Over the past 24+ months, Apple has opted to remain on the sideline instead of offering an integrated mobile payments solution. During this period, Apple introduced components of a potential payment solution, including the Passbook application for storing coupons, tickets and loyalty cards, the Touch ID fingerprint scanner with an API paving the way for more secure applications, and the iBeacon for location-based information and offers.

Like they did with music labels for iTunes and cellular carriers with the iPhone, Apple reached out to many of the biggest partners ahead of introducing Apple Pay – the major card carriers (American Express, MasterCard and Visa), the six biggest issuing banks representing 83 percent of credit card volume in the U.S., and major retailers like Macy’s, Bloomingdales, McDonald’s, Walgreens, Nike, Staples and Disney (with 220,000 stores).

Instead of payments disruption, Apple’s initial foray into payments appears to be focused on improving the experience between the consumer and the merchant … removing friction and improving the security of each transaction. In other words, instead of replacing the incumbent payments network, Apple decided to leverage what was already in place, building partnerships with key players.

“Any calls for Apple to disrupt banking or payments has proven to be premature, considering that Apple prefers status quo more than it’s fans,” said Cherian Abraham, mobile commerce and payments lead at Experian.

Evolution Not Revolution

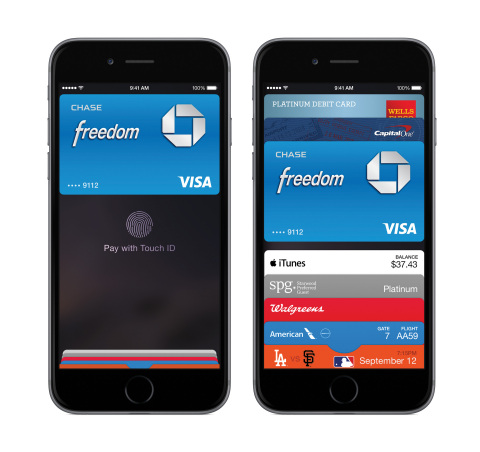

Using near-field communications technology, Apple Pay will enable consumers to make payments at participating outlets with a swipe of an iPhone 6, iPhone 6 Plus or an Apple Watch. Apple Pay uses the Passbook app, the Touch ID, NFC, and a secure element to process payments.

Apple Pay will also support online purchases with a one-touch checkout. This process will eliminate common online shopping hassles, like entering credit card information and typing out a billing address. Private information will be secure since it will not be shared with the merchant. A bunch of merchants are already on board with Apple Pay online, including Uber, Disney, Sephora, Starbuck, Groupon, Target, Staples, Tickets.com, Panera Bread, and more.

NFC at the point of sale will be categorized as card-present transactions for interchange fee purposes, and in-app purchases will be considered card-not-present transactions with fees aligned with more secure forms of card-not-present.

NFC payments are far from being new. In fact, they have been part of the Android ecosystem for years. The concept of a mobile wallet that stores payment credentials is also not new, with PayPal, Venmo, and even the on again, off again Google Wallet paving the way. Yet, Apple always makes what others have done before them more exciting. Despite not being first with either a payments app or mobile wallet, Tim Cook unabashedly ended the Apple Pay segment of his presentation with a prediction: “ApplePay will forever change the way all of us buy things.”

“The tech giant [follows] a familiar pattern: let the first movers flail with the earliest versions of some product or service, then release a more polished version of the same idea. The mobile wallet in 2014 is a lot like the MP3 player in early 2001, just before the launch of the iPod, or the smartphones available in 2006 ahead of the first iPhone. The tools now exist for fully functional mobile wallets, just not in a way that has won over the shopping masses.” – Bloomberg

Focus on Security

The debut of the plastic replacement Apple Pay solution comes as another wave of ‘bad news’ over digital security is part of the daily news cycle, with another major retailer data breach being announced and an iCloud hack that exposed nude images of celebrities.

To address security concerns, Apple is storing cards securely by encrypting the information and storing multiple credit cards in Passbook. Each card gets a device-only account number, so the actual card number is never stored or shared. As a result, a cashier never sees an account number or name. Apple Pay also replaces the three-digit code on the back of credit cards with a dynamic security code.

Apple Pay can either use the card currently stored on an iTunes account, or the consumer can add a card by taking a photo of another card and easily add it to Passbook. Apple Pay will leverage TouchID/fingerprint technology to authorize transactions, with the company emphasizing the relative speed/convenience of this one-touch payment method.

“We’re totally reliant on the exposed numbers, and the outdated and vulnerable magnetic interface — which by the way is five decades old — and the security codes which all of us know aren’t secure.” – Tim Cook, Apple CEO

Rumors leading up to today’s announcement suggested that the company had used its enhanced security and anti-fraud features to negotiate unprecedented discounts on the already low “card present” rates applied to traditional in-person credit card transactions. If true, that could eventually impact the balance of power a bit between merchants, banks and Apple.

Regarding security, Tim Cook told USA Today, “This is something that the merchants believe in, and the banks, because they love fraud plummeting. There’s that moment when a consumer’s card gets rejected for fraud (by a merchant) and they can’t pay for what they’re buying. When you combine all that, it’s like striking a match. It’s going to spread and spread fast.”

Finally, Apple will not collect consumer transaction data as once anticipated. This reduces the threat to the current ecosystem and to financial institutions in general.

The Power of Apple

Apple has over 800 million registered iTunes accounts, some portion of which will upgrade to the iPhone 6 devices. Though that shift may not happen overnight, eventually users will upgrade as their contracts expire and Apple continues to release new features that draw users in.

