It’s easy to dismiss the claims of some of the fintech entrepreneurs as bluster fueled by bucketloads of venture capital. But some of them pull it off, and not just recently.

Charles Schwab & Co., after all, was a disruptor, pioneering the discount brokerage business in 1974 and taking on the traditional brokerage giants of the day. It didn’t topple the giants, but it shook up the business, changing business models and impacting fees.

For Brian Barnes, Schwab is the role model for his M1 Finance. Even though M1 began life as in investment app, and has been successful there, in the shadow of Robinhood, its target isn’t solely overpriced investing services, but the total financial needs of mass affluent customers of the large banks. Barnes maintains these customers are not well served.

Barnes, Founder and CEO of M1 Finance, says the company’s core belief is that consumers should be able to “treat all their money as one giant pool.” More significant for banking providers, Barnes firmly believes that a personal finance account — with elements of investing, saving, borrowing and spending — will be the primary bank account of the future.

New Banking Order:

A low-cost digital account integrating retail banking and investing may ultimately supersede the primacy of the checking account.

With two banking partners already on board, M1 is part way to realizing this goal. But Barnes took an unusual step to advance the plan far more broadly.

Barnes has acquired — on his own — a small Minnesota community bank to enable M1 to fully develop personal finance accounts, before the megabanks can get their act together.

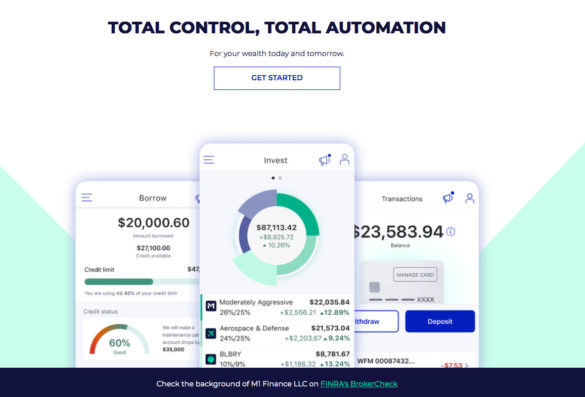

Launched in 2015 as an investing app for middle-market self-directed investors, M1 Finance now includes three primary services, all integrated:

- Investing: A free investing app with no trading commissions that offers fractional shares to help investors keep their portfolio balanced according to their preferences.

- Borrowing: M1 customers can borrow against their investment portfolio at low rates.

- Spending: Through its partnership with Lincoln Savings Bank, M1 offers an FDIC-insured digital checking account and debit card. The neobank also offers a credit card issued by Celtic Bank.

Barnes says the company has 300,000 funded accounts on the M1 platform. (The number of total accounts is higher, Barnes states, but he calls that a “vanity metric,” because it includes people who download the app, but don’t fund it.) Assets under management are “north of $5.5 billion,” he states. That figure has grown five-fold since early 2020, prompting four rounds of financing. The latest infusion valued the company at $1.45 billion, according to Fortune.

Barnes wouldn’t disclose the exact total of M1 customer deposits held at Lincoln Savings, but says “it’s in the hundreds of millions.”

M1 Finance uses a “freemium” strategy. The three core products are all free, but an M1 Plus account, which costs $125 a year, brings a lower borrowing rate (2% versus 3.5%), access to a cash-back credit card and several other benefits. Barnes says every new customer gets M1 Plus free for a year. He wouldn’t say what portion remain premium customers after that.

Read More: Can Traditional Banks Keep Pace With Fintech Challengers?

One Way to Get Into Banking: Personally Buy a Bank

Sometimes significant events come about quite unexpectedly. And that’s how Brian Barnes ended up, at age 31, as not only the Founder and CEO of a fast-growing investment app, but the new owner of a $30 million community bank in the northern Minnesota town of Buhl, population 900.

