Non-banking industries like hospitality and travel are deploying futuristic technologies and processes to enhance their service experiences every day — conditioning consumers with higher face-to-face service expectations. When these other industries ‘raise the service bar’, it puts a spotlight on the service shortcomings of increasingly aging branch banking practices.

Innovative approaches to improve branch sales and productivity effectiveness have been implemented across a varied landscape of non-financial organizations as well. Unfortunately, most financial institutions stay in the herd when it comes to technology adoption and process improvement. With a whole world full of great ideas and best practices spread throughout other industries, it’s a series of missed opportunities that banking can’t ignore.

Ten strategies from non-banking industries that financial institutions can consider implementing to improve sales, service and productivity at the branch level include:

- Beacon Technology

- Facial Recognition Software

- Heat Map Technology

- 3D Augmented Reality

- Business Process Management

- Recommended Product Engines

- Highly Trained Staff Deployment

- Tabletop Tablet Solutions

- Preferred Customer Programs

- Appointment Setting Technology

1. Beacon Technology

Target recently rolled-out a new merchandising alert system utilizing beacon technology. Essentially, this sophisticated application relies on smart phones to get targeted messaging to consumers, including product suggestions based on individual purchasing behavior, and/or special coupons aimed at specific demographics when the consumer is in the store.

Notably, the power of the technology is most effective when considering the location of the individual consumer in the store related to targeted products, serving as a personalized notification for the nearby consumer. For example, a young mother walking by a new brand of diapers might get a coupon notification on her phone.

Financial Services Application

Bringing a more personalized service experience to the branch can better educate account holders prior to any face-to-face interactions by sending highly personalized and targeted product and service content through smart phone notifications when they approach the lobby.

Picture a young couple waiting in the lobby to talk with a service representative about a home loan. As they sit down, both of their phones alert them of a new notification containing videos of the benefits of getting a loan through the financial institution they are visiting. The video may contain cross-selling messaging about investment products or car loans as well.

Another application for beacon technology is around alerting account holders who are geographically close to a branch. While this may only be applicable in more urban settings, the power of alerting a nearby account holder of a special limited car loan rate can certainly act as a powerful call to action.

2. Facial Recognition Software

Identifying individuals through sophisticated cameras and facial recognition software has been happening, whether you know it or not, for a number of years. Primarily, facial recognition applications have been used to identify criminals and terrorists, but more practical retail applications, including recognizing your best customers, are at hand.

Financial Services Application

Experienced and tenured branch personnel can be very good at knowing who their best customers are and can act accordingly when these individuals visit the branch. However, relying solely on this human approach can leave gaping holes in the white glove treatment the high-value account holders could benefit from receiving.

Facial recognition software can help identify specific account holders the moment they enter a branch, alerting each employee of their presence and, specifically, of which products they currently do not have with the institution. Armed with this pertinent information, service representives can wow the preferred customer with a personalized greeting and improve the chances of a cross-sell by bringing up products that would be the best fit for them.

3. Heat Map Technology

New heat map technology is helping retailers understand what their shoppers are interested in, helping them optimize the layout of their stores. For example, a clothing store believes their new pink summer dresses will be a big hit with shoppers, so they decide to feature this product in a prime spot towards the front of the store.

After analyzing the heat maps the next day, generated by this new futuristic technology, managers learn that they couldn’t have been more wrong in placing the dresses there. The icy cold colors on the heat map directly in front of the pink dresses alert them of a change they should make ASAP.

Financial Services Application

As transactions continue to decline and branches transform into more sales-centric hubs, new innovative layouts of the branch are becoming a much more viable and critical component towards the success of a location. There is no one perfect design, with variations needed dependent on location and clientele.

For example, some branches are now incorporating business centers and other luxury amenities, like cappuccino machines and large interactive touch pads, into their branch designs. The idea is to improve the service experience to the point where account holders want to come back, again and again.

Using heat map technology, banks and credit unions can gauge how popular these innovative branch amenities are and locations most frequented in the branch. Perhaps a branch shows a red-hot traffic pattern around the large touch screens in the front of the store. After analyzing this data, it might be a good idea to put the screens toward the back of the store to drive foot traffic throughout the branch. Or maybe the cappuccino machine has luke-warm colors in the back of the store; indicating people aren’t finding it back at that location.

4. 3D Augmented Reality

Blending augmented reality technology with the retail shopping experience is the ultimate example of gamification. Augmented reality superimposes a computer-generated image on a user’s view of the real world – typically used with tablets and smartphones. Consumers simply point their device’s camera with their augmented reality app turned on to see 3D graphics pop-out of strategically placed spots in the store.

For example, a young man might see an animated version of his favorite team’s mascot holding a 50% off merchandise sign in one aisle, or a golden coin/token floating by his favorite soda where he can collect loyalty points for prizes in another aisle.

This blend of digital graphics with the real world enhances the shopping experience by making it fun for the consumer to shop.

Financial Services Application

Already utilized by some organizations to locate branches and ATMs, financial institutions can deploy 3D augmented reality in the branches to attract account holders to special offers and/or to spice up learning more about their different products or services.

Imagine a man in his mid-40s waiting in line to deposit a check when he sees a sign advertising the availability of augmented reality capabilities in his banking app. Out of curiosity, he pulls out his smart phone, starts up the app and begins to scan the branch for any 3D graphics. A graphic of a large 3D sports car labeled with a very competitive interest rate fills a space in the lobby, causing him to click on the special rates.

