Not long ago, consumers were conditioned to make sacrifices. In any product category, they were accustomed to choosing between speed, quality, price and service; they would have to settle for only one or two of those things. That’s not the case any more.

Banking consumers in North America say they want it all: deals, discounts, convenience, relevance and a seamless, multi-channel experience balancing both digital and face-to-face interactions. Consumers may be willing to share their personal data with financial institutions, but only if they get what they want in return.

These findings come from an Accenture study encompassing over 4,000 consumers in the United States and Canada. Results from this multi-year research covering consumer banking attitudes and behaviors show that consumers are laser-focused on the value (or lack thereof) that they receive from their banking providers.

“Differentiation based on price or products and services is a zero-sum game for banks,” says Accenture. “They get trapped in an endless loop of one-upping and matching each other on discounts and product offers where no one wins. Brands ultimately become interchangeable in customers’ eyes.”

The way out, according to Accenture, is to compete on service — to provide superior service consistently across channels. “While some customers will always be driven by the deal, others are willing to pay for better service and ease of doing business. For example, consumers who applied for a loan in the past year said they would pay more if they received end-to-end customer service through the loan process. Delivering banking value means mastering the delicate balance between the tangible and intangible, the savings and the service.”

Robo-Advice Is Welcomed

In the Accenture study, consumers said they are intrigued by computer-generated advice. This style of “robo-advice” automates recommendations and suggestions (think: “next best product”) with insights based on profiles built from digital banking behaviors, questionnaires and advanced algorithms. Robo-advisors have already gained significant traction in the wealth management industry, but Accenture says this trend is also picking up in retail banking, creating an opportunity for banks to deliver additional value — and connect with — new customers.

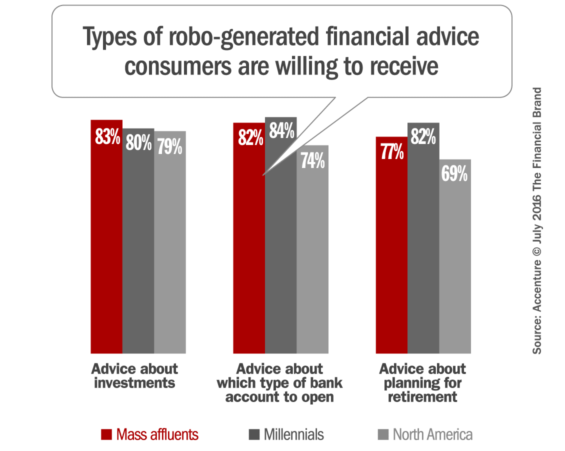

A surprising 46% of consumers are willing to bank using robo-advice. Consumers welcome robo-advice from banks to determine how to allocate investments (79%), the type of bank account to open (74%) and for retirement planning (69%).

“Consumers will continue to dictate how, when and where they want to interact, and banks have an opportunity to use intelligent automation and robotics to simplify and improve the customer experience,” explains David Edmondson, Senior Managing Director of Accenture’s North America Banking practice. “Successful banks will strike the right balance between human and machine interaction to elevate their role in customers’ lives beyond simple transactions and become a go-to resource.”

Branches Still Relevant

“The branch will remain relevant because it is the place where consumers can connect with their banks’ human advisors.”

— Accenture

Findings from the study indicate that “digital banking” is not an all-or-nothing proposition. While online banking remains the dominant channel in terms of both in terms of frequency of use and preference, the survey found that the branch remains popular. Consumers may be receptive to robo-advice and self-service/digital channels, but they also crave face-to-face human interaction.

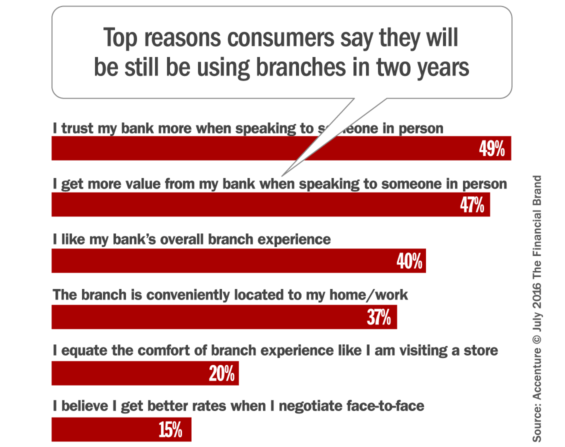

One-quarter of respondents in the Accenture study say they use a branch at least weekly, and it remains the second most preferred channel, after online. 61% of those who use branches say they prefer the “full service” model. The vast majority (87%) of consumers, including 86% of Millennials, report that they will continue using branches in the future.

