Banks and credit unions are more eager than ever to leverage the latest technologies to boost efficiencies, improve the customer experience and enhance their brand. From instant account opening and marketing automation, digital capabilities enable banking providers to capture both profits and market share while developing relevant, one-to-one digital relationships with consumers.

While these capabilities were once nice to have, they’re now a necessary component just to survive. According to the Digital Banking Report, the lack of digital maturity now threatens the survival of many banks and credit unions, and more than half of those with assets under $10 billion say they haven’t made substantial progress toward their goals.

The Complex Journey to Digital Transformation

Many financial institutions are still working with siloed legacy systems that lack data functionality and can’t support modern data needs, digital channels, or marketing automation. As a result, financial institutions aren’t always using their consumer data like they need to if they’re to meet their consumers growing expectations. 80% of COOs believe their organization’s existence is threatened if they don’t update their technology to support rapid innovation, according to Accenture.

While these technology upgrades are now mandatory, they’re not always so simple. It can take three to five years to complete a core conversion, and on top of that many financial institutions are already locked into contracts that can span several years. Even when the path is visible, overhauling technology can impact internal resources and operations.

As a result, many banks and credit unions still have yet to take the first steps to address their underlying infrastructure requirements. Given the added pressures of changing consumer behaviors and the impact of the pandemic, alternative approaches that make this long and complex process more agile are emerging and gaining popularity.

Laying the Groundwork: 3 Approaches to Digital Transformation

Some say that if you have to do something painful, it’s better to “rip off the Band-aid” and overhaul everything at once. Others will argue that it’s better to break it down in smaller chunks.

What this looks like for each institution is different. When considering a digital transformation, here are three schools of thought (one of which we feel is superior).

Approach One: Incremental

Financial institutions typically have four major milestones in their digital transformation journey: 1. upgrading legacy systems, 2. updating the digital channels, 3. developing business intelligence and data analytics, and 4. marketing automation.

One approach to tackling these requirements is to go incrementally. Selecting a new core system and making the conversions is usually the first milestone (and the most time intensive process that can take multiple years). With a core system in place, financial institutions can then establish their digital channels (which can take another year to go live).

After that, they can add in a layer to query and report so the institution can extract data and use it in a meaningful way. Typically the last of the four tech integrations involves choosing a marketing platform that can be integrated with the infrastructure that’s been put in place.

Some financial institutions find the incremental approach less intimidating because it’s easier to get started. It also makes it possible to select best-of-breed vendors (smaller, specialized providers that offer an innovative or superior solution for a specific area of focus).

One downside of this approach is that tackling elements one at a time can be slow. And by the time they finish the last step, the first one may already need an update.

Approach Two: “Do-it-all” vendor

Banks and credit unions that prefer to manage fewer moving parts, might opt for an approach where they can work with a single, large do-it-all vendor who offers most of the functionality required for the financial institution’s digital transformation.

While integration may be pretty straightforward, this approach has its downsides. An important one is that financial institutions are unlikely to get best-of-breed in technology. Which means that in the areas that fall outside of the large vendor’s focus, the functionality will not be state-of-the-art and might require an additional update sooner rather than later. Additionally, many financial institutions have concerns with putting all their eggs in one basket and would rather hedge their bets by working with more than one vendor. Last but not least, large vendors usually have lots of consumers and a more standardized approach, which can be especially hard for the smaller institutions.

Approach Three: Concurrent

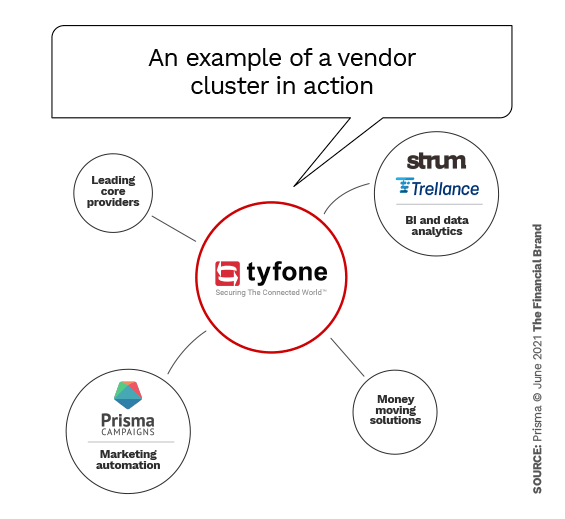

A third option, one that our partner Tyfone — a provider of digital banking solutions — excels at and that has become our recommended approach, is where a financial institution identifies the key projects that will propel their digital transformation and evaluates best-of-breed vendors who are suited to meet the specific strategic objectives of those projects. Providers are assessed at the same time for their agile mindset, interoperability and synergy.

