According to the 60-page Digital Banking Report ‘Strategic Planning Imperative: Capitalizing on Digital’s Promise’, a new competitive environment is emerging where technology-driven providers are entering the retail banking sector, offering simplified, algorithm-based financial services. The offerings of these new players cover the entire gamut of services offered by banks and credit unions, including deposit taking, lending, payments, personal money management, investment and advisory services.

Despite the growth of the ‘digital society’ in all aspects of consumer’s lives, the impact of the digitization of financial services has often been underestimated. More than simply eating around at the edges of product offerings of retail banking, non-bank competitors are capturing revenues, value-added engagement and at times, the loyalty of the digital consumer.

Despite the growth of the ‘digital society’ in all aspects of consumer’s lives, the impact of the digitization of financial services has often been underestimated. More than simply eating around at the edges of product offerings of retail banking, non-bank competitors are capturing revenues, value-added engagement and at times, the loyalty of the digital consumer.

It is time for traditional banks to place a high priority on the development of a digitization strategy, leveraging the benefits of brand recognition, a strong multichannel distribution network, unequalled customer insights, operational security, trust, and the infrastructure to provide a human touch. Beyond a cost saving strategy, becoming a ‘Digital Bank’ is becoming a matter of survival.

The forces driving the digital structural change in banking mirrors the forces seen in other industries, such as music, media, publishing, and a host of others. The high penetration and rapid acceptance of internet-based services and mobile devices such as smartphones, tablets and e-readers has set the foundation for rapid innovation and compartmentalized digital financial services offerings.

The emergence of the digital consumer gives rise to new opportunities for traditional financial organizations as well as new market entrants. This will give rise to competitive pressure on established players to continually innovate, simplify delivery, find ways to monetize digital offerings, potentially expand offerings outside the financial sector and become an integral part of consumers’ daily financial lives.

This transformation has also resulted in the development of innovation labs and uncommon affiliations and partnerships with technology providers outside the financial services industry. These partners usually have the agility, design capabilities and start-up mentality that traditional financial institutions lack. Examples of these collaborations include Simple/BBVA, Capital One/Adaptive Path and TD Bank/Moven.

Banking’s Move to Digital

The digital consumer does not distinguish between online and offline distribution channels. While many consumers still like walking into a physical bricks and mortar facility, a greater percentage of consumers prefer to use their desktop computer, mobile phone or tablet to transact business with their bank. For these consumers, ‘traditional banking hours’ are not only an annoyance, but increasingly a reason to change financial institutions.

“For digital consumers, ‘traditional banking hours’ are not only an annoyance, but increasingly a reason to change financial institutions.”

— Deutsche Bank Research

The digital consumer wants a bank or credit union that is available on demand. These consumers want to use sophisticated banking apps that have a clean design and are simple to use. They want real-time insight into their financial portfolio that will not only tell them what has occurred in the past, but how they should handle their money in the future. They demand contextual SMS alerts and notifications that illustrate that their financial institution is looking out for them 24/7.

The changes in the consumer present challenges that have spawned competition from technology-driven non-bank firms, who are offering easily standardizable financial products and services to gain customers and market share. These challenges also provide opportunities for organizations that understand the basics of being a more digital bank, and begin to transform their development and delivery of services accordingly.

Most banks and credit unions are playing catch-up. The digital revolution has caught most organizations flat footed and unprepared for the increasing demands of the digital consumer. The reality that most organizations have core processing systems that were installed decades before the Internet and are not structured for either online or mobile banking deliverables only makes the situation more difficult.

Becoming a Digital Bank

Becoming a ‘Digital Bank’ is about leveraging digital technology to provide an enhanced customer experience that fits the lifestyle of the increasingly digital consumer. It should ultimately combine the benefits of the digital and physical worlds.