That, in fact, is Apple’s biggest advantage in entering the mobile payments market where competitors like PayPal, Google and the mobile carriers themselves already offer their own mobile payment solutions, some of which also involve NFC technology.

The power of Apple also will be seen almost immediately with the relationships struck with card companies, financial institutions and retailers. Beginning in October, Citi and several other of the largest financial institutions will provide cardmembers the option to pay with their eligible credit or debit card using their iPhone 6 and iPhone 6 Plus. Whether they are buying in stores or online from merchants in apps, organizations will promote their partnership with Apple by stressing the simplicity and security of using Apple Pay.

Announcements similar to the one below from Citi will become commonplace.

“Citi has a long history of delivering choice and value through innovation that meets our cardmembers’ needs. We are looking forward to delivering to our cardmembers another way to simply and quickly make payments for a broad range of purchases such as buying a coffee, groceries or purchasing digital music.” – Barry Rodrigues, Head of Enterprise Payments at Citi

Impact on Payments Players and Use

NFC wallets have struggled for adoption, and one reason was because merchants didn’t have point of sale terminals equipped with the capability (and some merchants turned off the NFC functionality). But as merchants upgrade their terminals for the October 2015 deadline for EMV-chip card acceptance in the U.S., those new terminals will likely have NFC functionality.

“Overall, it’s still going to be the breakthrough experience tied to phone and watch that we’ve been waiting for … this will be huge and the naysayers will be proven wrong.” – Bradley Leimer, Mechanic Bank

Apple Pay should definitely accelerate the timeline for mobile payment acceptance in the US. While only about 20% of merchants accept NFC (tap & go) today, Apple’s move should tip the industry to upgrade point-of-sale terminals.Products such as eBay’s ‘One Touch PayPal’ could also have a positive impact.

Analysts believe that Apple Pay will have a positive impact on the card networks and certainly the terminal manufacturers with a possible negative impact on issuers and acquirers. And while Apple’s sizable smartphone market share, loyal users and iTunes card accounts could no doubt make it a significant player in the mobile wallet marketplace, it is believed that it may actually increase the opportunity for PayPal (and other payment players) in the near term.

Notably absent among the list of launch partners are the world’s largest retailers like Wal-Mart, Safeway, Target and CVS as well as thousands of convenience stores that have fought heavily against recent attempts to regulate interchange fees under the Durbin Amendment. The Merchant Customer Exchange (MCX) comprising as many as 110,000 locations and has just introduced their CurrentC mobile wallet.

If Apple wants ApplePay to become truly ubiquitous, both in-person and within mobile apps, it will eventually need to convince these holdouts that it adds more value than it takes away (through any fees).

Denée Carrington, Senior Analyst at Forrester Research said, “Apple Pay will ignite consumers’ interest in mobile payments by providing a seamless, secure, and easy way to pay both in store and on the go. By partnering with the leading merchants across retail, grocery, drugstore, and dining, consumers can use Apple Pay with merchants they shop every day — which will accelerate the growth of mobile payments in the US.”

Finally, many believe Apple’s new payments service may eventually challenge carrier-backed ISIS — soon to be renamed to “Softcard” — Coin, and even Square.

A Potential Trojan Horse?

While the introduction of Apple Pay eliminated much of the ‘doom and gloom’ discussion within the banking community, the industry may not be in the clear just yet. This is because there were several notable missing components to the initial announcements by Apple that could have a significant impact on consumer relationships with their financial institution.

In the wave of announcements, there was no mention of increased NFC functionality for the future versions of the iPad. Without NFC capabilities, plugging in a Square payments dongle won’t allow merchants to support ApplePay. While this may be on the drawing boards, Apple could take an alternative partnering position with smaller merchants.

Before the introduction of Apple Pay, there was significant discussion around the integration of Apple’s iBeacon solution (based on Bluetooth Low- Emmission, or BLE technology) to deliver targeted, actionable offers to consumers. Building a rewards network directly with merchants using this technology could significantly alter the balance of power with consumers as product/behavioral insight could still be collected without connecting the data to specific payment information. Much like a closed ad network, this capability could be the Holy Grail of payments revenue.

Finally, a more subtle, yet potentially game changing observation mentioned by Karen Webster, CEO of Market Platform Dynamics, is how Apple chose to name its payments capability Apple Pay as opposed to iPay or iWallet. “Apple wants the consumer association with Apple first and foremost. Sure, card brands and network brands are visible, but Apple Pay will make every other brand subordinate to it because that is how the consumer and the merchant will view it,” said Webster.

“That means that the power, at least in the iOS ecosystem, is likely to accrue over time to Apple. And with 800 million registered accounts, well, it might not need that much time,” continued Webster.

And what does that power mean when you look at person to person payments (P2P) that also was left out of the presentation by Apple?

A Future View

Apple will begin rolling out Pay within a month, and it will be accompanied by an iOS 8 update. American Express, Bank of America, Capital One Bank, Chase, Citi and Wells Fargo will be the first banks to offer Apple Pay with additional banks coming quickly thereafter including Barclaycard, Navy Federal Credit Union, PNC Bank, USAA and U.S. Bank.

Large and otherwise impressive companies like PayPal, Google, Amazon, Square, and Stripe, have all tried to tackle this problem before with limited success. But as is the case in most categories it enters, Apple has a way of delivering ‘mass’. This is why bank and credit union executives should expect ApplePay to be accepted and move the needle rather quickly.

“While it’s too early to know the business model implications (as Apple has been very secret about the back end agreements, though issuers and networks seem to be on the winning side), the industry will finally see whether what it has bet on is true: that only Apple can change user behaviors significantly,” says Yann Ranchere, director at Anthemis and finance 2.0 blogger.