When it comes to transactional features like checking balances and transferring funds, most banks and credit unions do a decent (if uninspiring) job with their mobile banking app. But these days mobile banking has essentially become a commodity — table stakes that won’t set you apart from your competitors. How should banking providers raise the bar?

Just adding features to your mobile app can make users happier. According to a study from Citi, 80% consumers with feature-rich mobile banking apps (defined as having five or more features) say they are more likely to remain loyal to their financial institution vs. 70% of consumers with apps with fewer than five features.

But which features will give you the most bang for your buck? When financial institutions evaluate their current mobile banking app to figure out what’s next, they typically approach the process the wrong way, focusing on features that are most likely to make the bank or credit union money.

There’s absolutely nothing wrong with adding features that drive profits. But if one of your major strategic goals is to increase adoption- and engagement rates for your institution’s mobile app, you’ll need to offer features that consumers actually want. Focus on the challenges consumers face, not the challenges you face.

Rory Holland, Founder and CEO of CSTMR, says financial institutions need to roll up their sleeves and do their homework.

“Banking providers must understand people’s needs by segmenting their audience and getting feedback about the features they would like to see,” says Holland. “You also need to look at the market, kick the tires on competitors’ apps and read reviews.”

This isn’t what most banks and credit unions typically do. Many retail institutions are satisfied rolling out whatever mobile banking app their core provider gives them. Some may opt for a third-party solution, but they usually accept a basic level of functionality. That may have cut it a couple years ago, but it isn’t going to get the job done anymore. These days, financial institutions need to obsess over their mobile banking experience.

“Banks and credit unions often think about their mobile app purely through the lens of which features they have or may need,” says Antonio Sanchez, Senior Product Marketing Manager at Kony. “This is a mistake. A bullet list of features may get people to download a mobile banking app, but the user experience is critical. UX is what ultimately determines whether or not the mobile app is actually used.”

Read More:

- 19 Awesome Mobile Banking Apps From Banks and Credit Unions

- User Experience Crucial to Mobile Banking Usage

- 25 Digital-Only Banks to Watch

Consumers want to get a grip on their financial lives — i.e., savings and budgeting. This is doubly true for Millennials and Gen Z. For instance, everyone is looking for ways to reduce their anxiety about being able to cover emergency expenses. Along these lines, you could add features and functions to your mobile banking app that help consumers manage their money more effectively:

- At-a-Glance Payments. Let consumers see their upcoming payments and transfers and give them their safe-to-spend balance. USAA does this well.

- Account Alerts. Notify consumers with text alerts in advance of a low account balance or if they are approaching credit limits.

- PFM. Include budgeting tools, financial education, tips and suggestions.

- Automatic Savings. Set up automatic transfers to a savings account.

- Virtual Agent. Ally Bank has a virtual agent, Ally Assist, embedded in the mobile banking app that uses a conversational interface to answer consumer questions about their financial health.

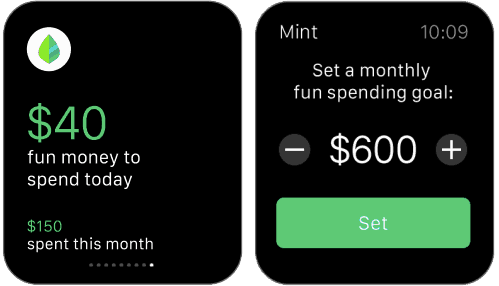

Take a page from Mint, the ubiquitous online budgeting tool. In addition to letting consumers handle transactions such as a paying bills, Mint gives consumers greater insight into their spending habits (see snapshot below). A user can set budgets across spending categories and the app alerts will alert them when the predefined limit is reaches. This level of control and proactive management is something consumers really like about Mint.

Catching Up: Financial Institutions Have a Way to Go

Forrester and Kony looked at the mobile banking apps of over 50 banking providers from around the world and came to the conclusion that most are doing a pretty poor job. On a 100-point scale, the average overall score was 63. The average functionality score was only slightly better at 65.

Perhaps most disappointing was the usability score. For this metric, Forrester and Kony used a scale of -30 to +30. The average score? A pathetic +4. The conclusion: financial institutions may be including features in their mobile apps… but that doesn’t mean the UX is any good.

In their analysis, Forrester and Kony identified some financial institutions that are doing an overall decent job with their mobile banking apps. In their final report, BBVA rose to the top with a respectable 87 out of 100 — in an academic context, that would work out to a B+ grade. There were a few others that Forrester and Kony called out as delivering outstanding mobile banking apps: Poland’s mBank, USAA, CaixaBank and CIBC. The only other U.S. bank to crack the top ten was Bank of America, coming in at number eight.

