An IBM report showed the distinct and complementary way consumers use their digital devices for retail spending. Smartphones drove 31% of total online traffic, nearly two and a half times that of tablets. While smartphones drove the traffic, more purchases were completed on tablets. Tablet sales accounted for 13% of total online sales, whereas smartphones only accounted for 9%.

This consumer behavior is called multi-screening. There are two primary types of multi-screening behavior: sequential screening, where consumers move between devices, and simultaneous screening, where multiple devices are used at the same time. Because the use of multiple screens makes the digital consumer feel more efficient, it is a behavior that is likely to increase as the universe of digital devices grows.

Omnichannel, a word making regular appearances at FinTech conferences and in the financial services industry media, originated in the retail industry. For retailers, it describes a strategy for leveraging the purchase cycle by providing shoppers with a consistent, intuitive user experience across the various digital devices they use when they purchase goods and services online or in a physical store. Some retailers are very good at this. Some are not.

Financial institutions now find themselves faced with the same challenges as retailers: the customers and members they serve expect to use all of their digital devices to address their financial needs. And, just as they do when they shop, consumers are moving between devices when they do their banking.

Determining how to provide a fluid, consistent user experience from laptop to tablet to smartphone may be the single most important goal for financial institutions if they want to compete successfully for the long term.

There are three specific lessons that banks and credit unions can learn from the retailing industry.

Read More: Amazon’s Dilemma – A Cautionary Tale for NeoBanks

1. Consolidating Digital Channels

In the eight years since the iPhone was introduced, digital devices have proliferated at a historic rate. Tablets were adopted more quickly than smartphones, and wearables are now being used not only to help consumers with their fitness regime, but also to purchase goods at the point-of-sale.

Smart televisions that are directly connected to the Internet are common in many households, and car manufacturers are offering Internet enabled vehicles. To date, financial institutions have responded to the growing number of devices that their customers wish to use by constructing solution silos for each device.

Not many banks or credit unions believe this approach is sustainable in the long term due to the rising cost and complexity it creates. In addition, the existing legacy systems in place at most banks and credit unions are not flexible enough to adapt to a future where the Internet of Things (IoT) may bring us.

Lastly, statistics – such as those from a recent study by Chase – indicate that consumers do not move to new digital access points abandoning those previously used. In fact, they continue to use the various digital devices at their disposal according to their particular needs at the time. Device use will not converge, so a means of consolidating the disparate channels deployed for each device is required.

Optimizing and personalizing the growing number of digital channels requires new systems with new architectures. Single code base solutions that can utilize APIs provide a foundation for consolidating existing digital channels. In addition, highly configurable solutions with customizable templates are a necessity. As the retail industry found out years ago, financial organizations can’t be held captive by inflexible products that require three months (or longer) to change product promotions, logos, colors or disclosure statements.

A single code base that leverages the power of APIs positions institutions for present and future digital access points. With these attributes, banks and credit unions can deliver a consistent user experience to any digital device and ensure that customers are not confused by changing interface as they move between devices.

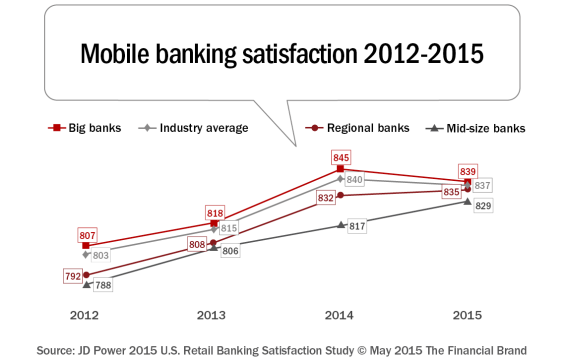

As many retailers have found during the most important buying seasons, even a little confusion can cause consumers to abandon the buying process, and an inconsistent user experience over time can drive them to find another financial provider. In fact, recent statistics from a JD Power study are indicators of user fatigue created by poor and inconsistent user experiences created by disparate, legacy systems and the antiquated practice of single sign on access to third party providers.

Young FinTech start-ups starting from scratch have the advantage of building for this digital infrastructure. However, these start-ups and early stage providers need to prove scalability, reliability and sustainability to get past the risk adverse CIOs who often are the gatekeepers for institutions considering new products.

