As a companion to the highly acclaimed article reviewing projections for 2016, the 82-page Digital Banking Report, 2016 Digital Banking Trends & Predictions, provides a detailed analysis of the ten most important changes expected to impact the financial services industry in 2016. The report includes 29 charts and graphs, expounding on each of the trends and representing the most comprehensive analysis in the industry.

As a companion to the highly acclaimed article reviewing projections for 2016, the 82-page Digital Banking Report, 2016 Digital Banking Trends & Predictions, provides a detailed analysis of the ten most important changes expected to impact the financial services industry in 2016. The report includes 29 charts and graphs, expounding on each of the trends and representing the most comprehensive analysis in the industry.

As mentioned in the crowdsourced article, the partnership between fintech firms and legacy banking organizations is the #1 expectation for 2016. This transition of start-up firms from competitor to collaborator reflects the increasing need for banking to digitalize all aspects of the business model and the need to meet the increasing needs of the digital consumer.

This year’s report is sponsored by Kony, Inc., which allowed us to collect insights from more global leaders than ever before and provide the depth of insights that can be used for planning and analysis during the upcoming year.

Top 10 Retail Banking Trends and Predictions

The top ten retail trends covered in the Digital Banking Report include:

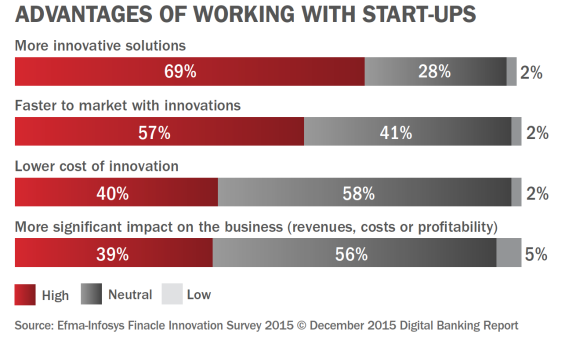

1. Partnership Between Banking and Fintech. Instead of competing, banks and fintech firms will partner more than ever in 2016, leveraging the banking advantages of scale, stability, trust, experience in navigating regulations and the access to significant capital. Conversely, by leveraging the agility, innovation culture and technological expertise of fintech firms, banks .

2. Removing Friction from the Customer Journey. It is no longer adequate to wait until the customer walks into a branch or decides to purchase a new product online or via a smartphone. Instead, banks and credit unions must engage customers at every stage of their purchase journey – not just because of the immediate opportunities to convert interest to sales, but because two-thirds of the decisions customers make are informed by the quality of their experiences all along their journey.

2. Removing Friction from the Customer Journey. It is no longer adequate to wait until the customer walks into a branch or decides to purchase a new product online or via a smartphone. Instead, banks and credit unions must engage customers at every stage of their purchase journey – not just because of the immediate opportunities to convert interest to sales, but because two-thirds of the decisions customers make are informed by the quality of their experiences all along their journey.

3. Making Data Analytics Actionable. Capturing and using consumer insight will be an important differentiator for organizations hoping to build new relationships and solidify those relationships already in place. Consumers will expect their financial institution partners to be able to provide real-time recommendations based on changes in their financial profile.

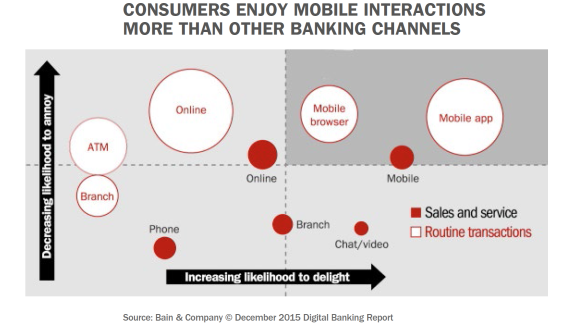

4. Introduction of ‘Optichannel’ Delivery. Today’s consumers demand financial services to be available and delivered to them as seamlessly and ubiquitously as any transaction they complete with Amazon. And it’s not just about improving customer service … it’s about satisfying today’s hyper-connected consumer by delivering both service and sales through any channel the consumer chooses to use. The financial institution that fails to deliver sales, as well as service, through the platform of their consumers’ choice is doomed to stagnant growth.

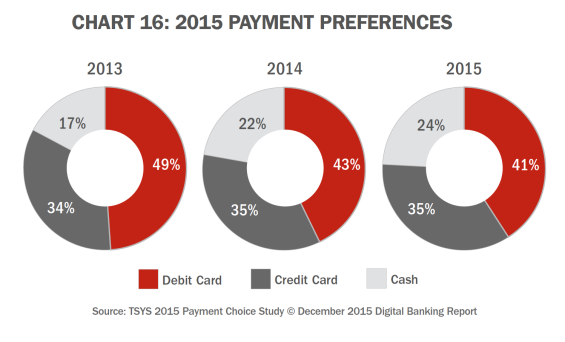

5. Expansion of Digital Payments. While it’s impossible to ignore the hype around mobile payments within the banking industry, consumers are seemingly unfazed by ability to make payments with their smartphones, according to an Accenture survey of 4,000 smartphone users in the United States and Canada. Even after the release of Apple Pay in the United States in October 2014, mobile payments have failed to catch fire. For the second year in a row, the majority of our crowdsourced panel believes that digital payments will ‘take off’ in 2016.

