The sharp falloff in credit card usage during the coronavirus recession has brought forth an interesting blend of innovation in product design, value propositions that rely on consumers’ hopes for a return to some semblance of the “old normal,” and renewed reliance on direct mail, that decades-old standby of card promotion.

It’s as if the very plastic most of the cards are made of was getting recycled into something that looks like the traditional card, but that is coming to be more than that.

This comes in a period where consumers have grown unhappy with aspects of the credit card business through much of the pandemic and the resulting economic slump. Their spending patterns changed drastically out of necessity and lack of opportunity.

New Entrants with a Retro Angle to Them

A taste of what’s going on can be seen in two innovative card introductions.

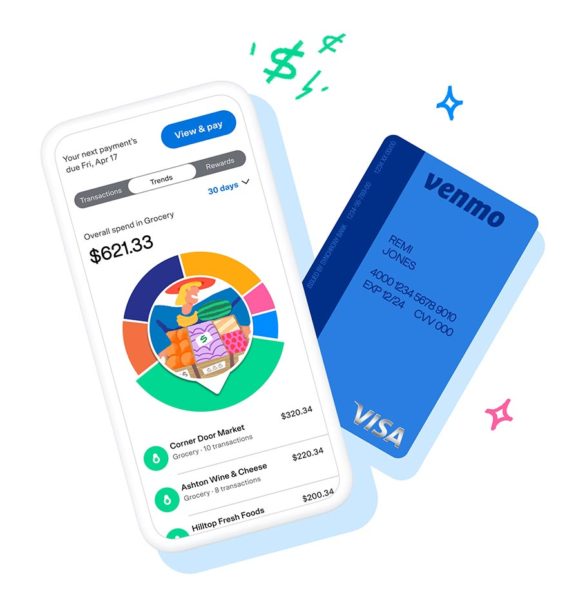

Venmo, the digital person-to-person payment service that has vied with the banking industry’s challenger, Zelle, gave its new Venmo Credit Card a soft launch for select users of the service.

Working with Synchrony Bank, Venmo introduced a payment vehicle that’s got something of everything. It personalizes its cashback feature to reward users with its top rate of 3% back in their own top spending category, and lower cashback rates for other spending. It allows cardholders to pay via two methods that eliminate or minimize contact — a unique QR code on the card and an RFID-enabled chip that permits tap and go transactions. The card can be managed directly in the Venmo app, including transaction alerts and freezes, and the card can be used in Venmo P2P payments — even cash rewards can be sent to friends. Online shopping can be done with a virtual card even before the physical card is delivered. Selected Venmo users can apply through their app.

Hotels.com and Wells Fargo launched a Hotels.com Rewards card that features “rewards that transform everyday spending into more rewarding travel.”

Travel? Now?

The new effort is not the first program during the pandemic to emphasize travel rewards. The card’s rewards program ties into the website’s preexisting program that turns “stamps” for hotel stays into free hotel nights. The card will turn spending into stamps.

Innovation is increasing as issuers have started to determine that COVID-19 will be with us for some time, according to Andrew Davidson, SVP/Chief Insights Officer at Comperemedia, a Mintel company. “We’re seeing this across the spectrum,” he continues. “Card companies have decided not to hold back on ideas and programs any longer.” More than a dozen new programs, many featuring collaboration between issuers and nonbank companies, have been unveiled as competition heats up.

The digital gorilla in the room is the Apple Card, which has been playing its cards wisely during the recession. “The Apple Card’s value proposition has become stronger and stronger,” says Davidson, as it adds more partners to its cashback program. Apple and its partners have been emailing heavily during the pandemic to drive signups and usage. Apple rolled out helpful accommodations early in the pandemic, including an outbound offer on mobile devices for relief that required only one button to be pushed. Many other issuers followed, some making relief easier to obtain than others, but Apple stole the scene.

“They were first out of the gate, in terms of helping customers,” says Davidson. And this comes at a time when research by J.D. Power indicates that many consumers have been frustrated or disappointed with their card issuers. “U.S credit card customers appear to be losing faith that their card issuers will be here for them when they need it most as the COVID-19 pandemic continues to drag on consumer confidence,” the firm stated in publishing its annual credit card satisfaction study.

Let’s take a look at the headwinds card issuers are facing, first, and then at how card marketers have been adapting to changing circumstances.

Consumers Have Been Cutting Back and Shifting Spending

In early October 2020 the Federal Reserve reported that U.S. revolving credit had fallen in August at an annualized rate of 11.3%. Total outstanding revolving credit, at $1.08 trillion at the end of the first quarter of 2020, had fallen to $985.3 billion in August, a period-to-period decrease of 8.6%.

“Consumers still think the worst is yet to come, financially.”

— John Cabell, J.D. Power

“Consumers still think the worst is yet to come, financially,” says John Cabell, Director of Banking and Payment Intelligence at J.D. Power. “People have gotten more miserly with their cards, spending less and paying them off.”

Davidson agrees: “The fallout hasn’t really taken hold yet.”

