In a fall 2020 survey of over 150 banks and credit unions, Bottomline Technologies and The Financial Brand identified a significant “Engagement Gap” between large and small financial institutions regarding CRM and data management. While nearly 84% of all respondents identified proactive engagement and delivering personalized guidance as key goals, only three-fourths of respondents at large organizations, and less than 50% at smaller institutions, said they have the tools to achieve these goals.

Our new report, “The Rise of Intelligent CRM in Banking,” highlights how respondents, who ranged in size from less than $1 billion to more than $150 billion in assets, are prioritizing and investing in relationship management tools and reveals both interesting similarities and telling differences.

We expect many of the changes to how financial institutions manage client relationships — necessitated by the events of 2020 — to last. Clients across segments are re-evaluating how they choose their primary bank, demanding ever more seamless and digital engagement and showing a new openness to truly consultative virtual interactions. How each bank and credit union evolves their relationship management approach in areas including consolidating key customer engagement data across channels, using artificial intelligence and machine learning to predict opportunities and risks, and delivering a single, banking-specific relationship management platform across lines of business will play a crucial role in their growth and overall success this year and beyond.

Data – The Neglected Foundation of CRM Success

Traditional CRM systems have too often failed to deliver timely and complete information on each customer’s engagement across an increasingly broad range of branch, online, mobile and third-party channels.

In fact, 59% of respondents confirmed they can’t currently see a complete single view of each client, making this issue the most common challenge respondents identified with their current relationship management initiatives. In addition to completeness, data timeliness is also a key factor in delivering value from relationship management initiatives. For example, the 39% of survey respondents whose CRM solution doesn’t integrate with their marketing automation system are likely reducing campaign ROI through delayed follow-up on new leads.

Relationship management systems that successfully address these challenges deliver the openness to share data in real-time with a wide range of core, investment, loan origination, marketing automation, document management and other systems. They are also designed to store and apply this banking-specific data — including treasury service entitlements, payment activity, online engagement and master relationships spanning multiple lines of business without risky and costly customization. This enables institutions to reduce the blind spots that frustrate clients and lower trust and adoption among relationship teams.

AI and Machine Learning – From Cool Idea to Critical Need

Predicting and targeting high-value opportunity and risk is moving from a theoretical “nice to have” to a real and urgent need for banks and credit unions. However, 49% of our survey respondents indicated their current CRM solution doesn’t provide helpful analytics or recommendations.

Customers are choosing or being forced to engage in new ways, and are relying increasingly on digital and mobile channels. One implication is that the “long tail” of relationships that have traditionally been under-served are at even greater risk in today’s environment, in which client behaviors and needs are changing faster than ever.

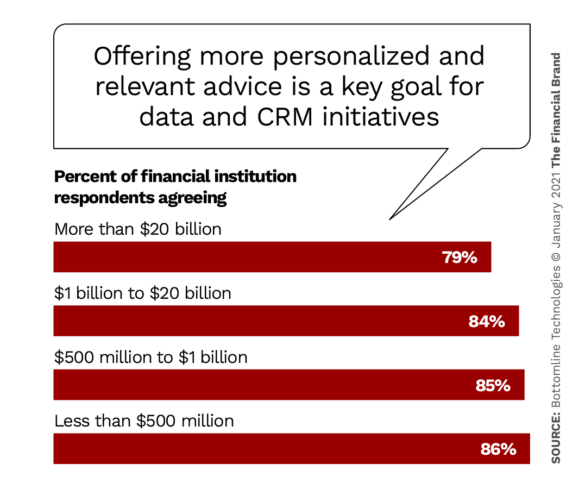

Recognizing this growing need, financial institutions of all sizes highlighted personalization as a key customer relationship management goal.

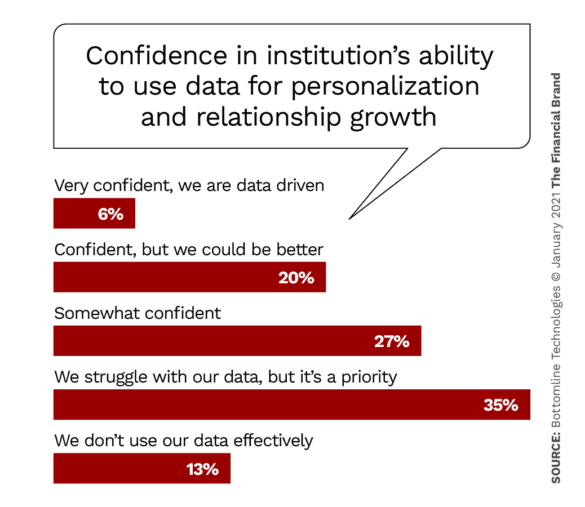

However, nearly 75% of survey respondents lack confidence in their ability to personalize engagement.

In response to new competitive threats and large-scale changes in when and through which channels customers choose to interact, the relationship management model must evolve to scale intelligently across ever-growing portfolios. Learning systems powered by artificial intelligence can play a key role in understanding changes in how each customer is behaving and engaging and in helping bankers accurately and consistently interpret the implications of those changes.

Coordinating Engagement Across the Institution

As financial institutions re-engineer business processes toward virtual interaction and break down data silos into a more unified digital experience, many banks and credit unions are also recognizing the need to further consolidate and share the tools retail bankers, commercial relationship managers, wealth advisors and others use to manage large and complex client relationships that span the institution.

Many of our respondents currently rely on fragmented or antiquated relationship management technologies: 25% of respondents reported using different relationship management solutions across different lines of business, while another 23% rely on email and spreadsheets to manage valuable client relationships. Another 27% of respondents currently utilize solutions from their core or loan origination provider or home-built solutions, which often struggle to drive bank-wide relationship visibility and collaboration.

However, we are seeing strong focus among market leaders on both information sharing and collaboration across business lines and the customer relationships that span them. This includes the ability to identify wealth clients without deposit relationships and master relationships whose youngest generation is starting small businesses. Large and complex relationship management teams spanning multiple locations and reporting structures also need appropriate visibility into these types of relationships, along with the ability to collaborate on sales referrals, share call reports and other relationship touchpoints, and collaborate to complete operational workflows using their relationship management tools.

Investing to Win

Not surprisingly, a number of survey respondents plan significant investments in relationship management capabilities to better support rapidly changing needs among their customer base and to ensure ongoing competitiveness in the wake of increasingly consultative and frictionless engagement offered by competitors.

Over 40% of respondents plan to invest in AI and machine learning to drive intelligent engagement, for example. In addition, 30% are moving away from fragmented or home-built relationship management tools to deploy a purpose-built relationship management platform.

This focus by banks and credit unions of all sizes on increasing the intelligence of relationship management and closing the gap between their desire and ability to engage clients consultatively bodes well for both the growth of these financial institutions and the depth and value of their client relationships.