More than ever, the ability to provide transactional and engagement functionality across digital channels is a critical component to success in banking. Traditional financial institutions must do more than just enabling digital banking support. They need to provide greatly enhanced speed and simplicity of acquisition and onboarding customers in both online and mobile channels. Failure to meet consumer expectations will result in significant app abandonment rates, negatively impacting financial institutions’ customer acquisition and relationship expansion efforts.

The largest banks and alternative financial services providers, including both fintech and big tech organizations, are already delivering on consumer expectations by reducing the time and effort required to open and use checking accounts immediately. In addition, they have integrated human communication to assist with any challenges a customer may have, close to eliminating new account application abandonment rates exceed 50% at many traditional banks and credit unions, according to Cornerstone Advisors.

The impact of digital account opening is clear. Cornerstone Advisors found that during the first half of 2020, digital banks grew by 67%, with the percentage of new deposit accounts opened with digital banks growing threefold from 6% in 2017 to 18% in Q2 2020. While some of these new accounts may be secondary relationships, over 20 million households consider a digital bank to be their primary financial institution.

It is essential for traditional banks and credit unions to improve the new checking account opening and onboarding experience, reimagining the back-office processes that create unneeded friction and dissatisfied customers.

Read More:

- Digital Account Opening: Hot Trend, But Kinks Hinder Speed

- Mobile Banking Apps Failing in Key Areas of CX

Time for Mobile-First Strategy

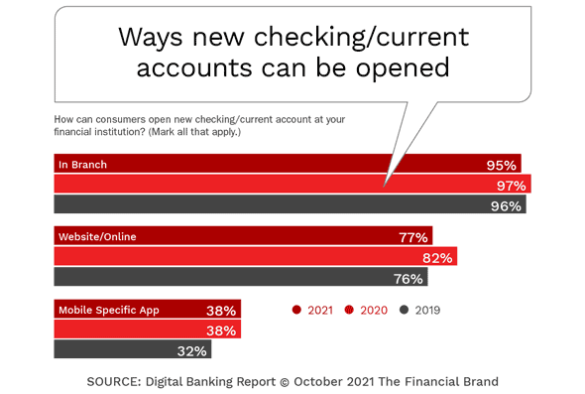

Checking account openings through digital channels exceeded branch openings in 2019, according to Cornerstone, with the percentage of accounts opened digitally accelerating significantly since the pandemic. This shift to digital is not expected to revert back to branch-based openings even after the pandemic subsides.

Despite this shift in consumer sentiment, many traditional financial institutions still do not support online or mobile checking account opening. In fact, according to research by the Digital Banking Report, the percentage of financial institutions globally that stated the ability to support online account opening dropped since last year, with no change in the percentage of organizations that support mobile account opening.

While there was minimal difference in the support of online account opening based on asset size of financial institutions, there was a very strong correlation between asset size and the ability to support mobile account openings, with more than 50% of organizations over $10 billion supporting mobile openings. All megabanks (over $250 billion in assets) supported the mobile channel.

We also are seeing a shift in focus by the largest financial institutions. They are supporting upgrades to the mobile account opening applications much more aggressively than they are for online account opening. There is also a trend towards using the innovations in mobile account opening to support branch-based processes.

Read More:

- Becoming a ‘Digital Bank’ Requires More Than Technology

- How Bank of America and Chase Get Mobile Account Opening Right

Hybrid Digital Account Opening Not Acceptable

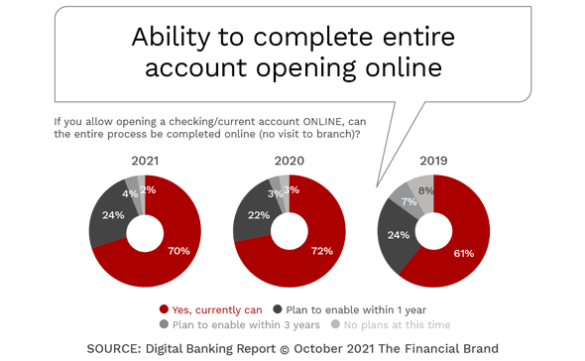

Consumers want to be able to complete account openings using only a single channel. However, only 70% of the institutions surveyed indicated that the entire online account opening can be done without coming into a branch. This compares with 72% last year and 61% in 2019. As can be seen below, the percentage of institutions that planned to move to single-channel functionality has not changed significantly in the past two years. This indicates that those organizations not already providing this level of functionality are putting a low priority on creating seamless experiences.

