The first report published by the Digital Banking Report (then known as the Online Banking Report) covering ‘online account opening’ was in 2009. At that time, online account opening was just moving into the early mass market and was a “nice to have” feature for many financial institutions.

By 2014, when our second report covering online account opening was published, digital account opening was no longer a luxury, but a differentiator when consumers were shopping for a new bank or credit union. The process had moved from being provided only as a desktop online capability to being available on mobile devices (primarily tablets) as well. The shift to mobile had begun.

In 2015, while less than 20% of the top banks in the U.S. currently offer a new account opening process optimized for a smartphone, this capability is becoming table stakes as more consumers use their mobile devices to research, shop and buy products and services. From hard-to-read screens, to requiring signature cards and proof of identity at a branch, to not supporting mobile deposits for new accounts, the new account opening process must improve.

According to the 57-page Digital Banking Report, Digital Account Opening, the benefits of using a mobile device to streamline new account opening are even beginning to reach the branch network. Mobile functionality, such as turning a smartphone into a document and ID scanner with character recognition (OCR) for improved accuracy, reduced friction and risk management, is replacing the slow, error-prone desktop processes at many banks and credit unions.

According to the 57-page Digital Banking Report, Digital Account Opening, the benefits of using a mobile device to streamline new account opening are even beginning to reach the branch network. Mobile functionality, such as turning a smartphone into a document and ID scanner with character recognition (OCR) for improved accuracy, reduced friction and risk management, is replacing the slow, error-prone desktop processes at many banks and credit unions.

Long term, the use of the mobile device as part of the self-service and branch-assisted account opening process will be even more important than opening accounts with an online desktop. According to Niti Badarinath, Senior VP of U.S. Bank, “Imaging features are the most positively reviewed features by customers. Data entry is painful. Every phone has a camera. Customers like convenience and dislike apps that don’t use features their phones have.”

Digital Account Opening Defined

Much of what is required for mobile account opening is the same as for online, but with the added complexity of varying device sizes, responsive design, the need for simplified staging and mobile identification verification. Despite these requirements, the exceptional capabilities of mobile devices provide the opportunity to significantly improve the experience for consumers and branch personnel alike.

Much of what is required for mobile account opening is the same as for online, but with the added complexity of varying device sizes, responsive design, the need for simplified staging and mobile identification verification. Despite these requirements, the exceptional capabilities of mobile devices provide the opportunity to significantly improve the experience for consumers and branch personnel alike.

Mobile device touch screens and cameras, in addition to the inherent portability of mobile devices, call for the addition of new, mobile specific features: data capture and document upload via the device camera, touch signatures, and location tracking for reporting and potentially other functions, like fraud prevention.

Core Features

Digital account opening, at the basic level would have the ability to perform the following:

- Capture and auto-fill of basic personal identity information

- Qualify applicants from a risk/fraud perspective

- Verify applicant identity (usually through third-party data sources)

- Fund digitally in real-time (usually with either a debit/credit card or with mobile deposit capture)

- Integrate with the core banking system

Ancillary Features

In addition to the five core features, a number of additional features should be included in any best-of-class digital account opening process:

- Contextual prequalification for, and cross-sell of, additional products and services using collected internal and external insight

- Online and mobile banking single sign-on (bypassing data entry and identity verification steps)

- Ability to save and resume account opening at any point in the process (supporting multichannel integration)

- Electronic signatures (replacing signature cards)

- Ability to upload photos of supporting identification documents for digital storage (business agreements, etc.)

As we look at the future of digital account opening, we will see more processes that take advantage of the mobile device capabilities both from the customer as well as branch perspective, making mobile account opening distinct from its online counterpart.

Digital Account Opening Trends

The majority of top banks and credit unions offer online account opening, yet mobile-optimized account opening capabilities are not commonplace. However, as mobile banking functionality and customer acceptance of mobile banking continues to increase, it is expected that more focus will be placed on optimizing the account opening process for mobile devices as opposed to making consumers use online tools as most do currently.

The challenge is that financial executives need to determine the priority of supporting mobile account opening in an environment where banking lags in so many areas of digital transformation. This prioritization process is underscored by the reality that there is more mobile development activity seen in the loan and credit card product lines than with the less profitable deposit products.

Moving forward, financial institutions should follow the lead of the neo-banks such as Moven, Simple, BankMobile, etc. and develop mobile account opening capabilities for foundation products (checking, savings, credit cards, etc.). These products are also more likely to be able to be supported by smartphone applications as opposed to requiring the expanded platform of a tablet device.

The key to moving more customers and (financial institutions) from branch to mobile account opening will be in providing the assurance that personal information is secure when entered and that identification can be verified quickly and easily. It is also important that basic new account opening questions can be answered without leaving the mobile account-opening platform.

Finally, while the convenience of opening a new account using a mobile device can’t be denied, the simplicity of the process needs to rule the day. Until financial institutions can eliminate/simplify legacy steps in the process, the full potential of account opening with mobile devices won’t be realized.

Digital Account Opening Forecast

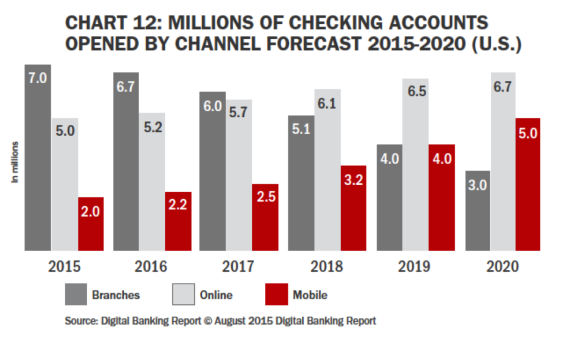

Within the report, we provide a forecast of mobile and online account openings for the next 5 years based on several industry assumptions. This estimate can vary based on industry and technological changes.

