At a time when most banks and credit unions are trying to improve their mobile banking offering, a research report from the fintech and digital commerce research firm, Futurion finds that mobile design and customer experience criteria predicatively drive usage. The Mobile Deposit Benchmark Report by Mitek, analyzed customer experiences, adoption and usage patterns for 15 of the top financial institutions in the United States.

“Mobile deposit is one of the most powerful options available to financial institutions for driving customer loyalty and increasing adoption of all the mobile services that migrate routine transactions out of the branch,” said Jim Van Dyke, CEO, Futurion. “For all financial institutions that wish to remain competitive, it is crucial to provide mobile customers with welcoming and easy-to-use apps that are free of unreasonable limits, restrictions or fees.”

Key findings from the study include:

- There are significantly different mobile deposit customer experiences from institution to institution.

- Customer experience rankings of mobile deposit apps have a strong correlation to adoption, usage and growth.

- There are specific ways to improve the mobile banking customer experience that can drive significant growth.

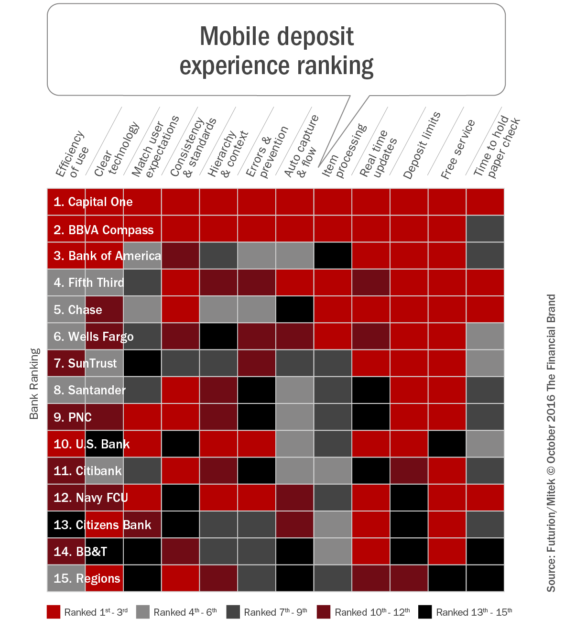

- Capital One was found to provide the best experience for mobile deposit customers, with BBVA Compass, Bank of America, Fifth Third Bank and Chase rounding out the top five banks that have exceeded the majority of their customers’ mobile deposit expectations.

Mobile Banking Apps Not Reaching Potential

Most studies of mobile banking usage continue to show high adoption of the balance inquiry feature with limited use of other mobile banking features. For instance, despite significant benefits to the consumer and financial institution alike, mobile deposit has experienced limited adoption — only four out of 10 banking customers have ever mobile deposit, and only 53% of those are highly active users.

A key reason for low adoption is that banks’ customer experience and related policies need improvement, and are likely the fundamental reason why there has not been explosive growth in mobile deposits or other mobile apps. According to the report, nearly three-quarters of a typical financial institution’s mobile deposit adoption and usage can be predicted by the strength of their customer experience.

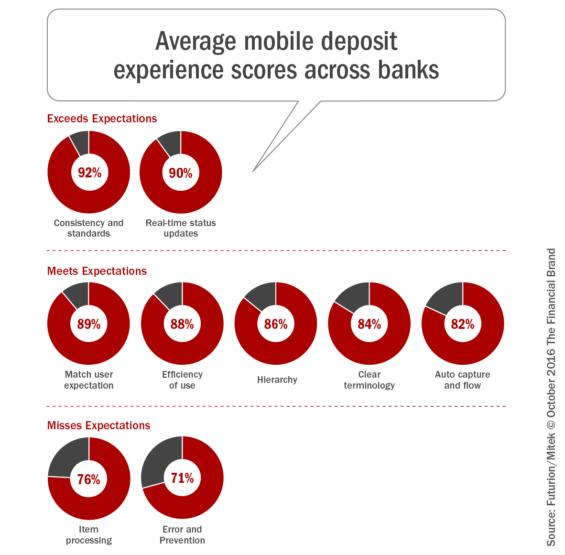

The mobile deposit benchmark study tracked 51 heuristics, plus policy and fee practices, to identify how customer-friendly each of the 15 banking’s mobile deposit offerings were. It was found that the customer experience ratings of the banks analyzed were vastly different. Adoption and usage rates were strongly correlated.

