Stock photos of Generation Z that financial marketers often include stereotypical shots of smiling youth in cliché poses and quintessential hairstyles. They’re glued to social media, taking selfies. They seem to have no cares and look like they’ve got it all figured out.

But in reality, this generation is stressed-out. One of the top stressors? Money.

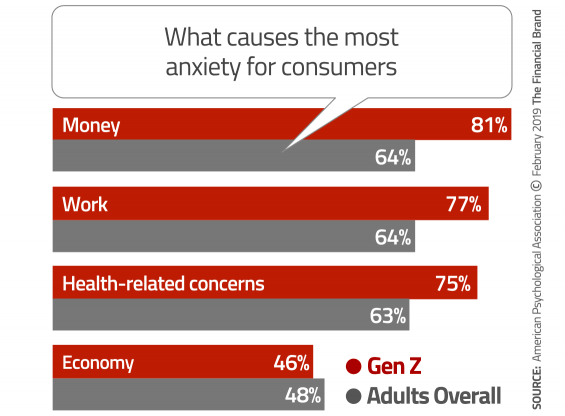

According to the American Psychological Association, four out of five Gen Z consumers ages 18-21 say money matters are a leading source of stress. In their study, more than three in ten Gen Z respondents, personal debt is another major source of stress.

Many members of Gen Z enter college lacking in essential financial management skills, increasing their stress and exposure to personal financial risk. It’s not that they haven’t had any preparation, but that they seem to lack skills where formal financial literacy training meets common sense practical application. Yet their college years, more than ever before, will include financial decisions impacting much of their future adult life.

“Many young adults heading to college do not feel prepared to handle their impending financial challenges.”

“Many young adults heading to college do not feel prepared to handle their impending financial challenges and those unprepared students are more likely to experience financial stress,” observes EverFi in their report on Gen Z. “Many of today’s young adults are struggling more than older generations with basic money management and overall financial skills.”

The EverFi study included a short test of financial literacy practical basics that Gen Zers frequently got wrong:

- Only 14% know they should have 6-12 months expenses in emergency savings.

- Only 29% understand that someone with too many credit cards must close the accounts carefully to avoid hurting their credit rating.

- Around half don’t know how to compute their net worth.

- Four out of ten don’t know that a late payment sent to a collection agency would stay on their credit history six years or more even after it is paid.

- Most have no clue how to tell if inflation was outpacing their return on savings.

EverFi says this data paints a rather uninspiring picture. The report suggests that school training in personal finance and economics tends to be seen as an academic requirement, with less emphasis on producing actual financial capability. As evidence of this:

- Four out of ten students with checking accounts admit that they haven’t checked their balance in the past year.

- Four out of ten haven’t created or used a budget.

- One out of four buy things to improve their mood.

- 10% admit to buying things they can’t afford.

- Only six in ten say they stop spending when their resources are low.

( Read More: Gen Z Means More Digital, Mobile & Social for Financial Marketers )

Optimistic Generation with Share of Challenges

A study by Charles Schwab indicates that Gen Z aspires to financial independence but often falls short of the mark. And while they are savvier in some ways about money than other generations, things haven’t always gone smoothly for them.

“Four out of ten Gen Zers have borrowed from their folks to pay for necessities. One in four have borrowed from friends.”

Gen Z harbors high hopes in spite of a rocky beginning. 76% think they will have a better financial future than their parents did — 81% saw their parents experience financial hardship during the Great Recession.

Schwab’s research indicates that Gen Z is having trouble making ends meet. Four out of ten have borrowed from their folks to pay for necessities and one in four have borrowed from friends. And three out of ten have had to skip a meal due to lack of funds.

About half of the young people surveyed have some type of debt, with the average amount outstanding coming to $8,000.

Financial independence is very important to this generation. About 20% have achieved this already. Among the rest, they hope to be independent within five years, typically. However, 12% anticipate that they’ll be supported by their parents indefinitely. Yet about half of those surveyed have less than $250 saved — on average, they’ve saved $1,628.

Who Gives Gen Z the Best Advice?

Members of Gen Z have the deepest, widest pool of potential financial advice any generation ever had, ranging from social media influencers to parents to websites to financial literacy programs to apps to each other. While research indicates that influencers are a frequent go-to, Gen Z will just as likely turn to a peer no more experienced than themselves.

