Many bank executives subscribe to this law of banking, “it is easier to retain a customer than to acquire a new one.” It seems to make sense, but how do you retain a customer? Let’s begin by examining the causes of attrition and then look for ways to reduce it.

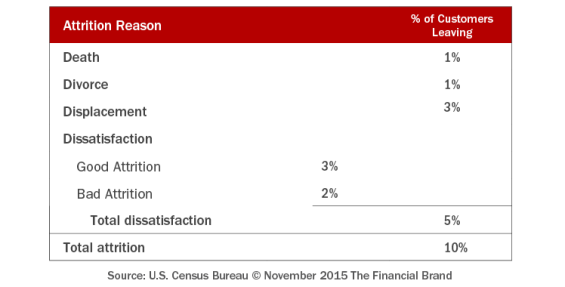

People leave their banks for four reasons – Death, Divorce, Displacement, and Dissatisfaction – the 4 D’s of customer attrition. If we were to assume that a bank’s total customer attrition is 10% per year, here’s how it might look in terms of the 4 D’s.

![Annual_customer_attrition_by_cause[1]](https://thefinancialbrand.com/wp-content/uploads/2015/12/Annual_customer_attrition_by_cause1-565x412.png)

Clearly, there is nothing we can do to stop customers from dying, getting divorced or having to move for work. But there are things we can and should be doing to minimize attrition due to these events. With the 4th D of customer attrition – dissatisfaction – there are clear opportunities for us to improve. Let’s look at the impact of each of the four causes of attrition in more detail and explore opportunities to reduce each.

Death

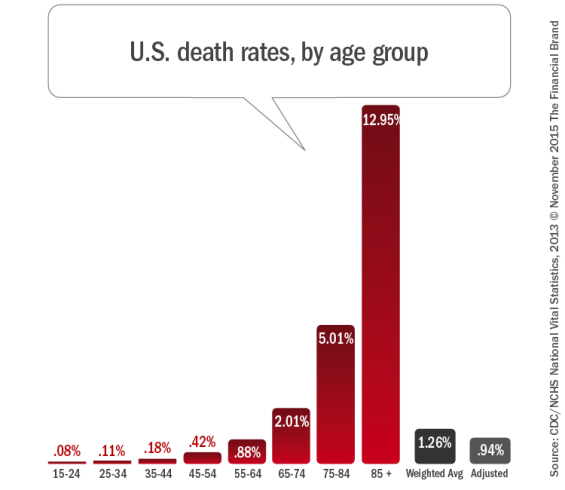

Not surprisingly, annual death rates increase with customer age. If the age distribution of a bank’s customers mirrors the U.S. population, and we adjust for surviving spouses, a reasonable estimate of attrition due to death is just under 1%.

Opportunities: One way to reduce the impact of death on your portfolio is to influence the age distribution of your customer base. For example, CD offers tend to attract older clients while checking offers tend to attract younger ones. Consistently promoting a particular set of products can gradually influence the average age of your customer base.

Another opportunity lies in estate and generational transfer planning. By helping customers know the importance of joint accounts, survivorship rights and payable on death options, you can make it known that survivors will receive VIP treatment if they continue with your bank. Likewise, you could offer beneficiaries and joint accountholders the perks of your best relationship products to incent them to stay after the death of the primary accountholder.

Divorce

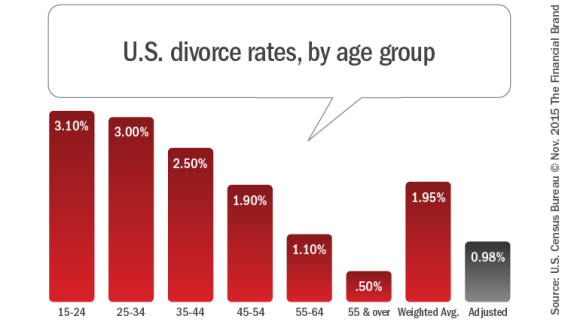

Unlike death rates, annual divorce rates decrease with customer age. Continuing with our assumption for the age distribution of bank customers, the divorce rate is 1.95%. Adjusting for the approximately half of divorcing parties that will stay with their current bank, attrition due to divorce is also about 1%.

