For the last decade, new competitors have been unbundling financial services and delivering products that are highly personalized and delivered with speed and simplicity. In response, consumers have diversified the financial institutions they work with, building their own open banking style of portfolio of savings, borrowing, payments and investment apps to better serve their needs.

Now that many of the first fintech firms such as PayPal, Square and others are achieving scale, they are offering expanded financial services as many seek to provide ‘super app’ functionality for stronger customer engagement and loyalty. The question becomes what will consumers do next? How do they want to manage their finances, their privacy and their daily lives? Most importantly, what will the value transfer between financial firms and the consumer be in the future?

To answer these and many other questions facing financial institutions, the Digital Banking Report asked people in the industry to provide their projections as to what will happen in the future … and when? Our global research study included not only banks and credit unions, but other financial services providers including fintech firms, third-party solution providers, as well as advisors and consultants to the banking industry.

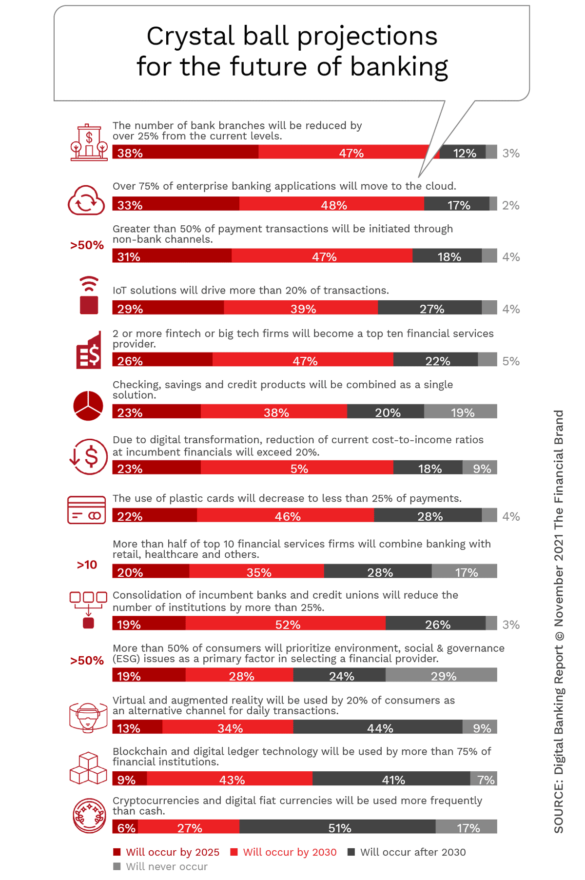

The research focused on 14 perspectives — shown in the first chart, below — within four areas of banking:

- Competition and Consolidation

- Modern Technologies

- Payments

- Digital Transformation

While the insights collected were enlightening, they obviously need to be taken within the context that no specific component of financial services can be viewed with certainty. The pandemic taught us that for sure. That said, the projected speed of adoption of some projections (e.g. use of cloud computing and industry consolidation) can’t be ignored. Likewise, the slowness of other projections (e.g. impact of social responsibility and use of crypto) should not be assumed.

Banking is Transforming at Different Speeds

One of the biggest takeaways from our research is that not all changes that are regarded as ‘inevitable’ in the banking industry are expected to happen at the same time … if at all.

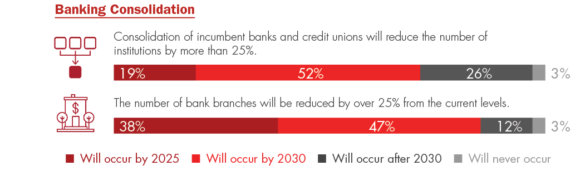

As can be seen in the chart below, the greatest consensus among retail bankers was around the likelihood of significant branch consolidation. The research showed that almost four in ten executives who responded to the survey thought there would be a 25% consolidation by 2025 (just four years from now).

Another 47% believed this level of consolidation would happen by 2030. Compared to all of the other projections, this had the lowest number of respondents thinking it would happen after 2030 or not at all.

Crystal Ball Highlights:

Speed of change will be rapid in branch consolidation and cloud computing, much slower in crypto as a payment and blockchain.

