The last of the Millennial generation are in high school. Most have already graduated and are in the workforce as young adults. This is the largest generation in history with 85 million people (vs. Gen X with 50 million people and Baby Boomers with 75 million people). While there are some decidedly different channel usage patterns among these three generations — particularly the older half of the Baby Boom — what is clear is the Millennials are pushing brands to engage them where they are, which is everywhere… all the time.

Millennials are more digitally inclined and demanding than prior generations, but what’s also true is they pressure brands to deliver more integrated online/offline customer experiences. And now Gen X’ers and Boomers want it too. To varying degrees, most consumers now expect a coherent customer experience — from the initial touchpoint, trial, sale, usage and ongoing brand interactions. Delivering a seamless experience is no longer a “nice to have,” it’s a “must do.”

This behavioral shift creates a challenging new reality. Brands that are not able to execute a choreographed online+offline experience are at a vast competitive disadvantage from those that can. Why? The answer is simple. If your brand cannot engage consumers when and where they want, you don’t even have a chance. You will be like the angler obsessing about the pole, line, bait and hook while fishing in a spot where there aren’t any fish.

Look at the traditional Four P’s of Marketing (Product, Price, Promotion, Place). Many marketers are still very focused on the first three P’s while only paying only lip service to “Place.” While Product, Price and Promotion are very important, but only if you are fishing where the fish are. And that’s only part of the equation. Once a new customer is sold and onboarded, they also expect the product/service will be supported across multiple channels. Consumers are now demanding to be engaged, sold and serviced where they prefer to be, not in the channel(s) that’s most convenient or cost-effective for you.

In retail banking, there are wildly disparate levels of competency in managing a multi-channel marketing, sales and service experience. If you think your financial institution is a leader, seek to maximize this (brief) competitive advantage, but prepare yourselves for the day where this is no longer a differentiator but table stakes. If your bank is behind, it has never been more important to “up your game” just to stay relevant.

While the leaders in the financial industry may enjoy an edge, they are by no means experts who have mastered the omni-channel model. The leaders in specialty retail are immeasurably better at managing a multi-channel experience than even the most competent financial institutions. Forces like these from outside the banking industry are creating tangible pressure for financial institutions to deliver an omni-channel experience. Amazon’s legendary ability to auto-suggest relevant products has elevated consumers’ expectations, and now they wonder why retail banks and credit unions can’t (or won’t) engage them in the same way.

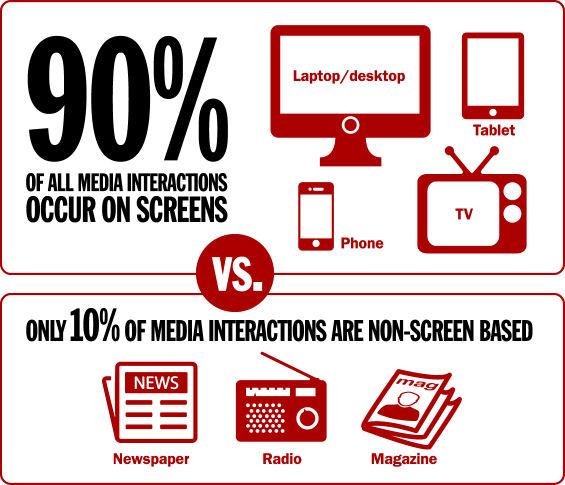

While branches and other traditional marketing and delivery channels will continue to remain important, digital has become essential. According to an Accenture Study consumers view online banking as the area they would like most to see banks invest in and develop. Eighty-percent of them use this channel at least once a month. Mobile banking activity has increased nearly 50% since 2012, with approximately one-third of customers active at least once a month. The most active online and mobile banking customers use these channels at least weekly. This will only continue to increase as Baby Boomers and Gen X’ers follow the digital/mobile channel behavior being blazed by Gen Y. Is Apple Pay just another mobile application albeit from a very adept marketing company or is it evidence that the fourth “P” of marketing (Place) is now more important than ever to earn business and loyalty from an increasingly digital/mobile consumer? All I know is the most successful fishermen are always the ones that fish where the fish are.

Why should financial institutions focus on acquiring and retaining mobile banking users? Because, they are:

- Younger – 55% of mobile banking users are between 18 and 34, vs. 25% for non-users

- More affluent – Average income for mobile banking users is $71,000, vs. $59,000 for non-users

- Buy more financial services products – Mobile banking users hold 3.1 products with their bank vs. 2.8 for non-users

Catching Up? Where to Begin

If your organization is in catch-up mode it can be challenging to figure out where to begin. While there are a host of important issues such as technology infrastructure, media attribution and the optimization and management of customer offers – you need to focus first on managing your information/data. That is because it is foundational to achieve multi-channel marketing and product/service delivery. Without having your data in order it’s impossible to deliver the experience the customer now demands.

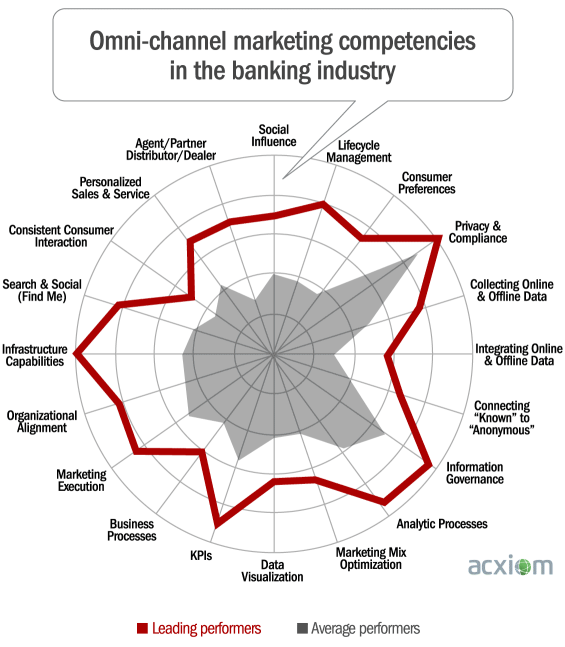

This chart illustrates the disparity between the average performers and leaders in the banking industry with respect to omni-channel capabilities. Is your bank a leader… or just average? Areas where there is the greatest opportunity for improvement include:

- Collecting Data (Known and Anonymous) – Does your organization presently collect data to effectively support marketing and analytics, using all available data sources?

- Integrating Data (Online/Offline) – What is your organization’s ability to integrate all available data, whether offline or online, across the company?

- Customer Recognition (Known to Anonymous) – There are collections of data, some of which are entity-based (e.g., mobile devices, iPads, PCs) some are people-based. Have you done the best you can within legal boundaries to connect all that at the individual or segment or pseudo-anonymous (aka cookie) level? Can you recognize the customer no matter where they are or what device they are on?

- Information Governance – How well does your organization mitigate the risk that exists from lack of controls regarding information storage and usage? Can you manage all these data sources in a compliant fashion?

More than ever, customers now expect you to find them and serve them in their channels of choice. Hoping they will somehow conform their behavior to a haphazard array of one-off marketing and service channels will make is increasingly difficult to achieve success in this new era. Because data is the fuel that makes all 1:1 marketing possible, the first step in the multi-channel journey is to ensure you are able to collect, store and analyze data in a compliant manner so you can begin to meet your customers where they are.