Opportunities: One way to stem attrition from divorce is to provide education on account ownership options and to ensure staff members are properly trained. Ideally, you and your customers should understand privacy, account ownership and access rules before and after a divorce.

Where children are involved, ensure that divorcing spouses know their options for protecting college and other savings programs using uniform gift to minor accounts or irrevocable trusts to minimize the impact of attrition from divorce.

Displacement

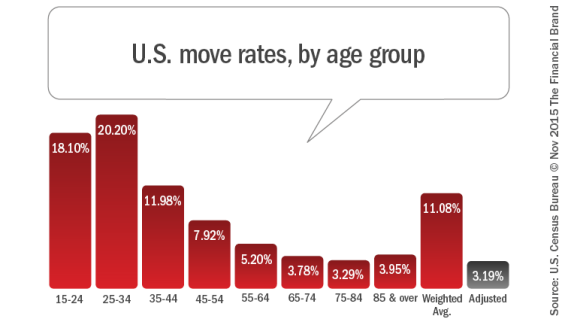

Like divorce rates, move rates decrease with customer age. U.S. move rates indicate that 11% of your customers will move in a given year. Of those, 20% will move within your state, 15% will move out of state. Adjusting for movers who will continue with their current bank in their new location, attrition due to displacement is a little over 3%.

Opportunities: Branch-reliant customers who move to an area where you have no branches will quit your bank and there’s not much you can do about it. But, strong mobile and online banking capabilities will help you keep customers who are comfortable using mobile or online banking even if they move out of your market area. Similar to how people are keeping their mobile phone numbers (regardless of area code) when they move, more people are keeping their bank accounts when the digital tools are strong.

When we combine the impact of Death, Divorce and Displacement, we’ve identified factors that cause 5% of a financial institution’s customers to leave in a given year. Since we started with an assumed total attrition rate of 10%, we can deduce that the remaining 5% attrition is due to dissatisfaction.

Dissatisfaction

Given our reasoning to this point, each year about 5% of customers will become dissatisfied with your organization and leave. It sounds bad, but you’ll actually be happy to see some of these customers leave. Let’s refer to bad customers who leave as “Good Attrition” and good customers who leave as “Bad Attrition”.

Good Attrition

Every month, financial institutions charge off a number of customers’ unpaid overdrafts and fees and close their accounts. In fact, about 40% of account closures are due to charge offs. Usually (but not always), charging off an account results in losing a customer, so we’ll estimate that good attrition at your bank is about 3%.

Bad Attrition

After determining the attrition due to each of the other reasons, we see that, annually, banks lose about 2% of their customers to bad attrition. Customer surveys consistently point to five main dissatisfiers as the causes of bad attrition:

- Poor service quality

- High fees

- Unattractive rates

- Poor products

- Inconvenience.

Let’s make a case for dealing with each of these causes of dissatisfaction.

1. Service Quality

Improving leadership, training, support programs, systems reliability, all have an impact on the quality of service. Improving leadership and developing effective training aren’t necessarily expensive, but IT changes are. Worse, they take time to develop, they are hard to implement and any benefits won’t be found until later on. But, excellent service quality should be every bank’s goal. So get to work on identifying your customers’ specific service pain-points and addressing these shortcomings.

Opportunities: You won’t see immediate results, but your bank should be working on improving service quality.

2. Fees

Reducing a $35 overdraft fee to $30 or even $25 isn’t enough to remove a customer’s pain when they get hit with multiple overdrafts. As far as leniency on fees, it’s not good to pick who will get refunds and who will not. Disparate treatment of customers can get your bank in hot water.

As an industry, we need consistency in the application of overdraft fees and to do our best to help customers manage their balances to avoid overdrafts in the first place. Regulatory scrutiny of overdraft practices is high and changes will come at some point. Until then, this largest source of fee income for most institutions will continue.

With regard to ATM fees, consumers understand that using another bank’s ATM may involve a fee (ATM Surcharge). What they don’t appreciate is also paying a fee to their own bank for using the ATM (foreign ATM fees). Granted, it’s a pain point, but customers don’t appear to be abandoning ship in droves over these convenience fees.

Finally, since monthly account fees are well disclosed up front and ongoing, they are a smaller irritant than overdraft and ATM fees. Plus they are a reliable source of income that banks don’t want to give up.