Some have suggested that educating influencers in financial subjects could help spread knowledge among the influenced. Likely not, one study suggests. A research paper by the National Bureau of Economics found that when education was introduced among its sample, the peer who did not receive the training typically only mimicked the behavior of the peer who instructed them — they didn’t actually absorb the knowledge.

The study also suggests that when someone can choose their peer, that might make a difference, because they could avoid individuals who appear to set bad examples.

( Read More: 6 Keys to a Best-in-Class Financial Wellness App With Data and AI )

Opportunity for ‘Financial Wellness Coaches’

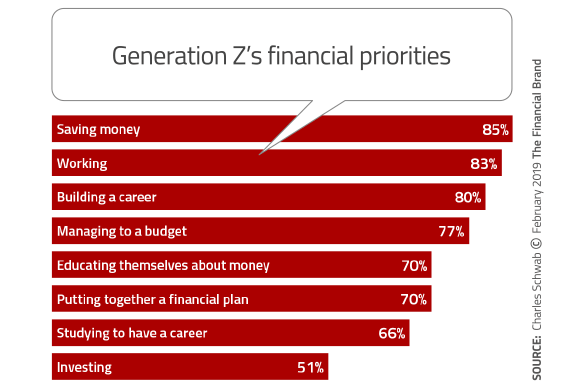

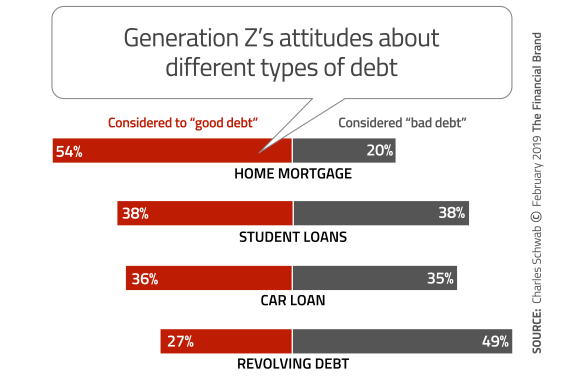

The Schwab research portrays a generation that craves a better understanding of finances. 70% say that educating themselves about money is important to achieving their goals. While family tops the list of trusted source of financial information at 39% — for nine in ten, what they know about finances came from their parents — financial institutions come in second in the survey, at 25%. The Schwab study indicates that banks and credit unions that want to help this generation can start by offering education about how to distinguish between “good debt” and “bad debt.”

If financial literacy programs in the educational system don’t always stick, what else can be done? To the degree that employers get involved in employee financial preparedness, it is typically concerned with retirement. Thing of it is, you have to be solvent when you get there.

PricewaterhouseCoopers notes that financial stress impacts the workplace. “The effect of financial stress on worker productivity is striking,” PwC says in its “Financial Stress & The Bottom Line” report.

“Employees who are stressed about their finances are nearly five times more likely to be distracted by their finances at work, twice as likely to spend three hours or more at work dealing with financial matters, and three times more likely to spend five hours or more,” according to PwC. “Stressed employees are also twice as likely to miss work on account of their personal financial issues and are more inclined to cite health issues caused by financial stress.”

Much of the stress found by the firm’s researchers arises through an over-dependence on credit cards. Another key source of financial stress is failure to build and maintain adequate emergency savings. The report notes that emphasizing retirement savings in financial wellness program content is premature for many.

( Read More: The Financial Gym – Pumping Money Out of Financial Education Programs )

“It’s imperative to address emergency savings,” according to PwC. “In fact, in some cases, it’s necessary to prioritize building an emergency fund over saving for retirement. Otherwise, all too often, we find that employees are raiding their retirement funds to cover immediate cash emergencies, thereby undermining efforts to achieve retirement readiness.”

PwC says that what employees want most is a personal finance coach — real people, not online/technology-based solutions. Personal financial advice often needs to be very specific, something a tech approach can’t always pull off.

Is one-on-one financial wellness something banks and credit unions should offer? Actually, many institutions large and small have already ventured into this, some going through employers, some offering it to consumers directly. In a blog on this by the Media Logic agency, there is this advice for financial marketers:

“Although financial education certainly benefits the consumer, it can also play an important role in defining (or re-defining) a brand. The effort, therefore, must be part of the overall marketing and branding strategy. It’s a good idea to align the brand with financial wellness and send a signal to consumers that you’re not only a valuable resource but also, perhaps, a valued partner. However, you’ll want to be certain the approach you take — a low-key conversation or a boisterous multi-city tour — works in support of your brand in a way that advances the company toward its business goals.”