Now, what was a simple visit to the branch to deposit a check has turned into a serious inquiry as the man approaches a service representative with additional questions about the car loan after he deposits the check. Outside the branch office, this technology has been used to display houses that are for sale. By showing the location, price, specs and the monthly cost to own the home, consumers can use their phone or tablet to search all available properties in their price range.

5. Business Process Management

Understanding precisely the processes that take place in a certain situation, analyzing them and then improving upon them with a measured approach is something management has been doing for decades. What is commonly known as the Six Sigma Approach, has now been implemented in the healthcare industry, as a hospital in Canada was able to track sophisticated processes with electronic tracking technologies to improve patient experience and optimize staffing.

Financial Services Application

Some banks and credit unions have already implemented some sort of technology to enhance their account holder experiences at the branch, online or the call center. Additionally, workforce optimization tools can help to schedule the right staff, at the right place, at the right time while also tracking account holders from the moment they arrive at the branch to the time they leave.

6. Recommended Product Engine

Industry leading product recommendation engines by Amazon have changed how consumers interact with cross-selling scenarios. Instead of an untrained retail associate suggesting every product in the store in a data dump manner, Amazon suggests products that best fit consumers based on previous searching and buying behaviors.

This form of personalized marketing is effective at influencing the consumers to purchase items they had no intention of purchasing initially (cross-selling).

Financial Services Application

While practical utilization of ‘smart data’ in the financial services industry can be difficult to implement, the opportunities are almost endless. For example, through predictive analytics, one might develop an algorithm that identifies account holders who have the greatest propensity to open a HELOC. With this database in hand, marketing departments can develop an integrated marketing campaign – including postcards, email blasts and outbound calling – to this targeted HELOC list. Since you are sending less communications out, the cost per marketing touch (i.e. expensive stand-out mail pieces) can be much higher than a typical non-targeted campaign, potentially increasing the response rate dramatically.

Financial institutions can also combine this ‘smart data’ approach with facial recognition technology helping service representatives to know which products to promote to improve cross-sell effectiveness in the branch.

7. Highly Trained Staff Deployment

The concept of Apple’s retail store Genius Bar relies on the public inherently trusting Apple to be able to answer seemingly difficult questions. Aptly named, this concept has been very successful for Apple, leading to increased brand value through deliberate attempts to establish trust, loyalty and expertise.

Financial Services Application

Having the right employees to handle higher-quality interactions is the key to a successful ‘Genius Bar’ concept at a branch. Turning to universal employees or staff that can handle all types of interactions at the branch can be a great place to start. Beyond sales skills, technical skills to assist customers with digital banking skills will help the engagement level of consumers.

Forecasting and measuring staff productivity, especially universal associates, is critical in assuring success with the ‘Genius Bar’ concept.

8. Tabletop Tablet Solutions

Restaurants like Chili’s have rolled out tabletop ordering, entertainment and payment solutions from Ziosk to streamline service and enhance the customer experience. This not only makes the dining experience more enjoyable, but the delivery more accurate and timely.

Financial Services Application

Tablet and interactive devices can be tailored for branch waiting areas where account holders can play games, look up product/service information and take customer service surveys. These can also be used to initiate the amount opening process, entering preliminary personal information to streamline the onboarding experience. The customer wait will seem shorter, they’ll learn more about the financial institution’s offerings, and much needed service data will be collected.

9. Preferred Customer Programs

Preferred customer programs like Hilton Honors, Delta SkyMiles and others are popular in the hospitality and transportation industries, rewarding consumers based on the level of service usage.

Financial Services Application

Financial institutions can also benefit from treating their highest valued account holders with white gloves, especially in the branch. Leveraging an express line, a dedicated account specialist and offering exclusive special offers to these preferred customers can increase service use and loyalty. Using ‘smart data, and beacon technology can assist in these efforts.

This program goes hand-in-hand with a more sales-centric branch where “higher-quality” interactions are more frequent. Would your most profitable account holders visit the branch more often if they received the red carpet treatment every time they came?

Adopting a lobby tracking solution to better track employee sales performance, management can better determine which employees need more targeted coaching around cross-selling.

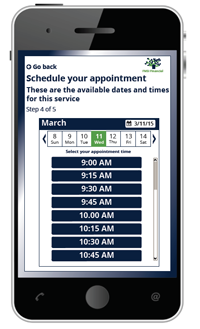

10. Appointment Setting Technology

Some retail stores like Sprint now offer the ability for consumers to set appointments through smartphone applications. As consumers grow accustomed to setting appointments for their retail visits, they’ll expect the same capability from their FI.

Some retail stores like Sprint now offer the ability for consumers to set appointments through smartphone applications. As consumers grow accustomed to setting appointments for their retail visits, they’ll expect the same capability from their FI.

Financial Services Application

A once manual and arduous process deterred banks and credit unions, but new automated appointment scheduling technology developed specifically for financial institutions opens the door to improved customer loyalty and increased sales in the branch. The more sophisticated appointment applications should understand each of your individual employee’s availability and skill sets – making sure to schedule the appointments with the right person at the right time.

Conclusion

Transactions are declining in the branch, requiring a more sales-centric environment to offset the facility costs. Leveraging new innovations from other industries provides a competitive advantage against an increasing array of fintech startups coming down the pike.

Until recently, other industries have deployed futuristic technologies, while the banking industry has remained a late follower. This is no longer an acceptable strategy, as digital consumer expectations are increasing faster than most firms can keep up.

It’s not a stretch imagining many ‘deposit-centric’ branches closing in the next decade due to a lack of technology adoption. What technologies will you implement in the coming years to prevent this from happening at your branches?