Josh DeTar, Tyfone’s VP of Sales & Marketing, puts the importance of synergy among vendors succinctly: “As any financial institution evaluates their path for digital transformation, a few key points should be kept in mind. Move at the speed of digital, not the pace of banking. We can’t do it alone, find the right partners. Find partners who focus on building long-term relationships centered around a culture of continuous innovation.”

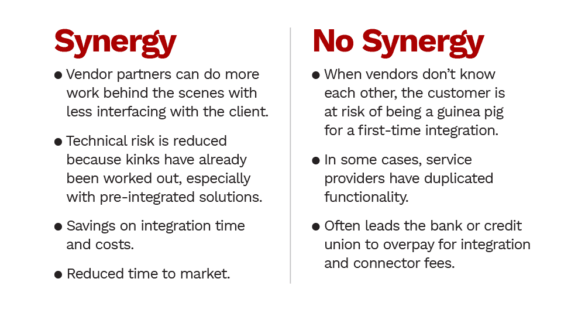

Here are just a few of the benefits of looking to clusters where solutions are already aligned and vendors have synergy with one another:

Vendor Synergy in Action

One great example of synergy in action is from SIU, a credit union that has been serving Southern Illinois since 1938. As they researched for a new core, they were aware that whatever choice they made, would also define the set of vendors they could work with in the future. In other words, choosing a core meant choosing an ecosystem. And so that’s how their choice of Corelation Keystone as their core led to Bankjoy as their digital channel provider and Prisma Campaigns as their marketing platform.

According to Mark Dynis, SIU’s VP of Marketing, “The longer you wait, the further behind you get. There’s no perfect time for it and we wanted to jump in as soon as we could. While features and cost are important, we do appreciate vendors that are good at relationships. We value their existing ones, as it makes integration easier for us, just as much as we value their openness to establish new ones with anyone else we may bring on board. Also, we’ve learned that even when the features are there, you can’t take full advantage of them if the vendor treats you as just another client. So how they work with us, intimately knowing our credit union, also matters.”

Numerica Credit Union, as another example, has been serving Eastern Washington state and the Northern Idaho Panhandle for over 80 years. When choosing providers, they evaluated and considered Prisma Campaigns as their marketing solution at the same time as their digital channel upgrade with Tyfone. Here’s what KayCee Murray, Senior Vice President of Information Technology said about how vendor synergy has benefitted their credit union:

“Numerica has benefitted from Prisma Campaigns’ partnership with Tyfone as we’ve prepared for our digital banking platform upgrade. Tyfone already understands the power Prisma brings to the table, while Prisma already has a blueprint for how to best match their solution with Tyfone’s platform. Numerica, Prisma, and Tyfone are collaborating to create a plan to ensure our members have a seamless transition to our new digital banking platform.”

Increasing Speed of Digital Deployment

Despite the urgent need to evolve and adopt the latest capabilities, many financial institutions still lack the underlying infrastructure to support automation.

Upgrading infrastructure can often be a multi-year (and sometimes unending) process, and while financial institutions can’t rush digital transformation, or avoid building their foundation, there are undoubtedly ways to ease transitions and smooth the road ahead.

Banks and credit unions can reap the benefits of digital transformation sooner by getting clear on their strategic objectives and based on that, choosing clusters of best-of-breed solution providers that have synergy with one another and are open to tackling each client’s unique needs with a collaborative, agile and iterative approach.

Additional Resources:

The 2021 guide to omnichannel marketing for financial institutions

Act like Amazon: how banks and credit unions can create a data-driven marketing strategy

Choosing a marketing automation platform – a guide for financial institutions