The day is nearer than anyone thought when children wonder aloud what on earth their forebears did with those folded, leather things — “What’s a checkbook? What did you use wallets for?”

A consumer trends survey fielded by Fiserv designed to determine awareness, familiarity, and use of various payment methods shows that mobile banking adoption and demand for a wider breadth of mobile services are accelerating. But it also shows that financial institutions have some serious work to do if they’re going to seize the opportunities these trends create.

The days of sitting at the kitchen table once a month to pay bills are gone. Consumers now pay bills on demand, wherever and whenever it suits them.

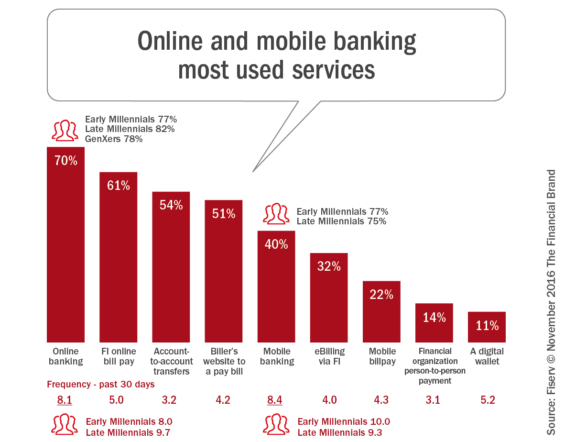

A full 70% of households reported having used online banking, and those who use online banking don’t use it just once but an average of eight times. 61% of households use financial institution online bill pay, making it the most popular online banking feature. Bill pay via a biller’s website follows closely behind, coming in at 51%. In fact, when the number of bills paid online at financial institutions and billers is combined, online bill pay now accounts for 58% of consumer bills paid.

Use of most online services rises as age descends. Among the 82% of late Millennials (ages 25-35) who say they used online banking in the past month, they accessed it an average of ten time — 12% more than households overall.

The temptation might be to assume that financial institutions need only make available a broad range of services in order to rest on their digital laurels. But, at best, offering an array of digital services is now no more than table stakes. Apps must be branded, intuitive, and easy-to-use. The report suggests even more needs to be done to satisfy the increasingly demanding digital consumer.

A growing number of consumers prefer carrying their bank around in their pocket as opposed to sitting at a desk and working from a monitor. 40% of consumers use mobile banking, including 87% of Millennials with an enabled device.

If less than half of consumers use mobile banking, more than half have yet to adopt — a significant opportunity to reduce costs and enhance revenues.

Mobile banking is more popular on smartphones than on tablets, with nearly nine in 10 households that use mobile banking saying they do so using a smartphone (87%). The most common financial activities for which mobile devices are used are to purchase goods and pay for them online, and to transfer money between accounts at the same financial organization. 47% of households that use mobile banking use it to pay for products and services online, while 45% transfer money between accounts within the same financial organization.

When it comes to adoption and growth, person-to-person payment (P2P) lags noticeably behind. Only 14% of households used P2P in the prior 30 days. Yet those who use the service like it. They like the convenience of not having to deal with cash or check. So what’s the holdup?

A clue lies in the fact that 41% of households didn’t even know if their bank offered P2P. It seems that if banks want more P2P adoption, a major first step is to do a better job of building P2P awareness. This points to an opportunity for, among others, advertising managers and agencies.

What Millennials Want (And Why it Matters)

Millennials are defined as being between the ages of 18 and 35. As noted above, 87% of Millennials with an enabled device use mobile banking. Millennials already represent a substantial and growing market for the financial services industry, and it’s only a question of time before they supplant boomers and, later, Generation X as banking’s most sought-after consumers.

41% of Millennials would leave their wallet at home if they could store all of the information they need in a digital wallet they could access and use anywhere.

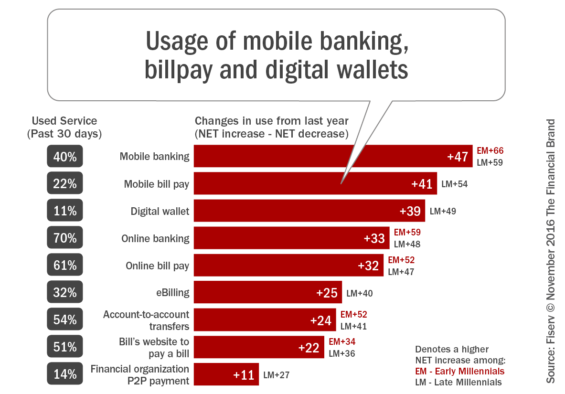

It shouldn’t be surprising that Millennials would be early adopters of new technology and services. Millennials and today’s technology pretty much grew up together. Even so, there may be some surprise in how fast Millennials are coming to rely on mobile banking services. 66% of early Millennials increased their use of mobile banking over the past 12 months, with late Millennials right on their heels at 59%. They also report increased use of mobile bill pay and account-to-account transfers.

The survey returned insufficient data to draw conclusions about the viability and future of wearables such as Apple Watch. This may be due more to the newness of the devices than to consumer preference. Some speculate that an intrinsic adoption inhibitor may reside in the smallness of the devices and the relative largeness of fingertips. In any case, wearables are worth watching.

The ‘I Want it Now’ Reality

Not long ago it was understood that banking transactions took time to clear. Accounts could be updated only as fast as information could be transmitted in person, by mail, or by telegraph. In an environment where ones and zeroes move at record speeds, consumers, in particular younger consumers who don’t remember the days of prolonged float, have little patience for delays.

