There once was an old saying about ‘banker’s hours,’ when referencing a standard 9-5 day with no overtime or weekend work. Not to slight dedicated banking professionals, but historically, many bankers did work in brick and mortar offices, where doors closed promptly at 4:00pm (or earlier) every weekday, with extended weekend work rare.

Sure, banker’s hours don’t matter as much in the digital age. Online tools have allowed customers to perform basic tasks like bill payments, money transfers and checking deposits from wherever they want, whenever they want. Still, customers sometimes need answers and help with services that an app can’t handle. They want to talk to someone at their bank, but can’t because of banker’s hours.

This can all change with a chatbot. Armed with advanced cognitive capabilities, a chatbot can perform many customer-facing tasks better and faster than a human can, anywhere, anytime. The technology can drastically improve customer relationships by supplementing – not replacing – the humans who can continue to work banker’s hours.

This new frontier is wide open for exploration, and banks are already poised to take advantage of chatbots to better serve and engage customers. Call it “cognitive banking” – the melding of AI, predictive analytics, natural language understanding, and machine learning technologies to transform banks’ relationships with their customers in the digital age. Cognitive banking can deliver a highly engaging customer experience that reduces friction for the customer and cost to the bank.

Banks can use chatbots to serve customers in ways that haven’t been possible until now. That’s because cognitive capabilities allow chatbots to do some things better than people. This is not to suggest a chatbot is human. It’s misleading and counterproductive to do so. Rather, banks should embrace the fact that chatbots can outperform humans in some situations, and position them as an integral part of their omnichannel strategies.

Instant Recall: Personalization at the Speed of a Chat

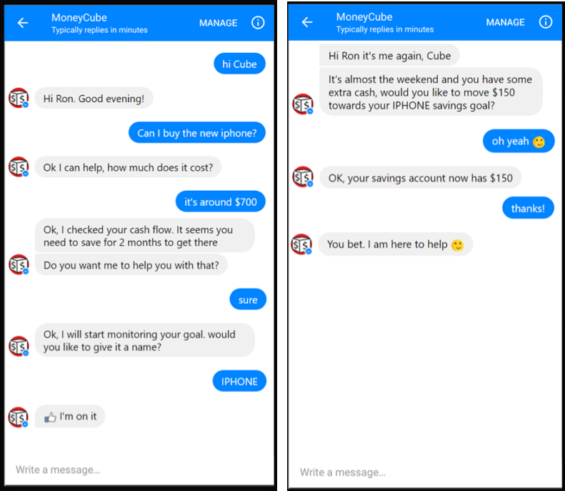

Have you ever tried calling your bank to ask a simple question such as “How much more can I save each month without overdrawing my account?” Even if a human banker was immediately available to field this query, he or she probably couldn’t provide a quick and accurate answer to such a question without first looking at personal data and taking the take time to study the information and evaluate options.

Instantly analyzing customer data, the chatbot can immediately provide a contextual answer that accounts for personal situations, suggesting a recommendation that will best fit a consumer’s needs.

Hi, It’s Your Banker Calling …

To take it a step further, when was the last time a banker did a proactive outbound call to provide real-time advice? Let’s face it, more often than not, the only time human bankers reach out to customers is to offer a generalized service that caters to many. What seems like a proactive action is actually a marketing campaign, a drive to entice many customers to try a service. Cognitive banking, on the other hand, delivers omnipresent, predictive customer service that’s personalized, timely and accurate.

The chatbot not only can use predictive analytics to answer customers’ direct queries, but it can also proactively offer advice. By consistently analyzing customer behavior, the chatbot makes sense of patterns and can proactively offer suggestions on how to manage and improve finances.

But What About Compliance?

Many banks believe an AI-powered chatbot has limitations, and these shortcomings would probably surface on issues of compliance. Despite its machine learning abilities – the theory goes – there’s probably no way a chatbot can master the nuances and particulars of compliance.

Believe it or not, a chatbot a can indeed play a role in delicate financial services. Just as it learns from historical customer behavior, the chatbot can also be programmed to respond within a set of guidelines, while still being personalized in context, and also within the boundaries guided by applicable regulations.

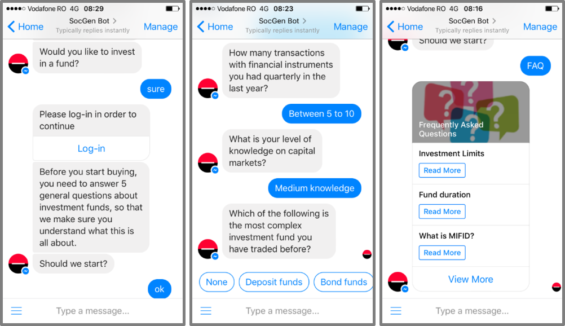

This year, BRD Groupe Société Générale intends to roll out a chatbot that will walk customers through the onboarding process and help them perform various tasks ranging from the selection of investment funds to transferring money between funds to withdrawing money from their accounts.

The chatbot has earned the trust of the bank, which believes it will guide a customer through compliance questions and disclosures more carefully than a human can. “In terms of operational risk, it’s safer for us,” said Horia Velicu, head of the innovation lab at BRD Groupe.

Autonomous Banking: The Final Frontier?

By and large, customers want to better manage their finances, but they don’t have time to stay on top of it all. That’s where the chatbot can lend a helping hand, by automatically executing money management tasks on behalf of customers, dutifully working to improve their financial well-being behind the scenes.

A chatbot can remind a customer to pay a bill on time, or, with the customer’s permission, pay the bill itself. If a customer fails to realize he/she is nearing a zero balance in their checking account, the chatbot can automatically transfer funds from savings so the customer can avoid paying an overdraft fee. It can also – again, with permission – help the customer save more by identifying “safe to save” funds and moving money out of his checking account.

There is growing recognition that it can’t be business (or banking) as usual anymore. Like every industry, banking must be ready to embrace the fact that artificial intelligence is becoming an integral part of our lives. If banks don’t adapt to these changes, someone else will.

A recent Accenture survey shows that seven out of ten consumers would welcome AI-powered advice for banking, insurance and retirement services. According to Gartner, 85% of all customer interactions won’t require human customer service reps by the end of this decade. As Chris Skinner notes in a blog post titled ‘We Must Automate Humanity’, “A machine can be programmed to get it right (the) first time, every time and never get it wrong. A human cannot.”

But the idea is not to replace humans altogether, as Skinner argues in yet another post aptly titled ‘You Can Never Automate Humanity’: “Replace humans with robots so we can all just kick back and (live) off a financial cushion will just make us all addicts living a narcissistic lifestyle in an economy that freefalls. That is why I do not believe the robots will take over everything. There will always be a need for a human somewhere.”

Because of its ability to always be available, predictive, understand compliance, and work autonomously, a chatbot can become a critical – even if not an exclusive – channel for customers interacting with their banks. At the end of the day, if a customer receives excellent customer service, he/she won’t care if it comes from a human employee or a chatbot.