When engaging with a digital bank, consumers should benefit from the following:

- Shop for a financial institution online or with a mobile device

- Open a new account by using a computer, tablet or mobile device using image capture to save steps

- Communication with their bank through the channel of choice, potentially with live video tools

- Financial insights pre-login, such as balances, recent transactions and product recommendations

- Real-time and secure transactions online or at the point of sale with a mobile device

- Personalized and predictive offers that leverage geographic as well as contextualized insight

- Real-time digital money management including alerts and notifications

- Integration of financial services with daily activities

Digitization is not simply a defensive strategy against bank and non-bank competitors. It should also be a way to increase revenue through improved consumer insights, combining algorithm-based banking with the human touch.

Digitization is not simply a defensive strategy against bank and non-bank competitors. It should also be a way to increase revenue through improved consumer insights, combining algorithm-based banking with the human touch.”

But making the above possible requires leaner operating models, streamlined decision making, the leveraging of both structured and non-structured consumer insights and a breakdown of silos to enable faster processing. None of these requirements are the strong suit of traditional banking organizations.

This is why many banking organizations have formed strategic alliances with technology-driven players. This simplifies the market entry of innovative start-ups while being able to leverage existing banking infrastructure. In many cases, the technology is at the forefront (mobile account opening tools, payment apps, etc.). The question becomes … is too much control of the customer experience being relegated to others (i.e. Apple Pay).

The 60-page Digital Banking Report ‘Strategic Planning Imperative: Capitalizing on Digital’s Promise,’ outlines how financial institutions can build the foundation for a Digital Bank. The ‘fundamentals’ covered in the report include:

- Mobile Account Opening (MAO), including image capture

- Digital alerts and SMS notifications

- Mobile payments

- Simplicity in digital design

- Selling on mobile

- Security and authentication

- Digital money management

- Digital customer service

- Online document storage and digital lockbox

- New gen video supported ATMs

- Contextual analytics

- Geolocational offers.

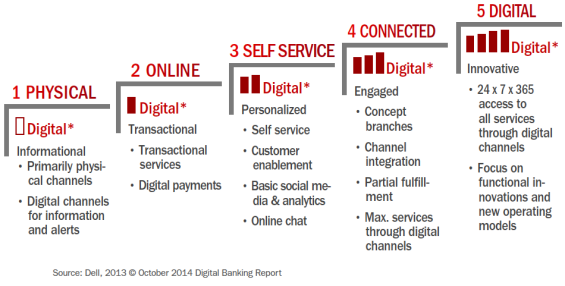

Digital Maturity Model

It’s time for some introspection within the financial services industry. One of the first steps to determining your strategic priorities for digital banking is to assess the digital readiness of your organization.

Dell has developed a comprehensive Digital Maturity Model (DMM) to map a financial institution’s current digital state allowing an organization to develop a comprehensive action plan that is completely aligned to overall strategic goals. Keeping pace with the changing banking environment and evolving technology can be a challenge — especially when technology innovations in mobility, analytics, social media and the cloud continue at a rapid pace. Add the emergence of digital services from non-traditional banking players such as peer-to-peer (P2P) payments, digital financial management (PFM), remote deposit capture and digital wallets and the challenge is even greater.

Success will depend on constantly engaging stakeholders, leveraging new technology and potential partnerships to enable consumers and extend existing business models to build differentiated products and services. The chart below provides an illustration of some of the steps involved.

Implications for Traditional Banking Organizations

When asked what his definition of a digital bank was, Chris Skinner, Chairman of the Financial Services Club and author of the book, , said, “A digital bank is a bank built with a vision to reach out to customers through digital augmentation. It is built specifically to offer the customer the service of their choice through the access of their choice.”

He also believes a digital bank believes wholeheartedly that, in order to do this the bank has to be designed and created upon a digital core infrastructure with an organization geared to digital. Finally, the organization must be committed to having an innate knowledge of their customer and using that knowledge for the customer’s benefit.

As Chris said, “A digital bank is more like an Amazon processor of finance rather than a Barnes & Noble bookstore.”

The future of the financial services industry will depend on its ability to leverage the power of customer insight and digital technology to provide services that help today’s tech-savvy customers save and better manage their everyday lives. If banks and credit unions don’t move quickly, competitors will insert themselves into the buying process, gaining the valuable purchase insight that is the domain of the banking industry today.