Cabell says that before the pandemic, 44% of consumers in the Powers samples were carrying a balance and 56% were paying their bills in full every month. Post-pandemic, he says, 39% have been carrying a balance and 61% have been paying off their balances. People have also changed what they use their cards for, with groceries, pharmacy charges and takeout dining now.

Cabell notes that a growing proportion of the nation’s jobs have not only gone, but won’t be back for the foreseeable future. In the face of increasing economic uncertainty and worse, the outlook for the card business isn’t promising. In a summary of a Mercator Advisory Group report on the card environment, Brian Riley, Director, Credit Advisory, states: “Credit cards are certainly not going away, but expect lower returns, higher risks and shifting purchase patterns at least through 2025.”

Looking at Today’s Card Economics

Though card interest rates have come down a bit, Cabell and Davidson note that they remain quite high compared to other market rates and that this may continue for a time. Riley states flatly that “Lending is a risk-based business; it requires a return for tolerating the risk.” While under certain circumstances consumers will pay what they must to keep credit card lines open for survival, this is generally unsecured credit, versus mortgages and auto loans.

The economics go beyond interest rate spreads. Cabell says most consumers feel they should be getting something for their credit card transactions — points, nights, miles, cashback or otherwise.

“The juiciest programs tend to have higher fees but those are in a state of flux.”

The juiciest programs tend to have higher fees but those are in a state of flux. During the first part of the pandemic many added more variations on rewards to make up for the fact that people couldn’t or wouldn’t travel. Davidson says a shift has begun back towards travel incentives, like the Hotels.com card, and American Express and Hilton have added to the perks in their co-branded card even as the megachain announced the permanent closing of its Times Square New York hotel.

“They are having an eye toward the future,” says Davidson, and counting on the influence of pent-up appetite for travel. “I find more and more companies are thinking longer-term.”

“Consumers have many personal financial issues and as card usage changes in terms of type and spending and people travel less, high-fee cards that offer formerly attractive perks and benefits are potentially going to become less satisfying,” says Cabell. “Cards with account fees may become less attractive down the road, and consumers may migrate to no-fee cards.”

Yet Riley points out that reward program costs already eat up much of the interchange income that issuers still get. “In a shifting market, all costs must receive consideration,” says Riley.

J.D. Power research indicates that, at present, consumers have a tendency to stick with the cards they have and many aren’t looking for more card accounts. “They are hanging onto what’s in their wallets now,” says Cabell.

But this could shift.

Cardholders Disappointed with Issuers’ COVID Performance

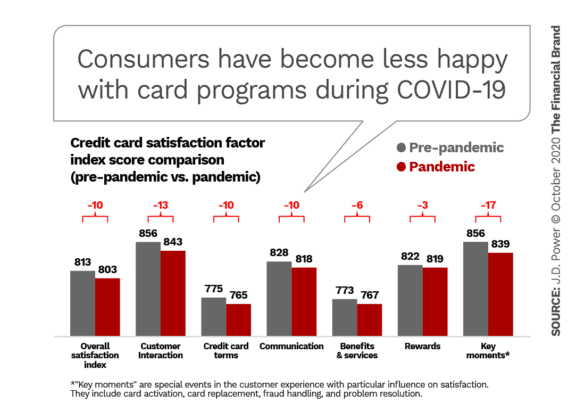

Indeed, there’s good reason to think that more card account switching could come. J.D. Power’s research indicates that many consumers are not happy with the way their issuers behaved early in the pandemic.

As the findings in the chart above show, the weakest links have not been in things like reward programs, but basics of customer service in a time of high stress. Contrast that with the word of mouth that the Apple Card’s outreach mentioned earlier has garnered.

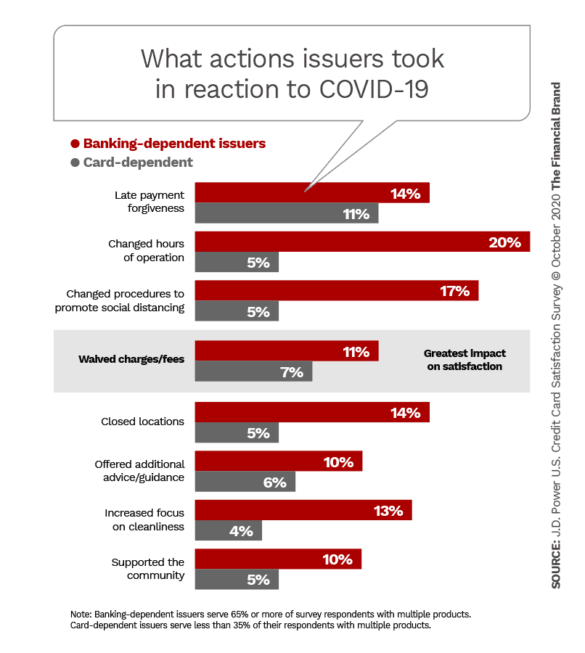

In terms of concrete actions taken, while some issuers took the steps outlined in the chart below, many didn’t. The one that J.D. Power identified as being most meaningful to consumers — waived charges and fees — were granted by comparatively few issuers. Note that both the Venmo and Hotels.com cards covered at the beginning of this article are no-fee offerings.