As has happened with smaller or slow to adapt retailers, some banks and credit unions may consider the capabilities and agility of newcomers to the digital space too significant to overcome. This is understandable, but those institutions that wish to be competitive in the ever-evolving digital arena will realize that the real risk lies in doing business as usual.

Organizations should look at the management teams and boards of those organizations who have already succeeded in the digital space for seasoned professionals with a history of delivering complex, high profile solutions to financial institutions of their size.

2. Optimizing Digital Context

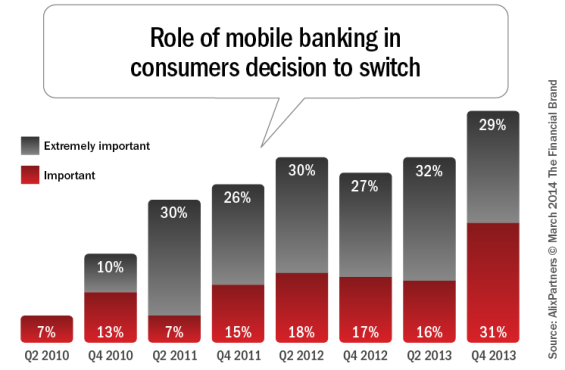

The influence of digital access points on the decision by consumers to switch financial institutions continues to grow in importance. It makes a “business as usual” approach the most significant risk an institution can take in responding to the digital needs of customers.

According to the Accenture 2014 North American Consumer Digital Banking survey, more than one in four customers would likely consider a branchless digital bank. In addition, nearly three-quarters of US customers – two-thirds in Canada – consider their banking relationship “merely transactional.”

To move beyond a ‘single transaction’ relationship, retailing has found that it is important to better understand the consumer buying behavior and to provide contextual solutions that will meet needs proactively. The same is true in the banking industry.

“The digital consumer is saying, ‘know me, understand me, reward me.'”

The digital consumer wants their banking partner to understand and react to their needs. They are saying, “Know me … Understand me … Reward me.” Even though the Baby Boomer generation is becoming more comfortable daily with using digital devices to bank, pay and network with family and friends, there is another generation rising that will even more dramatically accent the importance of optimizing digital context for all organizations, especially banks and credit unions.

In the U.S., Millennials represent more than $200 billion in annual buying power. As their net worth grows, this number will continue to rise steadily each year. More and more Millennials will be financing cars, buying homes, opening investment accounts and creating college funds for their children.

They are highly connected with an always-on mentality. According to the Accenture study, 94% are active users of online banking and 72% are active users of mobile banking. Thirty-nine percent would consider using a branchless digital bank, compared to just 16% for those over 55.

They also want help managing their finances. Sixty-seven percent want a financial institution that will help them create and monitor a budget; compared to 31% of Boomers. They expect their bank or credit union to be helpful in other ways as well. For example, 58% are interested in their financial institution proactively recommending products or services. Baby Boomers agree on this point, with 46% also wanting that kind of assistance.

These statistics suggest that an institution that wants to use digital channels to maximize its competitive advantage will need to do more than achieve a consistent user experience across all digital access points. They must rethink how they deliver existing digital services making them simpler and more intuitive to use.

For example, to give Millennials and Boomers the help they want with their finances means rethinking the whole area of personal financial management (PFM). The initial hype around PFM has largely faded, and most of the PFM services offered by banks and credit unions in the U.S. are stand alone solutions from third parties that present as a “tab” within the digital banking experience.

Consumers must not only go through enrollment, but many systems require them to spend time building budgets, reclassifying transactions and setting goals. With Millennials asking specifically for assistance with finances, institutions hoping to attract this segment must completely rethink how they provide financial assistance.

Specifically, PFM must be so integral to the digital banking experience that it is not seen as a separate service at all. When a user enrolls in digital banking, transactions for the last 90 days should be categorized and a budget automatically created with comparative charting to show trends. No additional enrollment should be required and every digital user’s transactions are analyzed.

If the financial institution uses aggregation, this view can include accounts and transactions from sources outside the bank or credit union, too. Categorization engines must achieve high levels of accuracy for this approach to work (95% or more) and the flexibility must exist for the customer to customize categorization, budgets and goals.

Retailing also discovered that contextual offerings (like those done by Amazon and others) can’t come with greater complexity and friction. The banking industry is no different, needing to proactively offer services and providing financial counsel and support to the consumer with a clean design, fewer keystrokes and simplification.

