The massive cross-selling fiasco at Wells Fargo has put bank and credit union incentive programs under the microscope. What changes should boards and senior leaders make to keep their brands intact and their employees on the right track?

Executive compensation consultancy Pearl Meyer has released its research findings on changes to retail banking incentive plans in the wake of the Wells Fargo scandal. The firm asked senior bank executives and board members to share their reactions, including how their retail incentive programs are structured and what plans they have- or will develop to mitigate future risks.

One thing is clear from the study: everyone in banking is aware of what happened at Wells Fargo and is concerned about the potential fallout.

Seven out of ten respondents in Pearl Meyer’s research said that they had recently received questions from senior managers about their organization’s incentive plan, while half have had received questions from the board, and a third had fielded inquiries from employees.

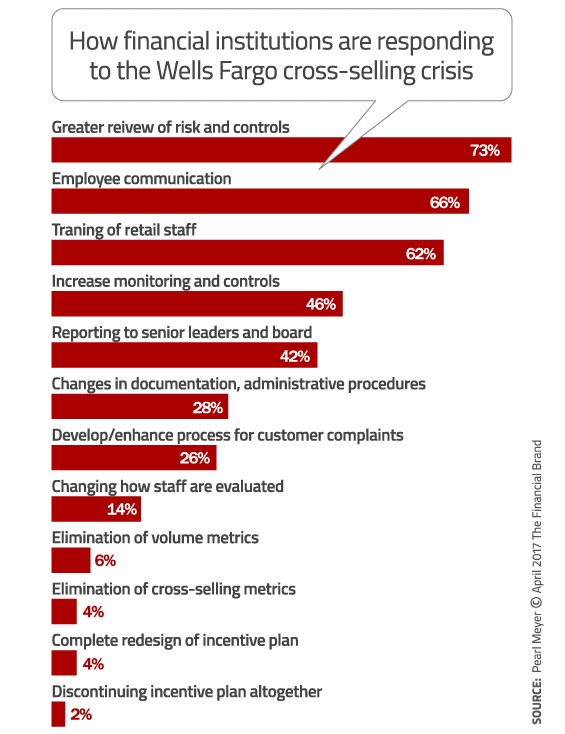

In response, a whopping 73% of bank leaders said they are now conducting a review of their risk and controls, and 28% are also planning changes in their documentation and administrative processes.

About half of respondents (55%) are using volume metrics and/or cross-selling metrics (47%), which have been criticized in the context of the Wells Fargo situation. 70% say they are using growth metrics, and 34% are using profitability or revenue measures.

How are banking providers reacting? The survey indicated that most are concerned about reducing risk. To shore up any potential trouble spots in their incentive plans, more than 60% are enhancing employee communication and retail staff training.

42% say they will be proactively reporting key cross-selling and incentive metrics up to senior management and the board. And a quarter of respondents are developing or enhancing customer complaint processes.

Only a third say they don’t currently have any plans to take direct action with respect to their retail incentive plans.

“Boards must challenge non-action and ask management teams to defend why the status quo is the best course of action,” says Laura Hay, managing director at Pearl Meyer. “The stakes are too high.”

“It’s not enough to simply look at the incentive plan’s structure and metrics,” Hay continues. “Risk can also be found in the process, controls, and administration of the plan. To properly assess risk, the board needs information on these aspects in addition to plan design.”

Read More: What Created Wells Fargo’s Corrupt Cross-Selling Culture? Toxic Execs

5 Questions About Every Financial Institution’s Incentive Plan

Pearl Meyer says there are five questions that banks and credit unions should ask themselves with respect to their retail incentive programs.

1. What does your plan reward? Pearl Meyer recommends using metrics that are difficult to manipulate and that help reinforce positive behaviors. For instance, Hay says it’s much harder for employees to game growth, profitability or revenue metrics — numbers that really matter.

“Using either volume or cross-selling metrics may put additional pressure on banks to demonstrate how their controls and administrative procedures curtail fraud or misconduct,” says Hay.

Pearl Meyer says that as long as any single metric in your incentive plan’s overall scoring system represents less that 20% of the total score, it is unlikely to draw excessive attention from employees or encourage unwanted behavior.

2. How is your plan monitored? You need to make sure you’re capturing the right data, particularly to help your board ensure the incentive compensation scheme doesn’t encourage inappropriate risk. In Wells Fargo’s case, that data may have been collected, but the board claims they were kept in the dark. According to Pearl Meyer, this is a common problem.

“Directors often have no visibility into retail incentive plans, nor any easy way to quickly understand the impact,” explains Hay. “They do not know what their rights or authority are in understanding, determining, and remedying the risk, so there is no plan for how to react. These issues need to be addressed to appropriately monitor the risk.”

3. Are your expectations reasonable? Pearl Meyer cautions that overly ambitious goals may encourage bad behavior, as evidenced by the actions of thousands of Wells Fargo employees.

“Collect data over time to see trends in performance, expectations and payouts,” recommends Hay. “This can identify unreasonable expectations, or flag the need for better training or management.”

“Cross-sell for the sake of cross-sell is going to come back to bite you. We should be thinking, ‘How have we solved a need for a customer?'”

— Nitin Mhatre, EVP at Webster Bank

4. What are your customers experiencing? You should implement mechanisms to ensure that the incentive program you’ve put in place actually has a positive impact on customers and not just your bottom line, or you could pay the price later — a public backlash, or worse. You should consider implementing mystery shopping techniques to get a sense of the sales experience — e.g., do employees use high-pressure tactics?

Pearl Meyer says you not only need to be able to manage individual issues, but also analyze feedback that can identify major trends or more broad, systematic breakdown in the customer experience.

“The process should not only handle specific complaints but also aggregate the complaint types to identify systematic breakdowns in the customer experience,” adds Hay.

5. Are you staying true to your values? You should also monitor employee feedback and satisfaction too, allowing them to provide input without fear of any backlash, according to Pearl Meyer.

One of the biggest problems with Wells Fargo’s cross-selling incentive plan wasn’t the carrot, it was the stick. Employees were afraid that if they didn’t hit their numbers, they’d lose their job. It was clear to everyone at Wells Fargo how important cross-sales were, so most staffers — even many senior managers — didn’t feel safe criticizing the program, despite its many obvious problems.

“Monitoring of employee satisfaction and providing mechanisms to provide feedback without repercussions — can help identify problems before they escalate,” Hay concludes.

Read More: Acquisition, Onboarding and Cross-Sell Marketing Showcase

Managing the Risks of Rewards

“We need to do a better job in teaching our front-line employees to speak up when something doesn’t smell right.”

— Ed Dwyer, Chief Risk Officer at U.S. Bank

Matt Turner, Pearl Meyer’s managing director in Chicago, says financial institutions conduct an annual risk review of their employee incentive plans to ensure the data being reported back from the frontline is genuine. This might include stiffening controls and enhancing audits. For instance, you might require “positive proof of customer intent,” as Turner puts it. Or you could conduct random audits of customer relationships.

Turner also recommends that you make it explicit in your organization’s employee compensation policy that any employee behavior that has a materially adverse impact on the company’s brand or reputation are grounds for clawing back incentive pay.

“While such language may call for subjective evaluation, that seems manageable and worth the enhancement,” Turner says. “Such a provision goes beyond Dodd-Frank requirements, but that could change by the time Congress is done investigating this scandal.”

Ultimately, Turner says it is leadership’s responsibility to make it clear that the trust and confidence of customers is paramount, and that the organization has zero tolerance for unethical behavior.

“Look for opportunities to reinforce the message,” Turner says. “Both internally with employees, and externally with other stakeholders.”