Visit any bank or credit union conference and it sounds like big data might be the cure-all for all business challenges. Ineffective customer insight? … Big data! Poor marketing performance? … Big data! Inefficient distribution or back office operations? … Big data! While big data holds incredible potential across a range of disciplines, harnessing this potential remains elusive for most financial institutions.

Even defining the term is difficult. Big data is most commonly defined as data sets that meet three attributes, known as the three “Vs” – volume, variety, and velocity. It’s data that is generated quickly, comes in all shapes and sizes, and in great quantities. But while the definition of big data may be somewhat vague, the value of this data is well documented.

For years, financial institutions have collected information on their customers and members – basic demographics, transactions, account activity, loan portfolios and credit card balances that are the backbone of decisions. Much of this data is converted into monthly, quarterly and annual reports for use by their internal and external parties.

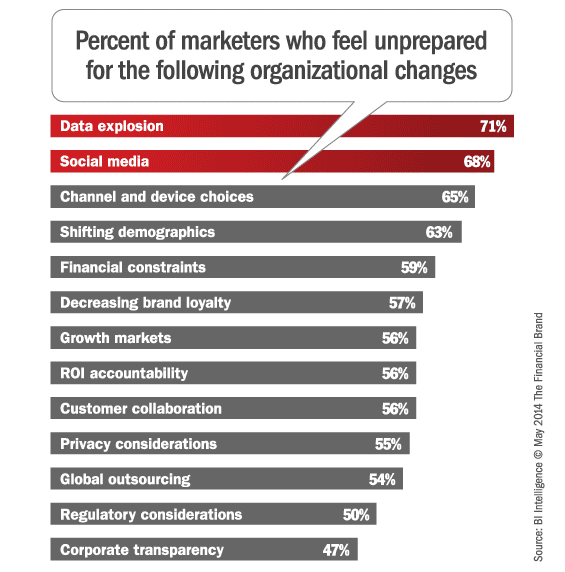

With all of this insight, banks have done a pretty good job of looking back in time and leveraging historical data. Looking forward has been more of a challenge. In fact, despite the importance of leveraging data for improved results, seventy-one percent of chief marketing officers around the globe say their organization is unprepared to deal with the explosion of big data over the next few years, according to an IBM survey. They cited it as their top challenge, ahead of channel fragmentation, shifting demographics and regulatory or privacy considerations.

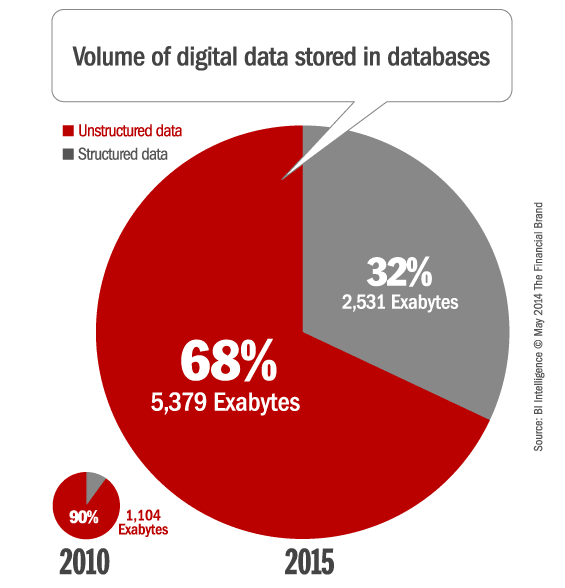

The growth in data is both structured and unstructured. Structured data refers to the data that currently resides in product and customer-servicing systems. Unstructured data refers to insight that is not as easily captured or stored, such as social media insight, voice call logs, emails, website click streams, and even video files. According to Business Insider, up to 70 percent of the world’s data is unstructured.

As one banker mentioned, big data offers more than a snapshot of what some representative cohort of people are doing, it offers the chance to mine millions or even billions of direct observations on what everyone is doing … in real time.

Big data capabilities provide bank and credit union marketers the ability to understand their customer and members at a more granular level and more quickly deliver targeted personalized offers. This results in better offer and cross-sell response rates, improved product penetration, increased satisfaction and advocacy, improved customer profitability and potentially lower campaign costs.

The challenge is departments within banks have operated in silos, meaning that many institutions have no clear, single view of their customers. Thus, careful analysis – by individual or household – of account usage tendencies, receptivity to marketing programs, customer service preferences or demographic patterns is nearly impossible. However, there is a lot of focus on getting this enterprise view of the customer fixed.

A 2012 survey conducted by Deloitte of executives in the United States and other countries found that 96 percent of respondents (many of them bankers) believe the use of analytics will increase in importance over the next three years. Although the use of analytics as a marketing tool lags behind other disciplines, 55 percent of respondents said their organization’s marketing and sales groups are investing in analytics today – a number that’s expected to rise.

Banks need to transform their approach to data and analytics from traditional, product-focused marketing programs to a 360-degree customer-focused approach. They should strive to break down longstanding silos, operating horizontally across the enterprise, rather than narrowly, viewing one business unit at a time. This is often difficult because infrastructures were designed to work vertically.

The Power of Automation

The ability to perform complex statistical analysis – automated and in real-time – can provide personalized offers at the moment the customer is ready for it. Without an automated analytics platform, the consumer could miss your offer or receive an offer from a competitor … in a digital second with a click of a mouse or mobile tap.

As one executive from a global bank remarked in Deloitte’s Analytics Advantage survey, “I would rather have a little bit of the right information at the ‘moment of truth’ than all the information in the world two weeks later.”

Automated data analytics can help financial institutions implement multichannel customer journeys. These omnichannel encounters, leveraging customer transaction data, can enable organizations to provide channel agnostic communication at the right time, with the right offer using the channel the consumer prefers. This will lead to greater sales, improved customer satisfaction and even organizational efficiencies.

According to Deloitte, automated decision making and other analytics-driven competencies have a track record of generating higher revenues in a faster time frame and at a lower cost. In fact, successful trials with impactful ROI can swiftly build out an organization’s analytics budget.

To find these skillsets in any one person is unlikely, requiring a team approach. When data and decision scientists are combined with bankers who know and understand the banking business and with traditional technologists who understand the business data, a powerful, problem-solving team is formed.

But the benefits from big data can be significant and widespread.

The analytics maturity or preparedness for using analytics varies vastly in banks. Size and deep pockets have not necessarily translated into competitive advantage. Organizations that have sound data infrastructure and a clear 360o view of their customers definitely have a head start and will maintain their tremendous advantage and will end up being the winners.

These institutions will benefit by deploying latest technologies and analytical platforms and guide business decisions as never before. They will emerge leaders of the pack. Many may need external help to carve a broader picture and pick the best practices or solution set that will be most appropriate for their organization.

In reality, both large and small financial institutions need to become data-driven companies that will have the capability to capture, crunch and analyze data to find hidden, but increasingly valuable insights that will make an institution more competitive, efficient and attractive to consumers. According to IBM, successfully harnessing big data can help organizations achieve three critical objectives for banking transformation: Create a customer-focused enterprise; Optimize enterprise risk management; and Increase flexibility and streamline operations.

“The key element in success for any project involving Big Data is accepting and embracing decision making with less-than-ideal information. Complementing bank decision-makers’ expertise with that of experienced data and decision scientists, though, is a proven strategy to overcoming the “analysis-paralysis” that delays and side tracks many Big Data projects,” states Seth Rosensweig, managing director in the Information Management Services group at global consulting firm AlixPartners LLP.