Consumers are becoming — nearly literally — kids in a financial candy store, able to choose among both traditional and new types of providers and to amalgamate what they choose into banking their way. Increasingly this makes the retail banking consumer the manager of their own financial dealings and destiny, balancing their “portfolio” of providers who render services both broad and narrow.

Incumbents still enjoy an edge. However, this situation holds threats for traditional financial institutions, and they must look beyond the current state of affairs that could make them feel like they are still holding their own against fintechs, neobanks, digital-only providers and other rivals.

The situation could change quickly.

These conclusions are drawn from a study by Galileo, the banking-as-a-service subsidiary of SoFi. They have implications for product design, competitive strategy, and marketing, especially regarding affinity group promotion and the expanding expectation by financial consumers of rewards for just about every relationship they have with providers.

“There are a lot more choices available than in the past,” says Seth McGuire, Chief Revenue Officer at Galileo. “Consumers are making active choices and they are experimenting.” McGuire spoke during a webinar covering the research as well as in an interview with The Financial Brand.

The variety of options has caused consumers to change their attitudes toward their finances. “People want to access their money how they want, where they want, and actively from any provider,” says Sherri Haymond, EVP, Digital Partnerships at Mastercard, who also spoke at the webinar. “They want to choose the method that works for them, they want it to work when they need it, and they want their money to be simple to access.”

As open banking becomes increasingly part of the mix, consumers will be able to do business with their choice of providers and move their funds around quickly.

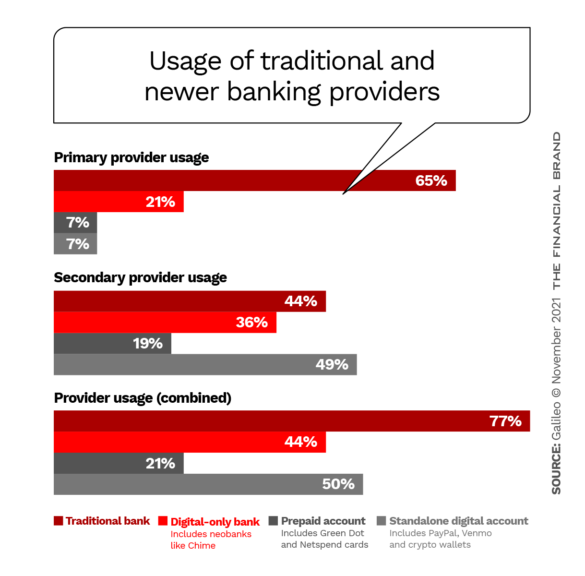

The Galileo survey examined relationships with both primary and secondary providers, though the line between the two categories has been blurring. It found that being a primary provider and holding the winner’s share of a consumer’s financial assets don’t necessarily go together anymore.

While 77% of consumers surveyed consider a traditional financial institution to be their primary or secondary provider, on average people keep only 57% of their funds with those institutions. By contrast, they keep an average of 43% of their funds in accounts with nontraditional providers. The three categories of nontraditional providers and their shares of funds: digital-only banks (22% of funds), which includes companies like Chime; standalone digital accounts, like PayPal and Venmo (13%); and prepaid accounts like Green Dot and Netspend (8%).

And the news about who holds consumers’ funds is not all: Many people are using nontraditional providers as secondary providers — 49% using standalone digital accounts, 36% using digital-only banks, and 19% using prepaid accounts.

Read More: The Most Popular Digital-Only Banks in the World

Strategy Hidden in Plain Sight:

The risk traditional institutions face is that the challengers typically start with a very narrow offering. As they build up a following, expanding their product lineup becomes more attractive and consumers can be tempted to make these providers their primaries.

While many challengers have started with some variation on transaction accounts, consumers increasingly treat these accounts as “money silos,” according to Galileo’s McGuire. These quasi-savings accounts offer the perception of being a stash of cash that won’t be touched for those who may have trouble putting money by in traditional accounts.

Read More: The World’s Biggest Database of Digital Banks

Use of Traditional and Nontraditional Offerings Isn’t Very Different

“As people explore how to use different offerings, they are finding their own ‘mix and match’,” says McGuire. There are many services traditional institutions offer that the newcomers don’t — consider needing a cashier’s check to purchase a car, for example. But McGuire sees the new providers as canny and inventive and such disadvantages can be overcome in time. Digital alternatives could very well develop and tip the scales.

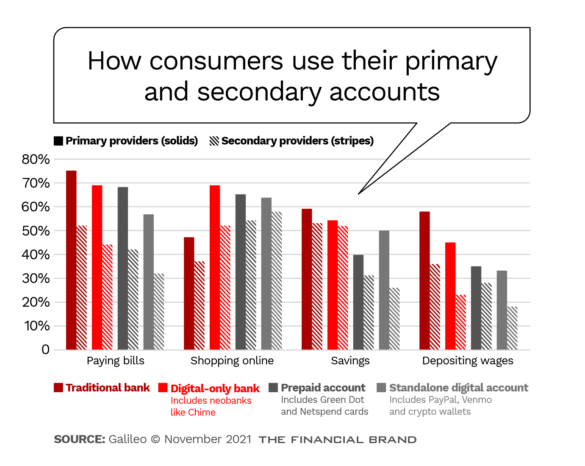

Already, according to the study, people are using their traditional and nontraditional providers for similar activities.

An interesting finding is how many consumers deposit their wages into nontraditional accounts — even when those accounts are not considered their primary providers. And digital-only banks are used for online shopping more than traditional bank accounts, when both are primary providers for a given consumer.