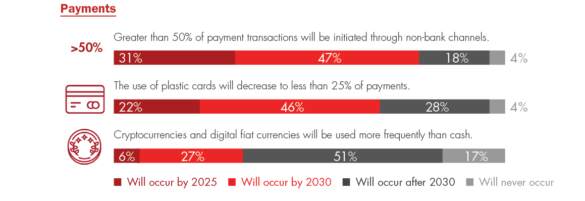

On the other end of the spectrum, the least number of respondents saw cryptocurrencies being used more than cash in the near or mid-term, with the highest number of respondents seeing cryptocurrencies surpassing cash use after 2030.

In between, a ‘barbell’ response range was seen when we asked financial industry executives whether consumers would select their financial institution based on social and environmental issues. While 47% saw this happening before 2030, a similar percentage (53%) saw this consumer trend happening beyond 2030 or not at all. In fact, the ‘not at all’ perspective was the highest of all projections.

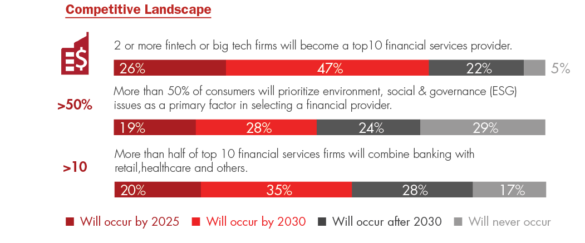

Competition Drives Consolidation

While the economy is recovering from the impact of the pandemic and the vast majority of traditional financial institutions are enjoying strong earnings, competition in banking has never been more intense. In fact, JPMorgan Chase’s CEO Jamie Dimon said in his annual shareholder’s letter that traditional banks are playing an increasingly smaller role in the financial system as big tech and fintech firms continue to grow.

“It is completely clear that, increasingly, many banking products, such as payments and certain forms of deposits, among others, are moving out of the banking system. In addition, lending in many forms – including mortgage, student, leveraged, consumer and non-credit card consumer – is moving out of the banking system,” he wrote. This perspective is reflected in the responses provided in our research.

While not believed to be the most imminent scenario by 2025, almost three-quarters of executives surveyed thought that at least two fintech or big tech firms will be a top ten of financial institution provider (in terms of assets) by 2030. Only 5% of organizations didn’t expect this ever to occur. More than half the institutions surveyed also expected more than half of the top ten financial services firms to use open banking functionality to combine banking with non-banking services by 2030.

Ready or Not:

Nearly three quarters of financial executives expect a fintech or big tech firm to be a top ten financial institution in less than a decade.

As established financial institutions increasingly need to move at digital speed to deliver startup-like innovations, and as fintech firms search for scale of business, there will increasingly be partnerships and collaborations between these types of entities as well as the increasing use of third-party providers to deliver solutions in weeks and months as opposed to the legacy method of ‘annual innovation deployment’.

While there is a great deal of discussion in the industry around the commitment of the banking industry to environmental, social and governance (ESG) issues, there is a lack of consensus as to whether consumers will actually select a banking partner based on these issues, as noted above. Because of the interesting split of opinion in this area, it will be interesting to watch whether consumers actually take action based on their stated belief around social and environmental issues.

The changing competitive landscape is reflected in the responses to trends around banking consolidation. While many of the competitive and consolidation trends began more than a decade ago, the landscape has changed at an even more rapid and dramatic pace since the onset of the pandemic. The benefits of innovation, new product development, the economic benefit of digital distribution and engagement, and the use of data and analytics can’t be over emphasized.

These forces are resulting in 71% of financial executives projecting a 25% consolidation of banks by 2030, and 85% of executives projecting a similar consolidation in the same period. In fact, almost four in ten executives expect 25% of branches to be gone in four years.

Banking’s New Metrics:

The survival of many financial institutions will not be defined by how they cut costs, but how they innovate and serve the customer with a ‘challenger mindset’.

Despite the benefits of large, existing customer bases, economies of scale, strong balance sheets and trusted legacy brands, traditional banks and credit unions can’t assume a successful future is guaranteed. Instead, all traditional financial institutions must embrace a ‘competitive mindset’ that can help to future-proof organizations from the nimble new players that are focusing on combining data and digital delivery to meet customer needs.

