“Personalization” is not a new or novel concept in banking. For centuries, financial institutions have prided themselves on the personal experience they delivered to each customer. But this CX strategy was easier to implement when physical branches were the primary — and sometimes only — touchpoint banking providers needed to worry about.

With the rise of digital, however, everything has changed. Banks (and even many credit unions) are now embracing data analytics to try and understand and predict consumer behavior. They mine user-specified preferences and fixed attributes such as age and income to shape various interactions. But this is just the beginning, says global consulting firm Accenture. They argue that basic personalization strategies must now give way to a new concept, one they call “hyper-relevance.”

According to Accenture, a new, hyper-relevant approach to CX should much more fluid and elastic, evolving as both consumers and their circumstances change. Financial institutions must delve deeper into the context of people’s purchasing decisions, and truly understand where each customer is in their buying journey.

In a 20-page white paper, Accenture says that investments in CX tools and technologies supporting a hyper-relevant strategy is the only way banks and credit unions can keep pace with consumers’ “non-constants” (i.e., their changing circumstances). In a hyper-relevant world, every interaction a financial institution has with a consumer should serve as an opportunity to learn more.

GAFA: Hyper-Relevant Role Models

People spend an average of 50 minutes per day on GAFA platforms, and half of consumers say they would bank with a tech firm.

— Accenture

Today, 76% of banking CEOs believe that it is “more important than ever” to provide products, services, and experiences that are very relevant to customers at different times and in varying contexts. This is, in large part, thanks to the pressure they feel to improve CX coming from other sectors like the retail, technology and travel industries. In fact, four out of five banking CEOs say customer expectations are being shaped by hyper-relevant, real-time, and dynamic experiences encountered outside financial services sector.

For financial institutions that want to take accelerate and amplify their approach to personalization, Accenture points to bigtech pioneers like Google, Amazon, Facebook and Apple (GAFA) as role models. You could throw Netflix in the mix as well, along with companies such as Baidu, Alibaba, Tencent/WeChat, Uber and Airbnb — all who have redefined the way in which companies and their customers interact with one another.

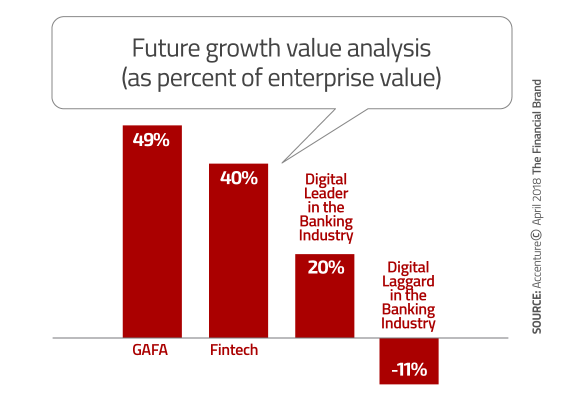

After all, when it comes to creating value through hyper-relevance, GAFA companies are in the premiere league. The growth potential of these tech giants blows away even the most digitally advanced financial institutions, with the future valuation of GAFA organizations more than double that of banking’s digital leaders. And if you’re a digital laggard in financial services? Well, Accenture predicts their future prospects look dire.

“A hyper-relevant financial brand is distinguished by the way it ‘walks and talks’ in very human-like ways, much like how you would describe a friend.”

— Accenture

Part of this revenue growth hinges on changing the predominant mindset that has driven the internal culture at traditional banking providers. Rather than seeing GAFAs as competitors, banks and credit unions should view them as additional channels they can use to sell products and services to consumers (think: JPMorgan Chase and their budding romance with Amazon).

To achieve hyper relevance, Accenture has identified five “human-like” ways in which financial institutions must adapt in order:

- Engaging – Help people navigate life’s choppy waters by looking out for their financial well-being. Look ahead and provide valuable advice — both financial and non-financial, in the physical and digital world.

- strong>Intelligently Personalized – According to Accenture, nearly half of customers want relevant advice and product information at their fingertips as they go about their daily lives (e.g., rate changes on mortgages when they are in the process of buying a new home). To deliver contextual experiences and value-curated interactions, financial institutions need the ability to proactively understand and anticipate people’s needs needs and preferences.

- Credible – Banking providers must be trusted by enhancing brand perception through effective “moments of truth”, social conversations and feedback loops (e.g., crowd-sourced ratings, opinions, and reviews. Employees’ actions must reflect the brand’s values.

- Consistent – Delivering the same branded experience anytime, anywhere across all channels and devices — from the chairs in a branch to the buttons on an app.

- Generous – Accenture says financial institutions are obliged to offer “a wide range of strategic gestures” intended to rebuild trust in the shadow of the industry’s past scandals and questionable conduct.

