It is amazing how some topics continue to stay relevant in banking despite the passage of time. One such topic is the importance of customer analytics in banking. In 2013, I referenced a report from Celent entitled, Customer Analytics in Banking: Why Here, Why Now?, where senior analyst, Bob Meara wrote that it was the time for banks and credit unions to leverage the advances in processing, memory, database design and analytic methods to improve performance and reduce costs.

While the Celent analyst noted that some institutions are already on the path of using advanced analytics for decisioning and optimization, other organizations had only limited experience. I am republishing the article that did not get transferred from my previous blog since the topic (and the examples) are as true today as they were when the Celent report (and my blog post) were first published.

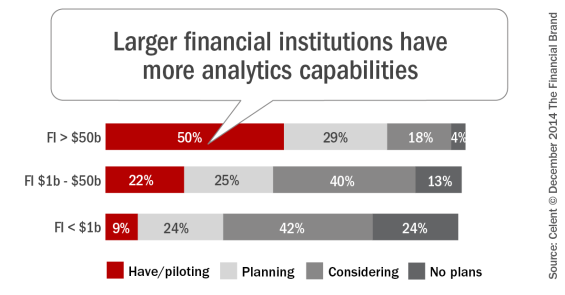

In the report, it is noted that financial marketers need to extract more value from internal and external data sources, guiding product development, customer communication, innovation and growth. According to Celent, the use of advanced analytics in banking is correlated to the size of organization even though the cost of processing data is no longer as much of a barrier as even five years ago.

The following are the primary reasons why banks need to step up their customer analytics game:

- The New Normal: The banking industry is expected to remain revenue challenged for the foreseeable future as a result of low interest rates, moderate fee revenue, onerous regulation and a less than robust economy. As a result, it will be more important than ever for banks and credit unions to focus on all possible strategies to reduce costs and increase revenues. Some of these strategies, enabled by customer analytics include:

- Improved targeting of customer segments

- Moving from a product focus to a customer focus

- Better management (and measurement) of sales leads across channels

- Inclusion of custom customer incentives/rewards to influence behavior

- The Imperative for Customer Centricity: With customer delivery and communication channels expanding, and more customers interacting with their financial provider using online and mobile channels, always-on, real-time sales and service become imperative. Analytics can respond to the migration to digital channels by:

- Improving branch efficiency and effectiveness

- Integrating sales and service tools within a new digital environment

- Helping to drive high value, high touch traffic back to branches

- Technology Advancement: Customer analytic applications are no longer the sole domain of highly skilled specialists. Today’s solutions can be accessed and used by marketers and other business users to answer complex inquiries. Improvements include:

- Collapsing of product silos and ability to process increased data sources

- Increased number of specialized vendor solutions and expanded talent

- Cloud-based solutions

Customer Analytic Applications

As the Celent study makes clear, there is no shortage of analytic applications for banks and credit unions. While some are more general in nature, some are highly specific outsourced solutions, supporting a buy vs. build decision. Obviously, with a focus on containing costs, the ability to utilize outsourced solutions is good news.

“Key retail banking priorities – specifically, using self-service channels to drive branch foot traffic, improving branch channel efficiency and effectiveness, and learning how to sell and service through digital channels – all require customer analytics,” says Meara from Celent. “The good news is that there has never been such a variety of specialized customer analytics solutions.”

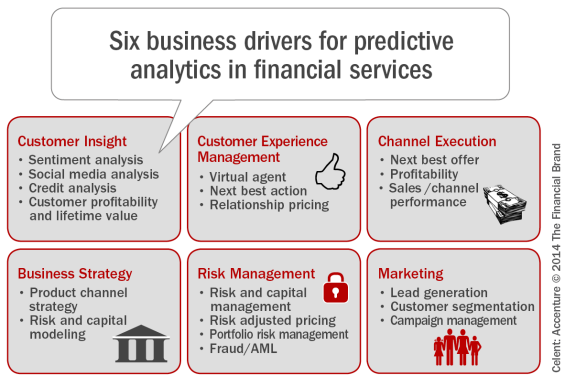

According to the Celent report, there are six key well-established business drivers for predictive analytics in financial services. Each of these are important as a bank or credit union builds an analytic strategy for the future.

