Today’s consumers are more connected than ever. Thanks to the technology advancement of digital devices, they now have more access to- and deeper engagement with financial services content and brands. Consumer ownership of digital technology continues to grow exponentially. A typical US consumer has six different devices connected at any given time. As a consequence, digital activities have become increasingly mobile, as consumers have ditched personal computers at home for tablets and smartphones.

The changing landscape is forcing retail institutions to interact with, acquire and grow relationships in new ways. Unlike in the past, the combination of technology and data today enables retail financial institutions to engage — at scale — with relevant, addressable messages that truly reflect the consumer’s financial situation, needs, preferences and behaviors.

To maximize on this opportunity to expand and optimize reach in the digital age, banks and credit unions must do the following:

1. Target and acquire consumers using traditional and non-traditional media and channels in the most efficient manner. Millennials are now the largest demographic in the U.S. The shift in demographics and usage of multiple devices provides a dramatic, exaggerated increase in how non-traditional channels are accessed for service and advertising… and how often. Financial marketers will be shifting budgets from traditional channels to digital.

2.Understand and act upon channel usage that impacts buying and servicing behavior. Improve the targeting of online media, and capture leads across the purchase funnel — from research to conversion. Reduce the clunkiness of the online account opening process to shift branch preference.

3. Integrate attribution and measurement capabilities across multiple media and channels. Invest in updating antiquated IT systems built for processing account data that are not conducive to omni-channel marketing. Focus on the ability to present the right message in the right channel at the right time. A consolidated customer view across all touch points provides a foundation for effective measurement will be necessary.

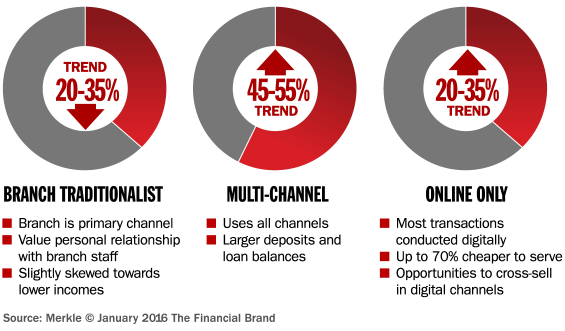

Technology is changing consumers’ behaviors when it comes to how they research and shop for financial solutions. Shopping in digital channels is now critical in at least half of the new primary bank relationships that are acquired today. Consumers with more experience making banking product choices are more likely to prefer online to branch interactions, while branches remain relevant for those consumers who possess less banking knowledge or product familiarity. Younger, digitally-oriented consumers tend to rely both on recommendations from friends and visits to branches more than other segments. Shifting demographics and channel usage patterns are also creating new segments that will be primarily engaged in digital- and non-traditional channels.

This growing number of newly-definable market segments present a real opportunity for retail institutions to expand from their traditional branch-centric approach to a much more nimble and responsive digital model. Marketing case studies from top retail banks targeting digital consumers have yielded the following results:

1. Digital Consumer Shift – Expanded distance to branch via digital extension. Approximately 2X lift from responders out of footprint.

2. Consumer Preference – Reach new younger audiences via media preference. Approximately 25% lift from responders < 40.

3. Affluence – Reach higher and varied household income via media preference. Approximately 50% lift from responders with income > $100k.

To expand and optimize the reach when targeting these new market segments, retail banks and credit unions must respond rapidly. Acquiring and servicing digital consumers means financial marketers must embrace critical new capabilities:

- Build common definitions for customers and audience segments

- Develop an integrated strategy and plan across the customer lifecycle

- Coordinate experience delivery on owned- and third-party channels

- Measure and attribute, tying back to offline activities

- Implement ongoing evaluation and optimization with increased frequency

Retooling for retail bank growth in the Digital Age will require a massive refocus on honing skill sets, intellectual property, experience, technology and data. It will require capabilities for inbound- and outbound engagement, and consolidation of the customer view among traditional and non-traditional media and channels. Great risk in terms of lost market share exists for those retail institutions who do not cultivate the new capabilities necessary today. To retain market share and accelerate growth, partnerships with solution providers will become increasingly important. You’ll need to rely on experts outside your organization more and more if you want to keep pace.

Despite all the challenges, retail institutions possess some innate competitive advantages that will help them prevail in the Digital Age. Retail banking providers have the ability to leverage a combination of technology and (big) data for improved addressable consumer interactions. That means more powerful marketing based on a deeper understanding of customer value that maximizes interactions… that is, for those institutions willing and able to embrace the opportunity.