“People are becoming more comfortable using these [nontraditional accounts] for more activities,” says Mastercard’s Haymond.

Challengers Pull Ahead in Satisfaction:

Something that should worry bank and credit union executives is that satisfaction levels come in higher for nontraditional providers who are seen as primary providers.

Galileo reported that of the 65% of their sample who consider traditional institutions to be their primary provider, only 66% say they are satisfied. By contrast, of the 21% of people whose primary provider is a digital-only bank, 79% say they are satisfied. Of the 7% who say a standalone digital account is their primary relationship, 81% say they are satisfied. (Prepaid accounts, representing 7% of the primary providers, came in just behind traditional providers for satisfaction, at 62%.)

Another worrisome finding for traditional players: 62% of all consumers say they are somewhat or highly likely to switch to a digital-only bank. And for three key generational categories, the percentage is higher: Gen Z (72%), Millennials (77%) and Gen X (55%).

More broadly, 31% of consumers surveyed say they feel motivated to switch primary providers of any kind, typically over fee levels, reward and points, security issues and convenience.

Digital Adoption Spans Generations, Accentuates Competition

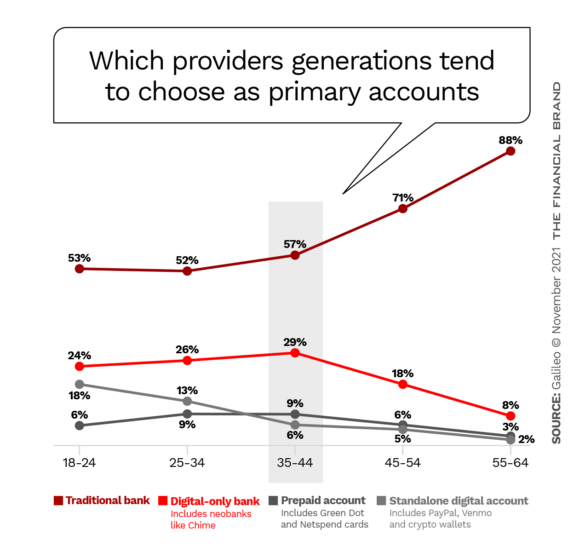

McGuire says that the survey shows that all generations have been drawn towards digital services, which makes the nontraditional provider categories greater competition than formerly.

However, a key finding is that 21% of the overall sample uses a digital-only bank as their primary provider. Of those consumers, the greatest share are those between 35-44, which includes both Millennials and Gen X.

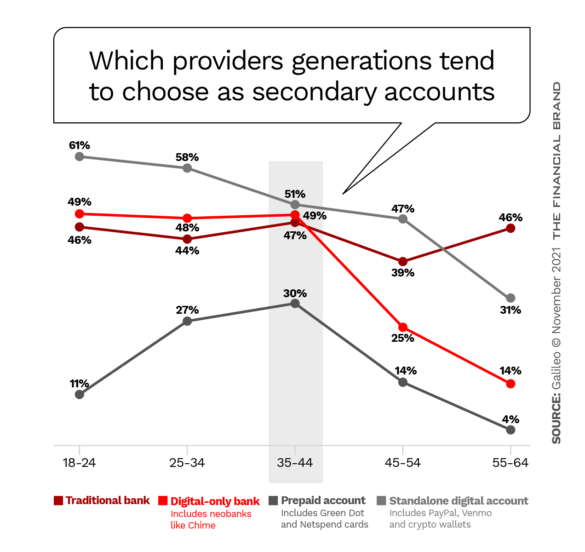

Interestingly, when it comes to secondary providers, the youngest consumers (18-24) and the oldest (55-64) are equal in their uses of traditional institutions as secondary providers. On the other hand, the youngest generation is by far the heaviest when it comes to use of standalone digital accounts like PayPal and Venmo.

Read More about Open Banking: Why Open Banking Is a Must-Have for U.S. Financial Institutions

Marketing Issues to Arise as Secondary Providers Buck for Primary Status

As the nontraditional players gain further ground, bank and credit union marketers will likely need to counter some of their offerings with new efforts at product design.

Two areas traditional institutions can focus on are rewards and affinity marketing.

One of the leading reasons that consumers say they would be interested in tapping non-financial firms for embedded banking services would be rewards or discounts (65%).

McGuire says consumers increasingly wonder why traditional institutions typically only offer rewards for using credit cards, for example, and not for using debit cards. In fact, increasingly consumers seem to want rewards for all aspects of their financial relationships.

“I think the expectation has shifted during the past few years,” McGuire explains. “They want to be rewarded for their loyalty and for their actions. The more of that which occurs, the more likely they are to obtain more products or use more services from a given company.”

A risk for traditional players is that they can be slow to develop the technology that will create competitive rewards programs, McGuire suggests. “Fintechs are uniquely positioned, because of their technical stack, to move faster and build the necessary linkages,” he explains.

Affinity marketing represents another potential plus, if an institution can build a genuine program that people with a common interest can rally around. This may take the form of a banking-as-a-service partnership with a group representing that interest.

McGuire explains that affinity marketing today goes far beyond cards with team or cause logos. He says that Aspiration, the environmentally friendly neobank, is a good example, as is Greenwood, which is organized to serve Black and Latino consumers. Another example is Purple, which serves the disabled.

Both of these factors represent means of differentiating a provider from others.

“The research shows that you can check the box on convenience, you can check the box on lower fees, on easy access to cash, etc.” says McGuire. “After that, you must get into differentiation to enable customer acquisition.”