The old, invented quote attributed to Willie Sutton about why he robbed banks — “Because that’s where the money is” — serves to illustrate a problem with the accepted wisdom that the future of the branch is all about advice and counsel. To consumers, the branch is still perceived to be where the money is… literally. The idea that a branch could serve mainly for consultation, a place to go to get the best thinking about your money, is not something most consumers are anywhere near accepting, yet, except perhaps for opening new accounts.

In fact, recent research by Shikatani Lacroix Design found that few consumers surveyed think about banking institutions as a source of advice. Banks have pushed the idea of bankers as advisors for decades. But apparently for many Americans that idea has little traction. The design firm’s research finds that friends and family serve as advisors far more often than financiers.

In many ways, one might reasonably think that bankers and credit union executives would have a strong sense of how to promote the idea that skilled advisors await puzzled consumers. But consumers rarely see that side of the industry publicized. Go to most institutions’ websites and you see product, product, product. Much of what is advertised concerns rates or seasonal product promotions. Comparatively few institutions explicitly market their advice or their problem-solving abilities.

And this failure to communicate extends to many financial institutions’ retail office floor plans. “The first thing you notice in the branch experience is the fact that there is a teller line,” says Jean-Pierre Lacroix, President and Founder of Shikatani Lacroix Design. “And the things that drive revenue for a financial institution —wealth management, loans and mortgages —are not visible.”

Teller lines still stand out, when more and more routine transactions are digital and usage of cash has fallen.

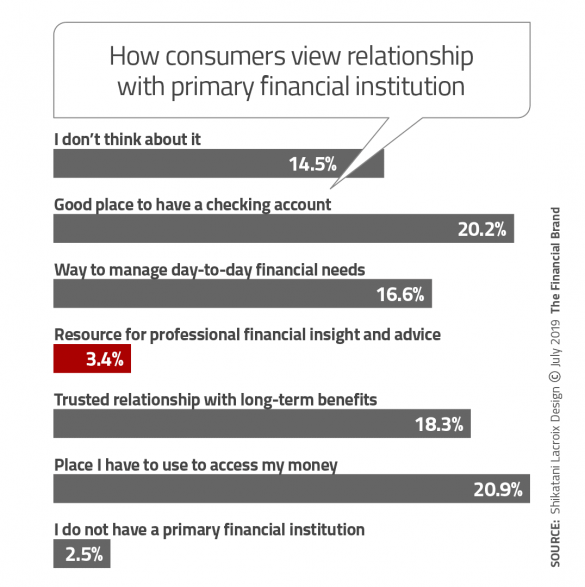

“It’s startling when you think about it, that 96% of respondents view their bank as a place to access money or conduct transactions,” says Lacroix. “So when you need to flip that perception on its head — where the key reason for them to come to the branch is for financial advice — you need to think very differently.”

Quality of advice is also a factor, which demands improvements in recruiting and training. The firm’s research found that only 38% of consumers surveyed are happy with their institutions’ financial advice.

Read More: Trends in Branch Design From Banks and Credit Unions Around The World

Branch Change Will Never Stop

Lacroix’s firm has been studying the branch challenge from multiple perspectives and has produced an ebook, Think: The Future of Retail Banking: Six Strategies to Future-Proof Branch Networks.

A key overall argument Lacroix makes in Think is that bankers and credit union executives must stop thinking of branch transformation as an event to work towards and then relax. Much like modern retailing, the tension between channels will continue — and will evolve continually, so that transformation will reside permanently on institutions’ do lists.

In fact, Lacroix suggests that as branch systems evolve, executives must be asking “what’s next?” long before the status quo becomes obsolete. When obsolescence becomes obvious to providers, it’s long been so to consumers.

“We are looking at a shift, to a vertical ecosystem that provides more than just banking services.”

— Jean-Pierre Lacroix, Shikatani Lacroix Design

Asking the questions early is what Lacroix refers to as “future-proofing.” He argues that because financial institutions must make major investments to change branches, deployment of new concepts should be gradual, in order to test reactions and learn from mistakes. To stay ahead of things, he advocates for coming up with scenarios to stress-test branch systems for different types of change. Institutions can then make course corrections or reboot strategies entirely based on what such projections show.