No longer is cutting costs enough for success in an environment controlled by consumers and small businesses who want you to know them, understand them and provide a strong value transfer for their loyalty.

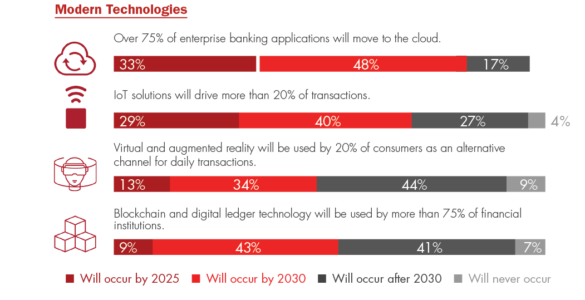

Deployment of Modern Technologies

When looking at technology trends for 2022, Gartner VP Analyst David Groombridge states, “CEOs know they must accelerate the adoption of digital business and are seeking more direct digital routes to connect with their customers. But with an eye on future economic risks, they also want to be efficient and protect margins and cash flow.”

Virtually every financial institution knows the need to use data, AI and other applied analytics to drive results, but we consciously decided to avoid any projections around timing of deployment since our recent research indicates a very long-term path to maturity. As a result, we focused on the deployment of cloud solutions, IoT solutions, virtual and augmented reality and blockchain technology.

Banks Not Prioritizing Technology:

With the exception of cloud computing, the timeframes expected for the deployment of many modern technologies is slower than expected.

While we weren’t surprised by the projections that cloud computing will become commonplace by 2030 (or sooner), we were surprised by the conservative timings for the use of blockchain, where only 9% of organizations surveyed believed blockchain technology would be used by 75% of organizations by 2025, an additional 43% by 2030 and 41% had a projection of a longer-term deployment.

Continuation of Turbulence in Payments

In no sector has the impact of competition, economic downturn, regulation, digital transformation and consumer behavior been greater than in payments. The payments sector experienced its first revenue contraction in more than a decade as consumers went into seclusion and businesses closed.

But, similar to many of the changes projected in our research, the pandemic reinforced shifts that were already in play. For instance, the importance of speed of payments, decline in the use of cash, and the accelerated migration from in-store to online commerce all created new opportunities as well as challenges for all players in the financial space.

Payments Exodus:

By 2030 more than half of all payment transactions will be initiated by nonbank players, predict 78% of industry executives.

Even as we approach the third anniversary of the onset of the pandemic, it is unclear which payment trends will revert to what was seen before the pandemic, and which will be permanent. Nonetheless, it is clear that the trend towards faster payments and less cash will continue. The integration of payments solutions within retail platforms for embedded commerce also does not seem to be temporary.

According to McKinsey, “The process of reexamining long-standing payments value propositions is already under way. While old tenets still hold true – scale still matters and ‘owning’ the customer relationship remains important, for instance – sticking to them is no longer sufficient to ensure success.

Future of Digital Banking Transformation

Research done by the Digital Banking Report has found that traditional financial institutions now rank themselves lower on the digital transformation maturity scale than they did in 2019. The reason for this retreat, despite massive commitments to digital banking transformation, is the speed of change in consumer expectations, industry competition and innovation.

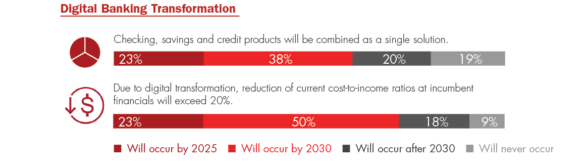

When we asked financial executives about the possibility of a move from a product-centric business model to a customer-centric model where checking, savings and lending are combined as an integrated solution, only 23% of those surveyed saw this happening by 2025, with a modest 38% saying it would happen by 2030.

Not surprisingly, more of those surveyed saw increased economies from digital transformation in the near-term, with nearly three-quarters of executives believing a cost-to-income improvement of more than 20% will be achieved by 2030.

If we had asked about the future of banking before the pandemic, many of the projections would have underestimated where we would be today. It is possible some of the projections made in this research may prove to be overly aggressive. The opposite is also true. In any case, as stated by Forrester’s Jacob Morgan, “Future banking will be invisible, connected, insights-driven, and purposeful.” We agree.