6. Executing on Innovation. Although innovation is a proven path to differentiation and competitiveness, the banking industry’s short-term focus, siloed approach to operations and risk-averse culture work against the potential for meaningful advancements. Banking will begin to replicate the best of fintech start-ups while leveraging their customer base scale advantage to respond to a changing marketplace.

6. Executing on Innovation. Although innovation is a proven path to differentiation and competitiveness, the banking industry’s short-term focus, siloed approach to operations and risk-averse culture work against the potential for meaningful advancements. Banking will begin to replicate the best of fintech start-ups while leveraging their customer base scale advantage to respond to a changing marketplace.

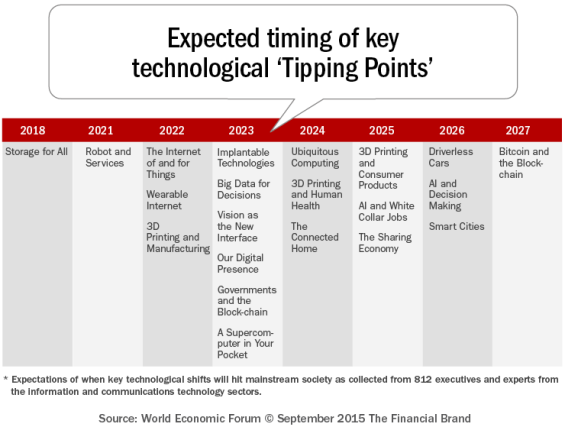

7. Exploring Advanced Technologies. Blockchain technology, robots, artificial intelligence (AI), biometric authentication and the Internet of Things (IoT) were all mentioned by our crowdsourced panel this year. While there will be a great deal of debate as to the likelihood of any of these trends gaining traction in the next 12 months, most panelists believe the debate can only be around timing.

8. Emergence of a New Breed of Banks. Competing with legacy banks that have the advantage of assets, large customer bases, established systems and technology and experience is not an easy task for a fintech start-up. On the other hand, similar to a pick-up truck vs. a semi trailer in a tight turn, size also has its disadvantages. Old core infrastructures that were built before the ATM were not built with digital technology or mobility in mind. As a result, it is more difficult to respond to the significant number of specialized fintech providers that are competing in service areas such as payments, mobile transactions and even advisory services. Our panel expects to see a number of new ‘challenger banks’ appear in the US, UK and other locations globally.

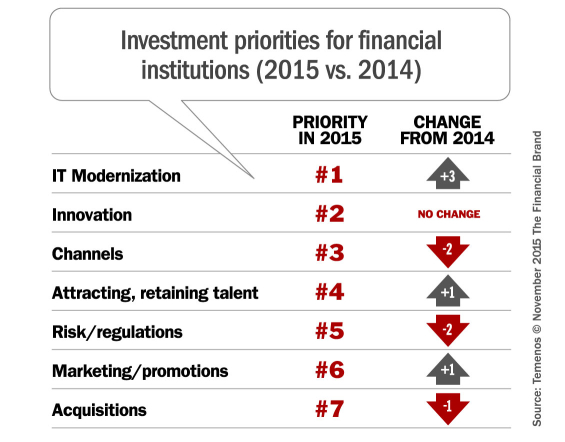

9. Mining New Talent. A significant change in the industry’s priorities is expected in 2016, from a focus on responding to regulations and compliance to a greater emphasis on building a ‘digital bank’. This shift in emphasis manifests itself in the fact that updated technology is banking’s biggest priority this year (up from number 4 last year) and that, for the third consecutive year, the industry’s biggest challenge was satisfying the demands of better-informed and less-loyal consumers. Underlying all of these priorities is the need to hire technologically savvy talent.

10. Responding to Regulatory Changes. In an effort to be more proactive, banks will begin to embed compliance throughout the organization, ensuring the most efficiency and effective use of resources. This will involve both cultural change and a streamlining and simplification of processes. For many organizations, the centralization of the compliance process has worked well, especially in regards to know your customer and anti-money laundering efforts. Advanced use of data for identification and surveillance of abnormal behavior helps detect for instance.

The Road Ahead

More than ever before, all of the banking industry’s constituencies are being impacted by the transformation of the banking industry. The category that has the most to gain from the changes expected in 2016 will be the consumer. They are not only in the driver’s seat with regards to being able to voice their digital banking expectations, but there are more firms than ever trying to meet those expectations.

As banking organizations further digitize their offerings, the consumer will benefit. In 2016, we will see end-to-end digital account opening

and onboarding solutions, contextual offers, better pricing that reflects the economies from digital transformation, and a greater array of offerings coming from the partnership of fintech and legacy banking organizations.

We expect to see this wave of enhanced consumerism continue for the next several years. As margins get squeezed, competition intensifies and the government opens the door for a free market banking system, the banking industry will be in a constant state of flux.

Digital Banking Report Ordering Information

The 82-page 2016 Digital Banking Trends & Predictions, sponsored by Kony, Inc. is available as a single issue or as part of a subscription to the Digital Banking Report.

The 82-page 2016 Digital Banking Trends & Predictions, sponsored by Kony, Inc. is available as a single issue or as part of a subscription to the Digital Banking Report.