At a time when most traditional banks in the U.S. are falling behind consumer expectations with respect to providing basic mobile banking services, Moven continues to blaze a trail of innovation that disrupts conventional banking paradigms. With the advantage of building a mobile banking platform from scratch, CEO and founder of Moven, Brett King was joined by Moven president and co-founder Alex Sion as they presented what some are coining ‘Bank 4.0’ at Finovate Spring in San Jose.

The introduction of its new Impulse Savings feature was one of several major expansions and enhancements to Moven’s overall experience that was introduced to another sold out crowd of bankers, investors, news media and others interested in fintech innovations. Moving beyond providing insight into spending behavior, Moven customers will have access to tools designed to encourage savings behavior and thus improve overall financial well being.

Data-Driven Contextual Experience

The 2015 Retail Banking Trends & Predictions report says the future of digital banking will combine four key elements underrepresented in the majority of today’s mobile banking apps:

- Data-driven contextual experience

- Highly visual mobile-first design

- Integrated share of wallet expansion potential

- Expansion beyond the smartphone

The new Impulse Savings feature leverages Moven’s existing real-time contextualized notifications, including instant receipts that automatically categorize every transaction, as well as an updated, color-coded Spending Meter® and app home screen, making it even easier for users to turn spending insights into savings behaviors in line with the app’s financial wellness mission.

According to King, “The entire app responds to the user’s behavior, using proprietary gamification and behavioral design to eliminate the need for budgeting in order to save. Users can track their spending, seeing how much and how fast they are saving in real-time.”

“Most banks have some form of mobile notification, a smaller number have actionable notifications, but Moven’s contextual notifications raises the bar for all FIs in the U.S.,” stated Alex Jimenez, SVP, Digital and Payments Innovation at Rockland Trust and an attendee at Finovate Fall. “Context gives intelligent emotion to real data. People need to believe in themselves first, then achieve success to change self-defeating behaviors,” added Lisa Kuhn Phillips, founder of inaVision, LLC.

Mobile-First Design

Very few traditional mobile banking applications in the U.S. provide innovative ways to save or provide incentives for positive behavior. This is one of the reasons alternative providers such as Digit and other fintech players continue to develop new mobile applications.

Moven is one of only a few truly innovative banking organizations in the U.S., stated Michal Panowicz, deputy head of digital banking at Nordea and previously with mBank. While mBank, La Caixa, Garanti, Denizbank, Kotak Mahindra, Hana Bank, Idea Bank, CheBanca! and quite a few others are impressive fintech innovators worldwide, the largest U.S. financial organizations are lagging international leaders in the online and mobile banking arena.”

The Impulse Savings app from Moven introduces several innovative feature including:

- ‘Lock Away Savings’ Prompts: With ‘lock away savings’, users are notified whenever their spending behavior has placed them far enough in the green (below their average spending) that it makes sense to set money aside. Moven gamifies that moment, turning that typical impulsive spending moment into a savings moment. This savings feature is perfect for the wearable form factor.

- Visual Wish List Leveraging Pinterest, etc: The ability to set up a visual wish list of items a user wants to save for, as well as the option to quickly and simply curate these directly from a user’s Pinterest board and others in a few simple taps.

- ‘Break the Glass’ to Unlock Savings: When users have reached a savings milestone, they can access their savings by tapping the app interface three times to simulate ‘breaking the glass’ – employing simple behavioral gamification to make the user think before spending their hard earned savings. If they proceed, their savings funds are immediately transferred into their Moven spending account for their desired purchase.

“It’s refreshing to see a unique way to redirect the strong energy behind typical buying impulses and the craving of material belonging into savings,” stated Duena Blomstrom, FinTech and Digital Experience Specialist at Duena Blomstrom Consulting. “The banking industry needs more ways to change current addictions to shopping into addictions to savings. Using gamification concepts may be the path to intensely emotional contextual Money Moments of Saving.”

“It’s refreshing to see a unique way to redirect the strong energy behind typical buying impulses and the craving of material belonging into savings,” stated Duena Blomstrom, FinTech and Digital Experience Specialist at Duena Blomstrom Consulting. “The banking industry needs more ways to change current addictions to shopping into addictions to savings. Using gamification concepts may be the path to intensely emotional contextual Money Moments of Saving.”

Integrated Share of Wallet Expansion Potential

The majority of today’s mobile banking applications do a terrible job of selling additional services based on contextual insights. Banking in general is steeped in traditional product silos and have a difficult time viewing their products from a consumer perspective (selling loans as opposed to providing real-time borrowing solutions).