Customer Insight

Of special interest to most financial marketers is the ability to gain a better insight on current customers. While demographics and current product ownership are at the foundation of customer insight, behavioral and attitudinal insights are gaining in importance as channel selection and product use become more differentiated. Sentiment analysis and social media analysis are two additional examples.

Another predictive analytic model is the FICO score. Scoring models such as FICO analyze consumers’ credit history, loan or credit applications, and other data to assess whether the consumer will make their payments on time in the future.

Business Strategy

The foundation of traditional banking business intelligence (BI), customer analytics are often used for product and channel development as well as economic forecasting, business improvements, risk analysis, and financial modeling.

Customer Experience Management

According to the Celent study, the key to using customer analytics for customer experience management (CEM) is about delivering personalized, contextual interactions that will assist customers with their daily financial needs. In addition, if done correctly, customer analytics in the context of CEM enables the real-time delivery of product or service offerings at the right time. It can also allow for highly sophisticated relationship pricing never before available.

Risk Management

One of the more common uses of ‘big data’ today is in the area of risk and fraud management. Data mining today has expanded well beyond internal purchase and balance insights to include transaction patterns and even social media interactions that can provide a leading indicator to potential losses or fraud.

This type of integration of structured and unstructured data can also be leveraged for traditional risk management uses such as for pricing decisions.

Channel Execution

BI tools have helped banks understand channel effectiveness for some time. More recently, analytics capabilities have boosted the usefulness of these tools. Capabilities include providing comprehensive views of channel performance based on both customer behavior and transaction mix. Solutions help banks understand channel profitability and customer satisfaction and tailor retail operating models to improve retail delivery.

As more banks and credit unions work harder at migrating customers to digital channels, analysis of engagement and shifts in channel use become important indicators of satisfaction and re-pricing opportunities.

Marketing

Another traditional use of customer analytics is the ability to increase the effectiveness and efficiency of sales and marketing in financial services. The ability to derive the likelihood of purchase based on available information about individual customers has ushered in a seismic shift in marketing from product centricity to customer centricity.

Rather than offering products and services based on what the financial institution would like to sell (campaigns), banks and credit unions are now able to make unique, timely, and relevant offers based on available customer insight. Doing this form of analysis across multiple channels allows financial marketers to significantly improve the efficiency of marketing spending and the close rate of sales leads.

For each of the applications shown above, the power is not just in the analytics themselves, but in the ability to do so in real time. With more challenges than ever in banking, analytics is at the center of it all.

Implementing a Successful Data Analytics Process

The Celent research emphasizes that while there are a growing array of use cases for data analytics, the process is definitely not a ‘one and done’ proposition. The move from a product/campaign based approach to a customer centric approach is huge and involves many moving parts.

Successful implementations always involve a series of steps and a test and learn process as shown below, with a different amount of time and effort applied to each step based on the specific objectives of the project being undertaken.

According to Bob Meara from Celent, “Most organizations (banks included) get good at specific analytics use cases and broaden their use once parts of the organization gain confidence and prove the business case. Only then is the approach used more broadly and extensively.” He recommended that financial institutions:

- Start small. Invest a little and wear out the application. See what it can do.

- Experiment – early and often. This requires a willingness to fail (in small and low-risk ways).

- Embrace analytics as a journey, not a destination. Keep learning and keep looking for ways to apply analytics for fun and profit.

In response to a question from me around whether banks should ‘boil an ocean’ in their analytics endeavors, Meara stated, “Of course, banks should walk before they run. By that, I mean banks should fully leverage in-house transactional data before investing heavily in external sources of information and insight.”

He added, “Social data is particularly compelling, but runs a big risk of being unrepresentative. SAS, for example, does a great job integrating social media data with internal data to arrive at more well informed models and more highly predictive outcomes. Either way, start with the treasure trove of data already available.”

The reality is that, in the digital banking model of the future, data is a financial institution’s most important asset. Banks and credit unions that are able to combine their internal and external data sources to create value will find themselves well placed to thrive in what some have called ‘Banking 3.0’. There is no question that this banking reality is as true today as it was years ago. The difference is that today’s technology is making the task a bit easier.