Opportunities: Unfortunately, while fees are a reason consumers leave a financial institution, dropping any of the above fees (overdraft, ATM or maintenance fees) will reduce your income but provide little attrition benefit.

3. Rates

Large portfolios cannot be re-priced quickly without dramatic impacts on spread revenue. Further, rate management should be part of an overall pricing strategy. Pricing strategies can support acquisition, retention, or profit maximization and in practice, most banks do a little of each.

The balancing act in trying to reduce rate dissatisfaction is to set rates at the lowest level possible that still satisfies customers. There are models to help banks determine what that rate should be. But again, they take time to deploy. Bottom line, any changes to rates have to be well measured because of the potential huge impact on each organization’s bottom line.

Opportunities: While better rates can help slow attrition, they won’t stop it AND they can be very costly. When rates rise, you’ll need good competitive intelligence, data on customer behavior and a demand elasticity model to optimize your response. The goal is to raise rates where they need to be raised and not to change rates where they don’t .

4. Products

Depending on complexity, it takes most financial organizations anywhere from 6 to 18 months to develop and launch a new product. Product and service development should focus on customer need, functionality, reliability and effectiveness. Such focus will help earn more customers AND improve retention at the same time.

Opportunities: Developing excellent products is a critical activity for institutions that want to stay in business. Good products are table stakes to compete in a free and evolving market. You don’t have a choice on this one.

5. Convenience

More branches? More ATMs? Better online banking experience? Better mobile experience? Each of these are components of a higher level of convenience. Unfortunately, improving the convenience of your organization through any of these methods is expensive. Therefore, we must choose our priorities – we need to stay relevant in a changing world BUT we need to protect our valuable customer base.

We won’t get into the changing economics of the branch network here. It’s a hugely strategic issue and it cannot help bad attrition in the short term. The fact is that customers are migrating more and more to digital channels and that is where banks need to focus.

Opportunities: Invest in mobile. Invest in your call center and invest in chat and video customer care capabilities. Maintain a branch network that fits your distribution strategy and retention goals. But don’t expect any of this to reduce attrition significantly in the short term.

Conclusion

About half of a bank’s customer attrition is due to death, divorce and displacement. Banks can reduce the impact of these by promoting specific products, offering relationship benefits to joint accountholders and providing excellent digital banking options.

The remaining half of customer attrition is due to dissatisfaction and is comprised of good attrition and bad attrition. Customers who are part of a bank’s good attrition (about 3% of customers per year) will leave or be pushed out by the bank and, frankly, we aren’t sad to see them go. Valuable customers who leave (about 2% per year) comprise a bank’s bad attrition – a small but important group we hate to lose.

One answer to our original question “how do you retain a customer?” is to focus retention efforts on bad attrition. In addressing bad attrition, we should consider the following:

- There is little evidence that dropping fees impacts bad attrition

- Careful rate management can slow bad attrition but mistakes can be very costly

- Good products are table stakes—developing attractive products is critical

- Branch networks should align with distribution strategy and support retention goals

- Because dissatisfaction is the only ‘D’ we have control over, improving service quality is a strategic imperative. That strategy should support serious investment in mobile banking, digital communication, call center and chat.

Each of these components of attrition and potential solutions need to be carefully evaluated. As you try to protect your customer portfolio, ask yourself a few questions: 1) Do you have the right tools to identify good customers at risk of leaving? 2) Can you reduce or eliminate the irritants or dissatisfiers that chase them away at an acceptable cost? 3) Even if you can prevent some of them from leaving, will it impact your overall attrition enough to make a difference?

Attrition from causes that can be impacted for the customers you want to retain is where your organization’s focus must be. Only with a concerted effort towards improving retention will your organization be able to reverse the loss of customers and their related balances, fees and potential for word of mouth referrals.

Alpine Jennings is a partner for the product and marketing consulting firm, StratAgree and the developer of the COMPASS™ marketing planning system. He helps organizations to better understand customers and markets, build and defend their brand, define product and marketing vision and strategies, and use data and insights to craft marketing programs that connect with customers.

Alpine Jennings is a partner for the product and marketing consulting firm, StratAgree and the developer of the COMPASS™ marketing planning system. He helps organizations to better understand customers and markets, build and defend their brand, define product and marketing vision and strategies, and use data and insights to craft marketing programs that connect with customers.