic, populated areas whenever needed? Imagine locals buzzing about your branch, and offering suggestions on where it should be located next? Or if you could put your branch where it was needed most after a natural disaster?

In the new omni-channel world, could pop-up branches like these be the answer banks and credit unions have been searching for? You have to admit, there’s something appealing about being able to quickly set up shop then trucking it to a new spot once it’s served its purpose.

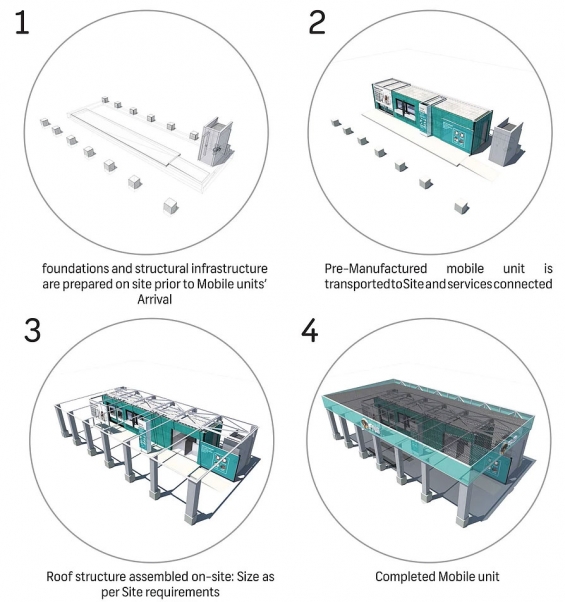

These micro-branch designs — many created from shipping containers with a footprint measuring 160 square feet or less — are a cost-efficient way to scope out areas where a more permanent branch location might be warranted. If one location isn’t getting the anticipated foot traffic or generating enough revenue, no big deal. It’s just one forklift away from being relocated.

Many of these pop-up branches are designed to serve as full-service branches. Believe it or not, a 20’ x 8’ container can house 24-hour ATMs, issue debit cards on the spot, open new accounts, and handle loan applications. Consumers can get information on lending and deposit products by speaking to a universal banking representative who is ready to help with an iPad and a smile.

And a pop-up micro-branch is not only cheaper to build and operate, they can generally be ready to go within three months. How much cheaper? It depends on its size and scope; it’s purpose and goals; the technology, equipment and accessories that will be installed; and how often it needs to move. Logistics and transportation are another consideration. Will a self-offloading trailer, forklift, crane or hydraulics system be needed? Then you have to think about permitting.

Several banks in the U.S. and other countries have been working pop-ups into their branch network strategies.

Since 2013, PNC Bank has incorporated pop-up branches in its facilities mix. Experimentation within its branch network has been an integral part of PNC’s multi-year customer experience strategy. In July 2016, PNC set up its first “tiny branch” pop-up on a college campus at West Virginia University, where it stayed for the next five months. To raise awareness of its tiny branch, PNC’s staffers could be found during finals week handing out free cups of coffee, or offering free rally towels around game days.

“Branch convenience remains the number one consideration when consumers choose their primary bank,” explains Jim Balouris with PNC Bank. “A tiny branch is a fun, creative way to bring a host of services that help customers discover ways to enhance their financial wellbeing.”

In Australia, banks such as National Australian Bank and Commonwealth Bank utilize pop-up branches as temporary hubs for customers recovering in the aftermath of devastating floods, fires and storms. The stores also come in handy when there are delays in the opening of permanent brick and mortar branches.

NAB’s modular stores consist of three different sections: the sales room, service area and a transaction zone. They take only 90 minutes to assemble, and run on generators.

In South Africa, FNB joined forces with Johannesburg-based architects A4AC to deliver banking services to unbanked rural communities. Each branch includes modules for an office, teller windows, ATMs, and a branded exterior.

“South Africa still has a large section of the population that has limited access to banking facilities and we want to turn this around,” Lee-Anne van Zyl, CEO of FNB. “The first step for us was to think about an innovative way of delivering a full suite of banking facilities to rural communities in a convenient fashion.”

Even digital-first direct bank Tangerine has found merit in expanding its physical presence beyond their signature cafés.

In 2015, the bank launched a pop-up pilot with two locations in Toronto and Brampton. Now up to five pop-ups, the engagements can run anywhere from six to 12 months.

With an eye on attracting new customers, the portable branch is equipped with iPads loaded with Tangerine’s “Sign Me Up” app, which allows customers to sign up for an account by simply scanning their passport or driver’s license. Customer service agents are on hand to provide assistance, not to conduct any transactions.

“Since we’re a direct bank, our pop-up locations allow us the opportunity to showcase our unique everyday banking experience to potential clients in new markets who may need a little extra nudge to help discover what we’re all about,” says Phil Taylor, VP/Service, Sales & Retail experience at Tangerine. “We view ourselves as innovative retailers that happen to be in banking and I think pop-ups really support that approach.”