What’s going wrong? Forrester and Kony outlined five of the biggest mistakes that financial institutions are making with their mobile apps:

- Making it unnecessarily difficult to complete basic tasks.

- Not helping customers find and apply for products.

- Not helping consumers avoid or recover from errors.

- Lack of integrated digital money management to drive consumer engagement and help consumers make better financial decisions.

- Limited customer service features.

Killer App Must Haves

So what’s it going to take? How can banks and credit unions deliver the mobile banking experience that will differentiate their financial brand from the rest of the pack while also meeting the high expectations of today’s digitally-savvy consumers? Forrester and Kony list the following as “must haves” for the killer mobile app:

- Be able to enroll in mobile banking from… wait for it… a mobile phone. Don’t make consumers sign up for online banking first. Some consumers — particularly younger ones — are mobile-first, if not mobile-only.

- Tutorials, videos or demos of how the mobile banking app works, especially for features that are more advanced or used less frequently.

- Access to account balances without having to log in.

- Let users turn on “travel mode” for credit card purchases, and notify the bank if their card is lost or stolen.

- Convenient login options such as biometric fingerprint authentication, a gesture-based PIN or voice ID.

- Reach a human easily through mobile chat and telephone.

- See relevant product offers based on current products, location, recent life events and past behaviors. Say a consumer has a low account balance and no savings. Offer a preapproved cash loan.

- Make sure your mobile app supports researching products — not all consumers do their research on their computer.

- Make it easy to apply for a new product. Pre-fill applications, include progress meters and let consumers save their application and complete it on another touchpoint.

- Make it easy to set up fraud alerts. In a survey conducted by UserTesting, setting up fraud alerts was the most difficult task for consumers to do on their mobile device.

In addition to the mobile app must-haves from Forrester and Kony, The Financial Brand asked three experts to weigh in on the features they believe need to be included in a killer banking app.

Top picks from Rory Holland, Founder and CEO of CSTMR:

- Ability to add your credit or debit card to the phone’s eWallet

- Ability to hold the mobile app up to an ATM to sign-in

- Touch ID sign-in

- Face recognition sign-in

- Sync with Apple Watch or other digital devices

- P2P payments (limits, Zelle)

Top picks from Antonio Sanchez, Senior Product Marketing Manager at Kony:

- Chatbots

- P2P payments

- Personalization and contextual offers based on behavior and/or profile

- Virtual accounts

- Wallet functionality

- Gamification for goals such as savings

Alex Kreger Founder, CEO and UX Strategist with UX Design Agency, bases his selections on the type of consumer. For ordinary consumers, Kreger’s top picks:

- Biometric authentication

- Convenient balance and transaction history status with smart search

- Instant P2P payments synchronized with contacts book

- Completely digital onboarding

For those consumers who are more sophisticated and tech-savvy, Kreger’s top picks include innovations that reinvent the banking experience:

- AI managed voice assistant integration

- Predictive analytics-based forecast notifications and advices

- Robo-advising investments management

- API connections

- Third-party financial services aggregation

- International cross-currency instant transfers

- Multicurrency wallet with crypto-currencies support

- Personalized bank offers

- A system of goal-setting and savings

- Social integration

The Core Dilemma

Holland of CSTMR notes that those banks and credit unions that outsource their mobile apps to their core vendor are putting themselves at a competitive disadvantage. These core vendors provide what Holland says is a “one size fits all” approach to their mobile apps. Any bank or credit union on the platform will have basically the same mobile app — and no opportunity to customize it.

Holland says that community banks and credit unions could compete with bigger banks by pushing their core providers for more customized or unique features for their mobile apps or the ability to customize their own app — beyond just branding — right on the platform. (Good luck with that. Core providers aren’t known for their responsiveness, specifically with respect to integrating new features.)

A better option, says Holland, “is to leverage third-party fintech solutions to design, support and optimize with your own app.”

Sanchez agrees that being dependent on your core vendor — and not being able to influence the feature release cycle or product roadmap — is not financial institutions’ path to a killer mobile banking app.

“If your current provider is unable to give you control of the roadmap, then seek out another alternative for your mobile banking app,” recommends Sanchez. “Look to other verticals for inspiration of what the consumer journey should look like, including Uber and Amazon. Then sketch the ideal experience you want for your customer journey and take control of the roadmap.”

No matter what route you take — working with your existing core provider or ditching them — remember that you must prepare for the new realities of an API economy.

“Application programming interfaces (APIs) allow you to more easily add new services and features on your mobile app,” says Sanchez. If you don’t prepare, he warns, you’ll continue down the road of letting core providers unilaterally dictate the entire consumer experience.

Bottom line, what’s the most important feature for a killer mobile banking app? Simplicity and an intuitive and easy-to-use interface that allows consumers to quickly access the features they require for their daily banking. That’s something every expert strongly recommends.