“For an app that helps you more rapidly, safely, and conveniently get access to your money, you just can’t market your way around a second-rate customer experience,” said the report.

Mobile Deposit App Rankings

For this research, the first nine user experience or heuristic ratings reflect the degree to which a customer can find the named feature on their mobile app, how successfully they’re able to access help during the process, and how well they can locate and/or use an auto-capture feature. Additional categories examined whether customers have lower deposit limits for mobile banking vs. an ATM and if customers were asked to retain their physical checks for extended periods of time (e.g. 30 days) after deposit? These policies can create apprehension and distrust for users who think it’s not safe to use mobile deposit compared to a branch transaction.

The chart below shows ratings for the top 15 banks and how they scored in terms of their customer experience measures.

The research found that the banks’ customer experience benchmark standings were closely correlated to the success they achieve in customer adoption, levels of activity, and growth. In fact, nearly three quarters of a typical financial Institution’s mobile deposit adoption and usage can be predicted by the strength of their CX.

Improving Mobile Customer Experience

As would be expected, the best way for any financial institution to improve their mobile banking app usage is to focus on customer experience areas in need of improvement. This can also prove to be a differentiator in a marketplace where not all apps are viewed as equals.

For instance, instead of focusing on areas where an organization meets or exceeds expectation, a bank or credit union trying to improve mobile deposit adoption and usage should focus on tailored error messaging and item processing communication that help users understand and correct issues that pop up while using mobile deposit.

Removing Negative Customer Experiences

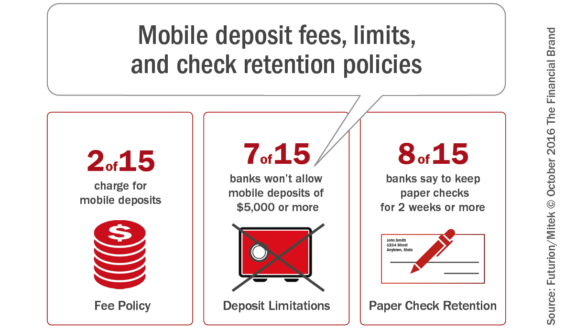

One of the overall findings of the research was that most banks continue to view mobile banking applications as cost-savings opportunities as opposed to a way to improve the digital consumer experience. The research found that two banks went a step further and use mobile deposit as a revenue generation opportunity, charging consumers for the service. This was found to impact adoption rates.

In addition, banks’ guidelines on how long to retain paper copies of checks had wide variations as did the mobile deposit limitations. Top-rated Capital One allows $10,000 in deposits for both new and returning mobile deposit users, in comparison to just $500 for new BB&T customers or $5,000 for returnees at nearly half the banks in our study.

Since mobile deposit is competing against branch and ATM channels that don’t impose deposit limitations and have a higher proportion of funds available immediately, this impacts usage. In my personal experience, my personal account at Wells Fargo has a significantly higher mobile deposit limit than my business banking relationship at PNC. Given the relative size and activity with both accounts, the limits defy logic from a CX and relationship management perspective.

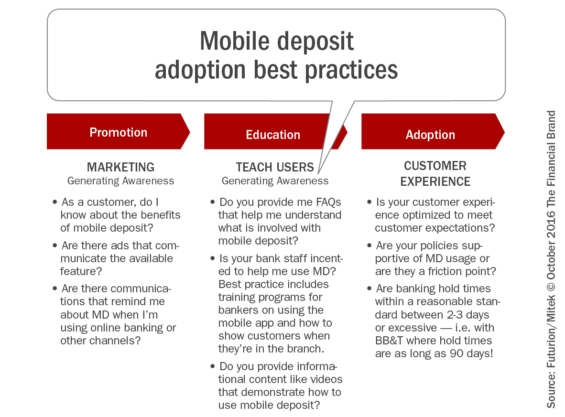

Mobile Deposit Adoption Best Practices

Overall, the study found that investment in CX should be expected to go hand-in-hand with all important measures of customer adoption or usage. However, a review of the impact on a banking organization’s most inactive mobile app users will provide insights into initiatives that are falling short.