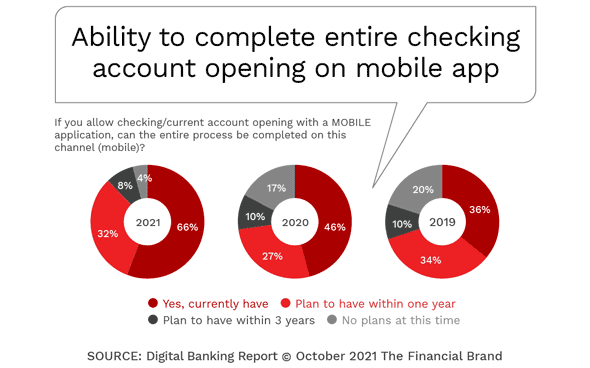

The focus on supporting checking account opening on a mobile app is evident in the significant increase in the percentage of financial institutions able to provide an end-to-end mobile account opening experience this year compared to 2020 (46%) and 2019 (36%). There is also a significant increase in the percentage of organizations planning to provide a complete mobile account opening experience within the next year (32%).

It is encouraging that only 12% of organizations that currently offer mobile account opening indicated that they either had no plans to offer end-to-end mobile account opening or had plans three years out. Last year, 27% of financial institutions had these longer-term aspirations. The primary reasons for not being able to complete a digital account opening without a branch visit were ID verification (73%), signatures (61%), documentation (51%) and the application itself (27%). All of these components are provided by digital account opening solution providers. They have been tested in the marketplace and meet compliance criteria.

Speed of Digital Checking Account Initiation Still Lacking

The advantage of digital-only banks is that they were built on technology that does not have the friction of legacy infrastructure. The focus from the origin of these organizations has been on speed and simplicity of customer experiences, setting the bar for traditional financial institutions. The excellent customer experience at the initiation of account opening is why digital-only bank account holders are expected to approach 55 million in 2025, up from 30 million this year, per Insider Intelligence forecasts. The number of customers of digital-only banks would compare to the combined active mobile users of Bank of America and Citibank … combined.

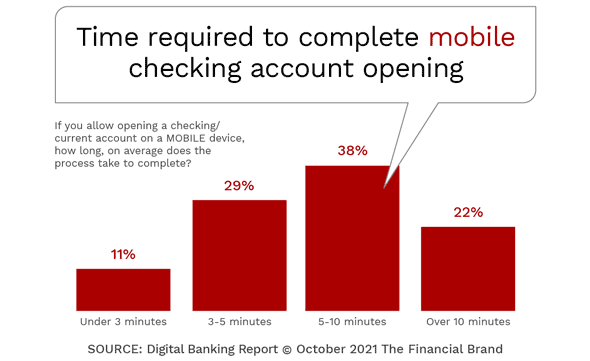

The increasing digital consumer population expects speed, simplicity and intuitive design when they want to open a new checking account. Unfortunately, while the number of organizations offering digital account opening continues to increase, the ability to complete an account opening online continues to be extremely slow. The research from the Digital Banking Report found that almost seven in ten of online account openings took longer than five minutes in 2021, with close to 30% taking longer than ten minutes. The improvement in the time it takes to open a new account online has changed very little since 2017.

The good news is that the time to complete a new account opening using a mobile device has improved significantly in the past year, with only 40% indicating a process of less than five minutes, compared to only 28% in 2020. It is also encouraging that over 10% indicated a new account opening completion speed of less than three minutes. The improvement in speed for mobile account opening reinforces the focus on supporting mobile account openings as opposed to using resources for the improvement of online channel openings.

Lack of Speed and Simplicity Inhibits Growth

In a digital world, it is unacceptable for a consumer to take longer to open a checking account digitally than it does to apply for a mortgage, buy a car, create an investment account relationship or get a loan. It is also unacceptable to not be able to complete the process on a single channel of choice.

A growing percentage of consumers use the internet to research, shop and open new banking relationships, often using their phone. For those consumers who want to save time and money, they want a seamless digital account opening experience that is fast. If the process is not built for digital speed, they will abandon the process and open an account with a provider that meets their time-restricted needs.

As mentioned many firms that can help traditional players to improve the digital account opening process. These firms can remove friction, increase engagement and improve customer satisfaction using time-tested tools and strategies. Most of these solutions can be implemented in a very short time frame, allowing traditional banks and credit unions to replicate the experiences provided by fintech and big tech firms.

Financial institutions must improve their digital account opening process by rethinking the back-office processes that inhibit speed and simplicity. This may require “starting from scratch” as opposed to trying to retrofit decades-old processes for a digital future.