Forecasting channel use and the number of checking accounts being opened requires a number of assumptions. While we do not expect the number of checking accounts opened to increase significantly overall, this could change if the government follows the lead of the United Kingdom, where account portability allows consumers to move accounts to different institutions without changing their account number.

In addition, we expect online account opening to continue to grow, albeit at a slower growth rate over the next 5 years. Finally, improving the user experience for mobile devices – with pre-populated fields and leveraging the OCR camera functionality – will be the catalyst for strong growth. As more organizations begin to offer this capability, a significantly higher percentage of accounts will be opened with mobile devices.

In our assumptions, while using digital devices to open the account, accounts opened in the branch using tablets or mobile devices are categorized as ‘branch’ openings for this analysis.

Digital Account Opening Challenges

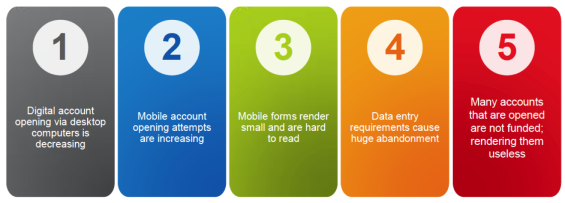

The greatest problem facing online and mobile account opening today is poor user experiences that drive abandonment. Applying for financial products entails many steps to satisfy risk requirements and comply with regulations. Here are the top challenges to for banks and credit unions trying to meet the needs of the digital consumer.

- Digital Account Opening via Desktop is Decreasing: As more consumers move to their mobile devices to perform tasks that were previously done online, there is an increasing expectation that organizations in all industries will provide an optimized mobile platform for basic tasks.

- Mobile Account Opening Attempts are Increasing: For the digital consumer, the mobile device is their link to everything digital. These consumers will research, shop and buy, on-the-go 24/7/365. If your organization doesn’t have an easy-to-find gateway to mobile account opening, they may abandon their search and move to a competing institution.

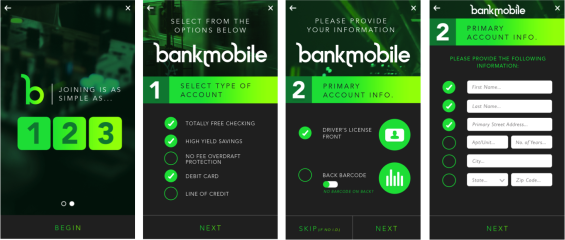

- Traditional New Account Forms Don’t Render Well on Mobile Devices: While smartphone screen sizes continue to increase, online forms used by banking organizations for new account opening are still too extensive for the digital consumer. For mobile-only firms like Moven, the new account opening process is completed in 5 steps … without extensive forms.

- Data Entry Requirements Result in Abandonment: Why should we require consumers to enter their basic information, when mobile phone OCR capabilities can capture the majority of the identity data, pre-fill the new account form, and even authenticate the new account opener? BankMobile uses a photo of the prospective customer’s drivers license to complete the majority of the application process.

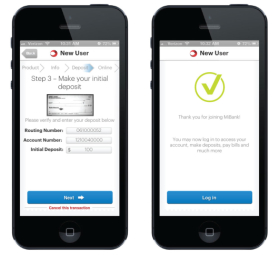

- Unfunded Accounts: While some firms allow the consumer to use a debit/credit card or mobile deposit to fund a new account, many still require an in-person deposit at the branch (when they may also be required to complete signature cards). Both steps are cumbersome and can result in dormant, zero balance accounts.

The Future of Digital Account Opening

One fact is clear … the new account opening is becoming easier. Leveraging mobile photo data capture, designing the new account opening process to be easier for a smartphone user and eliminating the need for legacy, paper-based documentation will dramatically cut down the time required to open account in the near future.

For user-initiated new account openings as well as branch-assisted account openings, digital capabilities will transform new account opening, allowing more time for discovering the needs of the new customer, determining optimal financial solutions, and building a better onboarding experience. Data capture, qualification, identity verification, account funding, and account creation will become so automated that the act of account opening might take seconds as opposed to being a hurdle to engagement and loyalty.

About The Guide to Digital Account Opening

The Guide to Digital Account Opening is an in-depth review of the transformation of the new account opening process in banking. Focused on online, mobile and branch-assisted digital account opening, this Digital Banking Report is available for purchase as a single issue or as part of an annual subscription.

The Guide to Digital Account Opening is an in-depth review of the transformation of the new account opening process in banking. Focused on online, mobile and branch-assisted digital account opening, this Digital Banking Report is available for purchase as a single issue or as part of an annual subscription.

Subscriptions to the Digital Banking Report are available to individuals and institutions, with the distribution of reports being done digitally. Subscribers not only receive monthly reports but also have free access to the 150+ report archive.

The Digital Banking Report, Guide to Digital Account Opening, focuses on the digital account opening experience, and the landscape of solutions and workflows that comprise the end-to end account opening process. The report provides trends and projections, case studies, and an extensive review of solution providers, covering both self-service and branch-assisted digital account opening processes.

This report will help banks and credit unions move forward with digital improvements to the account opening, removing friction, simplifying processes and providing a seamless digital experience. With numerous case studies, it is hoped that more organizations will follow the lead of Moven, Simple, GoBank, BankMobile and others in offering a mobile-optimized account opening option.