For three years running, EverFi and Higher One have conducted extensive research into the financial attitudes, knowledge and behaviors of college students. For their 2015 study, they surveyed approximately 43,000 college students at two- and four-year institutions across the America. Their survey probed issues related to banking, savings, credit cards and school loans. The data uncovers alarming trends in the levels of stress students face in regards to student loans and money management.

The results of the survey show that Millennial students’ attitudes about money “displayed more materialism, more compulsion, less caution and less aversion to debt as time spent on campus increased.” They are also less likely to pay their credit card bill on time, follow a budget, or save money.

These younger Millennial consumers are taking out more and larger student loans, yet report feeling less financially prepared to deal with them. Only 58% of students from four-year institutions say they feel prepared to manage their money. Three out of five don’t use budgets. 17% say they don’t even manage their money; their parents do it for them. 16% say they lived paycheck to paycheck, and yet only three-quarters stop spending when their bank account balances were low.

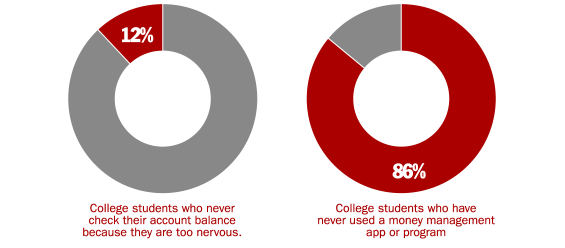

Surprisingly, results showed that even as young adults are increasingly connected to digital devices, only 14% of students report having used any form of money management app to keep track of finances.

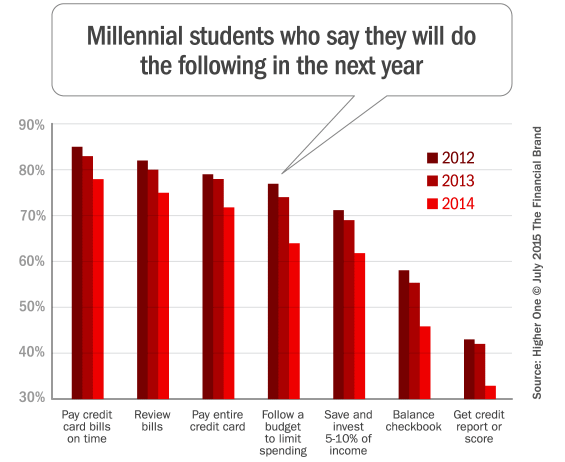

Over the course of the three-year study, results indicate that incoming freshmen have become less likely to engage in responsible fiscal behaviors. Significantly fewer say they that in the next year they plan to follow a budget, pay credit card bills on time, review bills for mistakes, save and invest, check their credit score, use a debit card vs. credit card for everyday expenses, balance their checkbooks every month, and buy only the things they need.

When Learning Financial Lessons, Real World Experience Pays

To expand the breadth of the study insights, they survey added a sample of approximately 1,000 students at two-year community colleges. The results reveal that two-year college students are smarter about money than those in four-year universities. For instance, community college students are more likely to curb spending when their resources are low, and to use budgets.

While 62% of four-year students say they check their account balances, 83% of community college students said they do so. And 60% of two-year students say they use budgets, compared with 39% of four-year students.

Two-year students were four times less likely to have their money managed by their parents (translation: they are figuring out their finances on their own). Students attending junior colleges are also twice as likely to keep their receipts, reflecting the more intimate and engaged relationship they have with their money.

Community college students are (somewhat unsurprisingly) more likely to have multiple credit cards/higher outstanding balances and more likely to worry about financial issues than students at four-year institutions.

“Community college is a less-expensive alternative, but those attending probably working and trying to make ends meet, so they are worried about trying to pay for school and be able to earn their degree,” says Mary Johnson, VP of financial literacy at Higher One. “Students attending four year schools might be a little younger, and maybe in a different frame of mind.”

The financial realities facing students at two-year schools almost certainly explain why they exhibit greater acumen when it comes to managing their money. Many of them had to save up for a few years before attending, so the average age of students at two-year schools tends to be older, giving them more time and opportunity to gain experience in financial matters. They also often have jobs and other responsibilities outside of school.

“Students that choose to come to a two-year school right out of high school really understand how much tuition and fees are going to be, and they are trying to save money,” says Ashleigh Lewis, chair of the financial literacy committee at Tyler Junior College.

Schools? Parents? Who’s to Blame?

Johnson at Higher One says the study really underscores the need for more personal finance education, specifically before students even get to college. According to Higher One’s study, students who took a financial literacy course in high school were 10 percentage points more likely to report being prepared to manage money in college than those who did not report any previous financial literacy education. Yet only 17 states require any financial literacy education for high school graduates, and only six test them on it, the report indicates. Only six — Colorado, Delaware, Georgia, Michigan, Missouri and Texas — require students to pass a financial management test for graduation.

John Hoffmire, with the Wisconsin School of Business at UW-Madison, says most college students learn life’s harder financial lessons the hard way: “It is much more common for students to start to learn financial literacy through an embarrassing rejection of their card at a restaurant on a date, a loan denial when they go to buy their first car, or an intimidating letter that comes in the mail notifying them of their delinquency.”

Phil Schuman, director of Indiana University’s financial literacy program, keenly observes that most college students never dealt with thousands of dollars at any point in their life. The sheer magnitude of dollars involved with credit cards, auto loans and student loans can give young consumers a “Monopoly Money” effect, where the numbers get so big that they aren’t perceived as real. “You sign the dotted line and all this money floods to you and helps you fund your education,” he says. “But students don’t really understand what paying that back will mean.”

Tom Arnold, professor of finance at the University of Richmond, says the results of the Higher One survey are disappointing, but not unexpected, because —according to Arnold — the problem with financial literacy starts at home. He says teenagers traditionally rely on their parents for financial guidance and support, so they haven’t been forced into making any real financial decisions. “Consequently, prior to college, many students do not have to budget their money nor be concerned about paying off debt,” he points out.

Arnold said teaching kids about managing money is similar to eating right — it’s easy to ignore until it becomes a problem.

Gary Herman, president of the non-profit ConsolidatedCredit.org, agrees that America’s institutions — both educational and financial — have failed at preparing young consumers for the important money matters they’ll face. “It’s amazing that our educational system prepares young adults for math, reading, science, sex education and more,” he says. “But it doesn’t prepare them for the one thing that they’ll be forced to make life-changing decisions on — money.”

Herman stresses the important role parents play in their kids’ financial lives. “Parents need to have ‘the talk’ about finances. Most talk with their kids about the birds and the bees, and let’s face it, that’s uncomfortable. But when it comes to money? Mostly silence.”

For America’s youth, there is clearly a knowledge vacuum when it comes to financial literacy. Are financial institutions willing to step into the role that parents traditionally filled, and take over for educational systems that seem to struggle imparting financial wisdom? Who will teach kids about loans, interest rates (APR vs. APY), credit cards, insurance, and building budgets? And why stop there? Why not expand the curriculum to include everything kids need to learn — how to buy groceries, cook nutritious and well-balanced meals, doing laundry, basic home maintenance, how to change a tire or your oil filter?

Tom Davidson, founder and CEO of EverFi, offers advice to organizations deploying a financial literacy program. “Financial education should focus on providing personalized, interactive, mobile-friendly learning experiences that allow students to practice good financial decision-making in a safe environment.”

You can download a full copy of Money Matters on Campus report, as well as an infographic summarizing this year’s key findings, at the Higher One website.