Cabell notes that 2020 card satisfaction levels, overall, seemed pointed towards record levels in January and February 2020. “But that all reversed course when COVID-19 entered the equation, with satisfaction, trust, advocacy and brand image attributes resulting in sharp declines.”

Cabell believes holding onto accounts in the long term will demand big improvement in communication with disgruntled customers. Email is the preferred channel for this, but strong communication through all digital channels is growing in importance and call center efficiency is at a premium.

Interestingly, the strongest impact has been seen at the extremes — the affluent and mass affluent consumer segments and among those financially hit by the pandemic. J.D. Power found that mainstream banking and mortgage lenders are seen as much more proactive in communicating with consumers during the pandemic than are card issuers.

An Intriguing Shift Takes Place During the Pandemic

The shift to digital channels throughout the pandemic has practically become a mantra in financial services, but Davidson says that Comperemedia, which has a massive network for tracking what consumers are receiving from marketers in major channels, found a strong contrarian trend.

During the pandemic credit card acquisition direct mail marketing picked up by 50%, while promotion via digital marketing was actually cut back. Davidson says that while digital has picked up a bit, it remains down historically.

Why have credit card marketers been leaning on this classic marketing channel?

“It’s about credit card marketers going back to basics,” says Davidson. While digital outreach has been a growth factor in recent years, the biggest cardholder bases were built largely on ads in envelopes or glossy postcards.

“The shift back to direct mail is about credit card marketers going back to basics.”

— Andrew Davidson, Comperemedia

This shift goes beyond the media used. Davidson says many of the offers being made are based on “pulled credit scores.” That is, card marketers are compiling lists of acquisition prospects based on their established credit scores at bureaus.

It’s a very vintage way of targeting potential cardholders, “but it’s a less-risky approach,” according to Davidson, in the marketers’ view. This ties in with reports that issuers have been tightening up on credit standards for new accounts. These classic methodologies can help narrow the field for issuers.

‘Pockets of Opportunity’ with Honed Marketing Pitches

While marketers and issuers of new card concepts face the dual challenges of consumers holding onto the cards they already have and constraining their card spending at present, Davidson believes there are what he calls “pockets of opportunity” that represent potential growth for issuers willing to work at it.

Synchrony’s partnership with Venmo, for example, gives it a potential fresh base of 60 million Venmo app consumers for the new card, once it is rolled out in full.

Two pockets that Davidson has identified that issuers are going after are tie-ins with home improvement and with auto purchases. The first has been doing very well during the pandemic, and auto sales are back on an upswing both for new and used models.

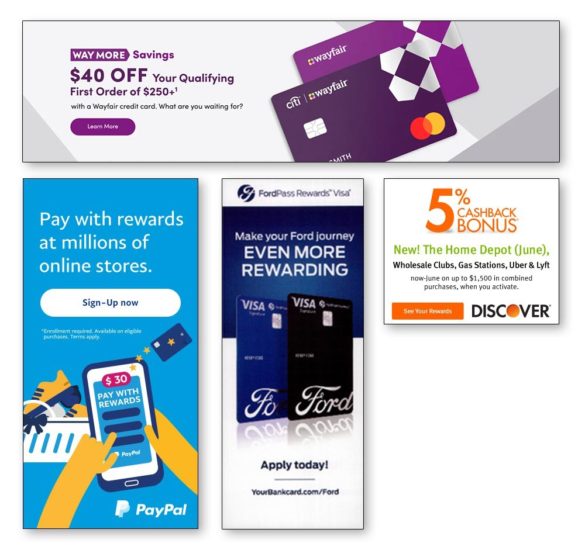

Citi, for example, launched a new card partnership in September 2020 with Wayfair, the home furnishing retailer. Two cards are involved, one a private label card and the other a co-branded Mastercard. Both offer a choice of 5% rewards on Wayfair purchases or no-interest financing. Discover Card added Home Depot to the sellers where cardholders can earn 5% cashback bonuses on charges.

In the auto area, FNBO and Ford launched the FordPass Rewards Visa card in August 2020, which ties the card and its app to the car. Activity can build to levels entitling the holder to free maintenance work and rewards can be earned that are redeemable toward other dealership purchases. The app attached to the program can also link to the holder’s vehicle, to show gasoline and other levels and even to unlock the door if the keys were left inside. The app also connects the user with roadside assistance.

GM and BMW are involved in card deals with banks, Goldman Sachs and U.S. Bank, respectively.

Davidson also thinks that as the recession deepens, secured cards will represent a growing opportunity. Heretofore they have been something of a niche product, although Amazon and Synchrony launched a joint secured product — Amazon Credit Builder — in 2019. Davidson notes that Chime, the popular challenger bank, has launched a secured card.

“Even in times of economic distress,” says Davidson, “people need to build their credit strength.”