A casual dinner conversation with a colleague and her spouse, who works at a law firm that does bank M&A work, led to a follow-up visit with one of the firm’s lawyers. Within 15 minutes, says Barnes, the lawyer told him, “I have a bank for you that’s trying to sell.”

“It was a perfect opportunity that just happened in the first meeting,” Barnes relates. For M1 to buy a bank would be highly complicated, as SoFi and others have found out. But having Barnes himself buy the bank was more straightforward, once the bank’s owners agreed and regulators approved.

“The natural buyer would have been another small bank,” says Barnes, “but once the owners got comfortable with me sort of coming out of nowhere, they realized they would never have seen the money I planned to invest in technology if they had sold to another bank.”

First National Bank of Buhl has two branches and serves an area with a combined population of about 11,000 people. “They don’t have a ton of growth opportunity,” says Barnes. The fintech entrepreneur says he told them he is committed to supporting the bank’s current local markets as well as building a banking-as-a-service offering.

Read More:

- How Fintechs Buy, Rent and Fight Their Way Into Bank Charters

- Millennials and Gen Z Demand Digital Investing Tools

BaaS Plans for the Newly Acquired Bank

M1 Finance will continue to work with its two partner banks, according to Barnes, but he adds that the Buhl bank will give M1 more flexibility in releasing new banking products over time. “We didn’t love the idea that anytime we needed a new product, we would have to go out and search for a new bank partner and then manage multiple bank relationships,” Barnes allows.

The newly acquired bank could be the vehicle by which M1 offers mortgages, auto loans, home equity lines or even farm equipment loans.

Barnes figures that as long as he’s improving the technology at the Buhl bank to provide what M1 needs, he might as well make a Banking-as-a-Service business out of it. Of the approximately 15 banks offering BaaS arrangements to fintechs, he states, most are doing it as a side business. For First National of Buhl it will be a core business, since their traditional banking business is so small.

“Once you get to a certain size and scale, a fintech can’t avoid regulation — operating outside the rules becomes more problematic than operating ‘in the club’ with regulators.”

— Brian Barnes, M1 Finance

The CEO confirms that M1 Finance’s intent is to become a bank holding company and bring the Buhl bank under that umbrella. They’re not ready to begin that process yet, but he thinks that they will be ready within 12 to 18 months.

“Truthfully it’s easier to operate without the legal regulatory compliance associated with a bank, and so that’s why fintech companies have avoided it for so long,” observes Barnes. “Once you get to a certain size and scale, however, you can’t avoid that, and operating outside the rules becomes more problematic than operating ‘in the club’ with regulators.”

Watch Out Chase and Wells Fargo

In a blog, Barnes writes that banks need modernizing but are unlikely to drive the change themselves, the megabanks in particular. The reason, he says in an interview with The Financial Brand, is simply that “they make too much money in business as usual.” He also states bluntly: “Big means slow.”

“I’ve talked to a lot of people who work at the big institutions and they bang their heads against the wall because they say you can’t get anything done despite having unlimited resources. And they know that their products are not as easy, as simple, as intuitive, as low cost as a lot of what’s coming out.”

The Race Is On:

It’s an open question whether agile newcomers will become large enough to survive before the megabanks get their act together.

But Barnes also notes that the end of the story has not been written. Time will tell, he says, whether the better products such as those offered by M1 Finance attract enough users, assets and distribution to stay in business before the incumbents figure out how to innovate. “I do think it’s a story that will be written over a decade or longer,” he adds, “not one or two years.”

Meanwhile, M1 Finance is not targeting the underbanked or unbanked markets as many neobanks do. Instead the startup’s premise is that Chase, Bank of America and Wells Fargo are not serving their mass affluent customers well, so it’s going after those customers.

With better technology, a better customer experience and much lower costs, M1 can pass the savings to the consumer and do so profitably, Barnes maintains.

Charles Schwab’s success over decades proved that view to be correct. Barnes believes M1 Finance can do much the same as it pursues a digital personal financial account.