There are exceptions, such as with mBank’s 30 second mobile loan application and PNC’s virtual wallet, but these are exceptions. “It is clear that unbridled by technology legacy platforms, and critically bulging business unit and product divisions who stifle most traditional banking product innovation, Moven is inspired and able to deliver services that customers will actually want, use and benefit from. The products and services offered by traditional banks today haven’t fundamentally changed since the 1800’s merely how they are distributed. In most cases, this is the equivalent of trying to sell vinyl through the Apple Store,” states David M. Brear from the London-based Think Different Group Ltd.

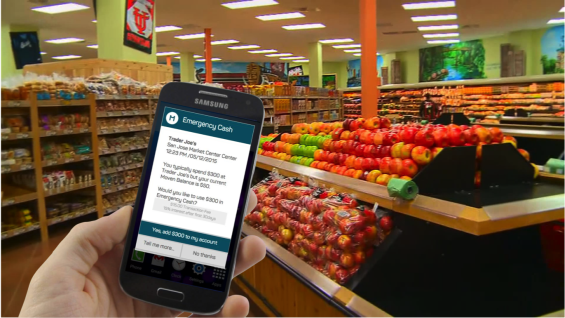

To combine checking, savings and lending services, Moven unveiled its Emergency Cash feature to provide users the spending capacity for their regular purchases beyond current balances. The emergency cash notification leverages GPS-technology to alert users when funds are low as they enter their favorite or most frequented places.

Using Moven’s real-time behavioral insights on a user’s typical spending habits at any location (i.e. average grocery shopping bill), users receive a notification offering them a real-time overdraft opportunity. This notification comes with a transparent upfront fee, to help bridge the gap between typical spend at the location and their current balance. The emergency cash advance is settled when the next deposit is made.

The benefit of this integrated solution is a breakdown of traditional product silos and the ability to increase share of a consumer’s wallet in real time, eliminating the traditional friction of an overt sales process.

“With Moven’s contextual savings and credit, we’ve eliminated the need for separate products like checking, savings, overdraft, credit card and fixed deposits. We’ve replaced these silos with contactless payments and a real-time receipt, impulse savings, emergency in-store cash, wish-list savings and eventually, the potential to gamify your savings rate through referral,” stated King.

After seeing the new application, David Gerbino from DMG Consulting said, “What King and Sion and the rest of the Moven team have done is to begin the process of eliminating traditional bank products and services that were operational constructs and replaced them with a financial offering designed to aid its users in managing and improving their financial well being.”

Expansion Beyond the Smartphone

One of the early pioneers in integrating banking beyond the smartphone, Moven will enhance many of these compatibilities with the benefits of wearables. Impulse Savings will be made available via wearable devices, such as the Android Moto360 and Samsung Gear smart watches as well as the Apple Watch.

Users on all these devices will be able to receive instant receipts, see insights on their spending habits via the Spending Meter® and be gently nudged to save their spare cash via the new Moven apps. According to Alex Sion, Moven’s wearable strategy is not to deploy an app on a watch or on smart glasses, but to provide experiences or insights that are optimized for the location or the moment.

“Moven has taken the checking account, savings account, overdraft, credit card and fixed deposit or CD and we’ve made an app that provides savings, payments capability and credit in real-time, based on context,” said King. “However, perhaps the greater innovation is the removal of budgeting, or what we call the envelope or ‘goals’ personal financial management (PFM) concept, in favor of accelerated savings behavior via gamification – you don’t need any discipline or plan, no financial education or literacy … you literally just use the app everyday and it will help you save.”

“Moven gets moving again and has becomes an integral front end system for many banks. In other words, it is now the innovative front end software house for banks, but not a bank. It will be interesting to see how that pans out as their software becomes the customer interface of choice,” stated Chris Skinner, Chairman of the Financial Services Club and author of the book, Digital Bank.

“What Moven has captured is the shift from primary financial institution (PFI) to primary financial application (PFA),” stated Bradley Leimer, industry thought leader and Finovate attendee. “They have developed a tool that provides an aggregated view of a consumer’s financial life, including real time payment analysis and a contextual savings tool. They have also shown the power of moving from traditional push notifications to actionable real-time insights. This is a significant step in the evolution of the Fintech space.”

While Moven was initially introduced as a mobile-based alternative to traditional banks, it has recently moved beyond its home market of the U.S., partnering through licensing agreements with TD Bank in Canada and WestPac in New Zealand. To expand this initiative, Moven and Accenture announced a collaboration in deploying Moven’s experience-as-a-service platform at Finovate.

According to King, the alliance with Accenture will help Moven expand the distribution of their next-generation digital platform globally, reaching tens of millions of users worldwide.