But the strongest example of thinking differently in the designer’s book is his view that institutions should no longer build their branch networks around general purpose branches. Ideally, Lacroix says, the branch, while incorporating many new ideas no matter its purpose, should be tailored to a specific market.

“Ultimately, we view banks going from a one-size-fits-all model to targeting unique personas and groups,” says Lacroix. As this model, or set of models, comes into use, “we are looking at a shift, to a vertical ecosystem that provides more than just banking services.”

Lacroix believes that institutions must pay more attention as well to building emotional connections with consumers and businesses banking with them.

Perhaps someday “robots will be able to relate to humans on an emotional level,” writes Lacroix. “Until then, driving emotional engagement can only be achieved through people who are focused on delivering empathy and building rapport through human interaction.”

Read More: Are Tiny Pop-Up Branches Banking’s Brick-and-Mortar Future?

Rebuilding Branches as Advice-Centric Ecosystems

Ecosystem is one of those words that get over used. But Lacroix sees the packaging of advice and services around specific markets’ needs as a key to keeping branches relevant and to increase their utility. This applies to multiple consumer and business segments.

“Customers increasingly need to feel recognized on a deeply personal level and want more from their banking experience, including additional services in a convenient, cost-effective model,” writes Lacroix. “This new model will reframe the definition of a target group, moving from the current approach of offering the same services in different retail footprints to offering curated and highly personalized services.”

“Staff will evolve to become a combination of life coach, mentor, advisor, and collaborator to help deliver a customized set of services and products for each customer.”

— Jean-Pierre Lacroix, Shikatani Lacroix Design

Branches organized as ecosystems, says Lacroix, will come to be seen as a center for a community. That community may not be geographic, but instead organized by interests.

This new model allows financial institutions to offer more consultation, according to Lacroix, potentially increasing revenue. He suggests that specialized branches could increase loyalty and in time turn people banked by such locations into brand advocates.

The designer describes four ideas for ecosystems, incorporating both functional design elements as well as ideas on the look for each ecosystem. Lacroix and his team suggest applying “phygital” concepts to each model, incorporating interactive digital screens in tabletops and walls where and as appropriate,

Lacroix envisions manufacturing the variations on branches as modular structures that could be sited by themselves or hooked to a hub structure serving one or more other branch variations. He likens this to having banking Lego parts. Capsulizing the concepts:

• Small Business Ecosystem. This concept almost sounds like a mini conference center with collaborative work spaces and private consultation areas for meetings with bank advisors. “Rather than feature staff seated behind a desk, financial experts and advisors move throughout the space, which is designed to allow for private meetings but encourages casual, spontaneous interaction.”

Lacroix sees this as an important component going forward because Millennial and Gen Z consumers, as a group, tend to be more entrepreneurial and interested in opening their own businesses than earlier generations.

The firm’s research indicates that 42% of respondents would like some form of one-stop advice for small business, going beyond financial services. Among the advisory services a sizeable portion of the sample wants to be able to tap digitally or physically are tax advice, HR services, and marketing assistance.

Read More: Banks Should Turn Branches Into Branded Coworking Community Spaces

• Family Ecosystem. The target community here is the young Millennial family, with tiered levels of privacy available and space allowances based on the expectation that for some financial matters a consultation might involve not only the couple, but potentially toddlers in tow. At other times parents or grandparents might come along. Overall, family-oriented branches and wealth management branches designed for retiring Baby Boomers would feature more private space than the small business branches.

For these branches, Lacroix thinks a stress on residential colors and seating will best put consumers at ease in spaces where they will meet with advisors. Meeting rooms would have floor plans like cafés, to put consumers at ease and to let them comfortably and privately talk prior to the advisor entering the room.

• Incubator Ecosystem. Taking the business branch concept a step further, this variation would be designed for startups and provide more training space for young entrepreneurs. Experts to advise them would not necessarily be on premises, being able to address them via electronic whiteboards and other digital connections.

• Wealth Management Ecosystem. This variation would incorporate elements of the family branch, but would add a second floor with private offices designed to serve wealthier Boomers planning their retirements

In all of these situations, Lacroix believes, surviving institutions will need to raise the capabilities of their staff. Being centered on the advisory function requires genuine expertise.

“Staff will evolve to become a combination of life coach, mentor, advisor, and collaborator to help deliver a customized set of services and products for each customer,” Lacroix says.