Targeting a North Star

Accenture says every bank and credit union needs its own “North Star” — a compass heading for your brand’s values. It should guide you, and help you focus on tackling those items on your to-do list that will deliver the biggest returns. The North Star concept may seem similar to other oft-used — and sometimes misaligned —brand management terms: unique selling proposition, vision statement, or mission statement.

But Piercarlo Gera, Senior Managing Director in Accenture’s financial services practice says that North Star is none of these. It’s a “brand promise” that differentiates you from your competitors, defining how you will achieve your mission/vision while also describing the style and flavor with which you will execute your strategic plan.

“The ‘North Star’ concept is important both in terms of banks defining their North Star —what is it the makes them hyper-relevant to their customers — but also the reverse: how can they become consumer’s point of reference in their moments of need and of decision making, today and tomorrow,” explains Gera.

He suggests that banks and credit unions use the following questions to evaluate their positioning and find their financial institution’s North Star:

- Are you the first point of call when consumers have a question about their future, their money, and protecting their families and their assets?

- Are you interacting across the entire ecosystem — GAFAs, fintechs and providers from other industries such as retail, telecommunications and even government — to become hyper-relevant to consumers in terms of presence and accessibility?

- Do your digital and physical channels interact seamlessly with your consumers, providing them with the right level of interaction, trust-building, support and ability to talk to someone in a timely manner?

- Are employees — and any AI-powered chatbots — engaging with consumers and providing help and advice that is consistent with your brand values

Build Intelligent Platforms

The passage of the EU’s Payment Services Directive (PSD2) states that financial institutions must give outside firms access to consumer financial data via open APIs if/when requested. Even though open banking is not a regulatory mandate in North America (yet), banking executives in the U.S. are getting on board with the concept.

Forward-thinking banks and credit unions understand how important open banking will be to the future of the industry. Indeed, research by Accenture found that 63% of financial institutions believe that implementing open banking will be critical for competing, cooperating and/or partnering with fintech and bigtech players. Two-thirds say it will help create new revenue streams and 90% expect it to drive incremental revenue growth.

What does open banking have to do with a strategy of hyper-relevance? With an open banking platform, financial institutions can rewire their business toward new platforms and data primacy by deploying APIs. Collaborating with partners on the development of APIs can help yield greater contextual experiences based on multiple, integrated data streams. Accenture says that giving outsiders access to APIs will “cultivate fertile ground for more innovative services.”

Accenture also strongly recommends adding robotics, robo-advisory services, and artificial intelligence capabilities across the back-, middle-, and front offices. Financial institutions need to connect legacy platforms with more contemporary and sophisticated automation systems that incorporate algorithms fueled by data. Accenture says voice recognition interfaces like Amazon’s Alexa or Apple’s Siri that draw on cognitive computing and machine learning are a great example of how financial institutions can leverage technology to create hyper-relevant, personalized experiences.

Design for the Physical+Digital World

Nine out of ten consumers say they will continue to visit branches, and they expect to interact with a human when they’re there. But many also want automation such as advanced ATMs (59%) and access to online banking (55%).

“As consumers continue to carry out their daily banking services via convenient digital channels, the branch role will evolve but will most definitely not become extinct,” says Accenture’s Gera. “Instead, the branch will take on an ever more important role in providing human interaction while becoming smaller, more agile, engaging and flexible.”

Gera explains Accenture’s vision for branches — a strategy that fulfills multiple different roles:

- Brand Trust Centers – where consumers and staff can emotionally, logically and literally experience the values of the brand.

- Advice Hubs – face-to-face validation of online research.

- Places to Engage – Environments that afford rich opportunities for community interactions that are relevant and rewarding.

- Spaces to Educate – Where banks and credit unions can demonstrate social responsibility with financial education.

While some banks and credit unions are ambitiously adding digital to their existing branches, others, like Virgin Money, are taking what Accenture calls the “phygital” approach — a mix of both physical and digital — in entirely new directions. For instance, Virgin Money Lounges scattered throughout the U.K. live up to their name; they are actual lounges, with spaces where people can relax and unwind with complimentary refreshments, free Wi-Fi, newspapers, magazines, TVs and iPads. Several lounges include amenities such as bowling alleys and theaters and most have a play area for the kids.

To expand hyper-relevance, lounges host special events, like an after party for the London half-marathon, a Spanish-themed evening of music and comedy and a “Cops and Coffee” fraud awareness seminar. The lounges work. There’s been a 200% growth in sales in Virgin Money branches near a lounge.

Read More: This Virgin Money Lounge Is The Funnest Bank Branch You’ve Ever Seen