“Customers need to know that features exist, they want to learn how it works, and they seek support fromtraditional channels such as branch tellers, bankers and through the phone. If bankers are unaware of policies or are hostile to mobile deposit adoption because it reduces branch traffic, this may cause customers to be skeptical of using the service themselves,” stated the report.

Exclusive Interview with the Author of the Mobile Deposit Research

Jim Van Dyke, CEO and founder of Futurion, discusses the findings of the 2016 Mobile Deposit Benchmark Report, sponsored by Mitek.

What were your goals when you started the development of the 2016 Mobile Deposit Benchmark Report, and how did you go about achieving them?

Jim Van Dyke: This was an unusually insightful project, because we started with a particularly important, but unproven, hypothesis. Our goal was to assess how much customer experience (CX) design truly impacts customer adoption of mobile deposit functionality across the largest retail financial institutions.

Everyone has heard product or design experts say, “If we build it, they will come”, but exactly how true is that statement? More specifically, we took 15 seemingly similar implementations of mobile check deposit, conducted a precise assessment of how customer-friendly each one was, and looked at customer adoption rates for each of those 15. The overarching finding was that, despite the presence of so many factors that can influence customer behavior (employee training, marketing, years since implementation, etc.) customer experience and customer adoption are remarkably highly correlated, measuring .72 on a 0-1.0 scale.

So if banks (or credit unions) build a better customer experience, customers/members will use the service at a higher rate?

Jim Van Dyke: Yes. While we didn’t rate other factors beyond CX, the strong correlation indicates that customers respond based on how welcoming or friendly the experience is.

Our analysis covered 9 heuristics capabilities such as consistent terminology or placement, the ability to get status updates, and the presence of important functions like auto capture to make it easier for the customer to know that their image can be used by the bank to process the payment reliably and quickly. Our research also included pricing variables since two banks (Regions and U.S. Bank) charge for the service. Finally, we also measured variables that varied significantly between institutions like deposit limits and how long the bank recommends consumers to hold on to checks after deposit.

Bankers are already telling us that they didn’t think the CX of mobile deposit really differed that much from one bank to another, yet our data on the 56 CX criteria told a different story and correlated strongly to adoption and usage patterns.

What do you mean by ‘adoption patterns’? Are you saying that you measured more than just how many users a particular bank had? And what does this adoption comparison really tell us?

Jim Van Dyke: We measured several aspects of adoption for each of the 15 large retail financial institutions, including the percent of customers who have ever used mobile deposit, the proportion who use it on a high-frequency basis, the proportion who have essentially lapsed after using it long ago, and how fast the bank’s adoption has grown since 2013.

The proportion of lapsed users was found to be a stronger indicator of how customer-friendly the banks’ app was, but every adoption measure had a strong correlation to customer experience. So, while bankers might think their implementation of mobile deposit doesn’t differ significantly or even matter much when it comes to adoption, our analysis proved that CX matters to consumers.

The primary takeaway is that I could essentially take only the CX scores for each of the top 15 banks and predict how strong their adoption is with high accuracy, and the opposite is also true!

Of the banks analyzed, what were the main differences, and what should banks and credit unions focus on to become better?

Jim Van Dyke: Capital One and BBVA were the two highest-rated customer experience institutions in our study, and they have the adoption rates to match. Their apps are easy to use, they don’t charge a fee, and they don’t send a mixed-message by setting deposit limits for mobile that are inferior to that of ATM or branch channels. The apps of the leading banks are highly-intuitive, almost like the difference between driving a new car where everything is “in the right place”.

Alternatively, the lowest ranked institutions did poorly in the categories of auto capture & flow and matching user expectations, penalize customers with some of the most limiting monthly deposit limits, and risk undermining customer confidence by recommending that they hold on to paper copies for longer than all of the other banks. It’s almost as though the lower ranked banks’ own team members don’t appear to trust the app, which is certain to be picked up by their customers.