Accenture says consumers’ appetite for an integrated omni-channel experience — one that blends digital and physical — makes sense: “It signals just how pragmatic consumers are today. To get the value they want, consumers do not always choose the same channel. Instead, they make channel choices based on their specific banking needs at the time.”

Consumers Will Dump Banks That Don’t Deliver

Consumers say that if their increased demands aren’t met, they have no problem switching to another institution. It might sound like little more than sabre rattling, but this isn’t an empty threat. Banks and credit unions can’t count on inertia to save them any more. In the past, switching banks was considered such an onerous chore that only the most irate consumers would pull the trigger.

But switching banking providers today isn’t as difficult as it once was. 11% of North American consumers left their bank in the past year — up one percentage point from Accenture’s 2015 survey — and consumer perceptions that “switching is hard” have eased substantially since 2013 (the first year of the survey). Fewer consumers say that “the difficulty of the process” will keep them from making a switch.

The survey found that consumers are increasingly willing to bank with non-traditional players, if that’s what it takes. One-fourth of consumers in the U.S. say they would consider switching to a bank with no branch locations, up three percentage points from last year. Among Canadians, 23% would consider switching to a branchless bank, up eight percentage points from last year. Across North America, 26% of Millennials would consider switching to a branchless bank (up three percentage points from last year), and 34% of mass affluent consumers would do so, up ten percentage points from 2015.

Among those who have already switched, 33% said they chose a non-traditional provider (online-only bank, payments provider, retailer, etc.), versus 23% who switched to a large regional or national bank. Of those who switched, 15% of consumers ages 55+ joined an online-only bank, up from only 5% who did the same last year. Millennial switchers increased the move to online-only or payments providers from 24% in 2015 to 27% this year. Consumers ages 35-54 had a reverse trend; 30% moved to online-only or payments providers in 2015, down to 24% in 2016.

Discounts & Deals Trump Privacy Concerns

Nearly one-fourth (23%) of respondents have experienced at least one incident of their financial data being hacked online over the past two years, including 25% in the U.S. and only 16% in Canada. Yet, despite this, consumers are willing to share their data in order to receive better service from their bank.

Nearly two thirds (63%) of respondents are willing to give their banks direct access to personal information, such as mortgage, credit card and student loan data, so their bank can use it to present them with suitable products and services. Respondents want banks to use their data to provide access to lower prices, faster service (such as rapid loan approval), more relevant advice, and personalized offers based on location.

What Can Banks & Credit Unions Do?

To deliver banking customer experiences that provide new value, Accenture says retail banking providers must do things differently… and do different things.

1. Win the data game. Data is the currency of customer insight. Retail banks are clamoring for it. Banks must refine data collection, preserve customers’ data privacy and digital trust, support insight- driven banking innovation, and develop predictive analytics skills.

2. Reinvent loyalty. Real-time, personalized interactions can cultivate loyalty. Digital marketing platforms can capture customers’ implicit and explicit intent through triggers such as key word searches, social interaction and transaction indicators, so banks can connect in ways that matter.

3. Be relentless about service. Banks cannot afford to take their eye off of superior customer service. It must become part of the bank’s genetic code, from the business strategy to the day-to-day culture. Service must be consistent and continually refined based on customer feedback.

4. Explore new roles. Banks can provide more value to customers by becoming a go-to resource for how they live, rather than being a pure financial utility. There are several roles to play—from brokering partner services to providing an open platform for buyers and sellers to interact.

5. Master “physical” + “digital experiences. Developing banking channels in isolation from one another is risky. Customers want seamless “phygital” experiences that blend physical and digital, and few banks are meeting their demands. Minimizing channel conflict will help banks stand out

“Today’s consumers expect their service providers to understand and anticipate their needs and offer a seamless experience across digital and physical channels,” concludes Edmondson with Accenture. “They expect this as much from their bank as they do from retail stores and internet giants.”