3. Personalizing the Digital Buying Experience

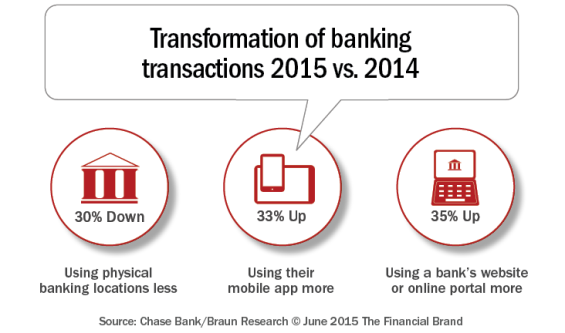

As has occurred in the retailing industry, traffic to physical facilities is down and digital use is up at financial institutions. However, there is much debate over the supposition that such a trend means that branchless banking is just around the corner.

To some, the argument for keeping branches open seems to be backward facing, to a time long gone when most consumers had to make a personal visit to their financial institution to make deposits, open accounts and send money. Why hang onto branches when all those services and more can be completed on digital devices?

Winners in the retail industry have responded by providing a highly personalized digital shopping experience. Personalizing digital banking is also heavily dependent on providing consumers with a customized experience that replicates (and improves on) what was once offered by the branch employee.

But, there are a significant number of consumers who are so young as to have hardly ever darkened the door of a branch. They are comparing the digital experience they have with their financial institutions not only with other banks and credit unions, but with other organizations they encounter online, especially in the retailing industry.

Unfortunately for many financial institutions, the best they can do is “customize” a digital user experience based on macro level demographic data. Too many count their display of generic banner ads based on this macro data as “up-selling and cross-selling.” This is assuming any sales messages are provided at all.

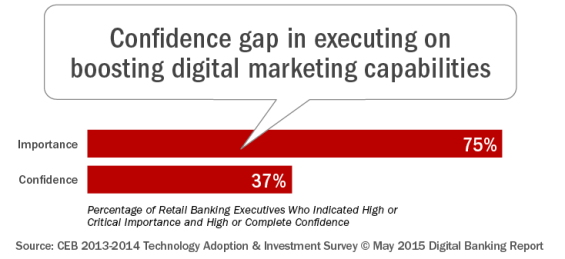

This is not Amazon-like in the least, and most executives in financial services have shown this lack of confidence relative to their digital marketing capabilities.

The personalization required to deliver an Amazon-like banking experience that differentiates and monetizes a financial institution’s digital buying process requires data. The specific data they need to personalize the experience is typically either isolated in the disparate systems serving the various channels they deliver services through, or it is in the hands of the third parties they outsource certain customer facing services to. Without easy access and the ability to analyze (and apply) this data, creating an Amazon-like banking experience is extremely difficult to do.

Some banks and credit unions may undertake core conversions or seek new CRM systems to address this need for data, but neither of those alone will give them what they need to personalize and then monetize digital channels. Without a consolidated, integrated (360 degree) view of the consumer’s digital activities across all devices, institutions will likely run the risk of doing more harm than good by posting irrelevant offers that cause the consumer to question how well they know their clients.

In addition, deciding to renew a core or upgrade a CRM system represents a strategy that underestimates how quickly the digital landscape is changing. By the time the financial institutions involved in such projects finished them, the fight for the digital consumers’ loyalty could largely be over.

“The ‘digital genie’ can not be put back in the bottle, no matter how some may wish to make it so.”

There are other options to consider. There is a financial institution in the U.S. that is currently completing a project designed to monetize their digital channels based on easy access to and analysis of customer data. Instead of beginning with large and complex backend systems, they decided to start to migrate their digital channels onto a single code base built upon a data analytics engine.

In addition, they are deploying an approach to areas such as money movement and PFM that reinforces this focus on data. In both instances they retain control of data that provides them with a comprehensive, up to date view of every activity of each digital user within their digital channel.

As has happened in the retailing industry, more forward thinking institutions will begin their journeys down the digital integration path as well. Others will follow these innovative organizations, as the challenge of consolidating, optimizing and monetizing digital channels will only continue to grow.

Those banks and credit unions that do not move beyond business as usual to embrace scalable, reliable, and modern options may not be found on the financial services landscape of the future. As was found out by Blockbuster, Borders, Circuit City and many other retailers, the ‘digital genie’ can not be put back in the bottle, no matter how some may wish to make it so.