They want their transactions and balance updates to happen in real time. The Fiserv report shows that 36% of bill pay users want same-day online bill payment posting and 25% want real-time account balances reflecting payments made.

Besides satisfying a craving for instant gratification, providing real-time updates can help bring more mobile users onboard. Of early Millennials, 40% said that the ability to have a person receive their payment in real-time would make them more likely to use person-to-person payment.

To be sure, moving to real-time data is not as simple as a snap of the fingers. But, consumers have the luxury of not understanding as much and, if they do understand, not caring. All they know is that their non-banking applications provide instant updates, and they want the same from their banking apps.

Making an Impression: Fingerprint IDs

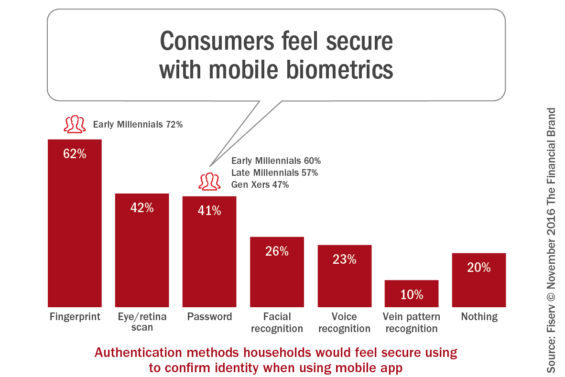

Security remains a barrier to mobile banking adoption for all age groups. 64% of consumers who don’t use mobile banking cited security as a main concern.

“Security concerns are major barriers to adoption of mobile banking (64%) Bill Pay (35%) P2P (29%).”

Nearly one-third of mobile banking users (29%) said their concerns about accessing mobile banking through their mobile device increased during the last year. Of those, 41% said they gave up mobile banking in favor of PC or laptop banking, which they perceive as more secure. 33% used cash or checks more often.

It doesn’t help matters that data breaches make for big headlines and have a long half-life in the public consciousness. The eBay, Sony, and The Home Depot breaches loom iconic in consumer minds even though they took place two years ago. The Target breach happened three years ago.

We need to expect security concerns to continue inhibiting adoption, and we need to find ways to allay them.

On the bright side, it appears that measures as simple as password use can help allay fears. 60% of early Millennials, 57% of late Millennials, 47% of Gen X-ers, and 61% of adults overall expressed confidence in passwords as a mobile application identity authentication method.

Even better, many expressed confidence in the use of biometrics for mobile security. Highest confidence is in fingerprint technology (62% overall with that number rising to 72% for early Millennials), followed by eye scan (42%), facial recognition (26%) and voice recognition (23%).

While the need to stay ahead of hackers in the security arms race with state-of-the-art measures goes without saying, here are two marketing recommendations:

1.) Remember that consumers cannot see your behind-the-scenes security measures. The only way they’ll know about them is if you tell them. Apps, your website, and printed collateral provide ideal opportunities to reassure. Given the link between security concerns and consumer satisfaction, this should be a priority.

2.) Educate consumers as to security measures they can implement on their own. This gives them a valid feeling of empowerment and of control over their own safety. In turn, it can help lift barriers to mobile banking adoption.

Low-Tech Solutions to High-Tech Avoidance

Security concerns aside, consumers have other reasons for dragging their feet when it comes to adoption of certain digital banking services. Not the least of those reasons is that people tend to be loath to change habits. 36% of non-users of online bill pay report that they are not currently paying bills using a financial organization’s bill pay service because they don’t mind paying bills by check, and 35% say that they just don’t want to change.

“People don’t use services because they don’t understand them: eBills (15%), Bill Pay (14%), Mobile Banking (20%) and P2P (24%).”

Lack of awareness also plays a significant role. Fiserv found that a number of people have yet to use certain mobile services simply because they don’t know they exist. Besides the above-referenced 41% of respondents who have no idea if their financial institution offers P2P, 45% didn’t know they can receive and review bills online. Leaving consumers unaware of a service doesn’t help promote adoption.

The survey also revealed that a significant number of people avoid new online services because they don’t know how to use them. This accounts for 15% who don’t use e-bills, 14% who don’t use bill pay, 20% who avoid mobile banking, and 24% who don’t use person-to-person payments.

Misconceptions also deter adoption. For instance, 41% don’t use online bill pay because they erroneously believe they’ll be locked into auto-payments. Correcting instances of misinformation could go a long way toward increased mobile adoption.

Finally, these are not technology challenges. They are marketing and communication challenges. Owned media such as apps, your website, and printed collateral can be useful conduits for making consumers aware of digital banking services, how to use them, and for allaying fears and correcting misinformation.

Good News… And More Good News

First, the good news – Increased adoption of digital banking services portends well for the industry. Mobile banking in particular is primed to become the new norm. Customer satisfaction runs high across digital banking services accessed on mobile devices, and is at its highest among older generations and households with an average annual income between $100,000 and $149,000.

Now for more good news – There is plenty of opportunity, with 30% of consumers not yet embracing online banking (saying they have used in the past 30 days). Of the 70% who use online banking, half have yet to embrace mobile banking. And of those, a significant number have only used it once or twice in the past 30 days (26%).

The environment for creating new online and mobile banking consumers, and broadening their use of services, is constantly improving. That’s due to three factors:

1. Improving technology.

2. Younger generations unafraid to try new things.

3. The “upward spiral effect” — as more people sign on and say they’re “very satisfied,” others will begin to feel reassured.

As things progress, even the most cautious may overcome their fears, and the most stubborn may give way in favor of hopping on the bandwagon.