As consumers, particularly young adults, turn to digital services and tools for their financial needs, traditional banks are increasingly vulnerable. Major banking organizations are well aware of their fintech competition and have invested heavily in the companies that are trying to disrupt the finance and banking industries through digital innovation, simplicity of design and advanced pricing models.

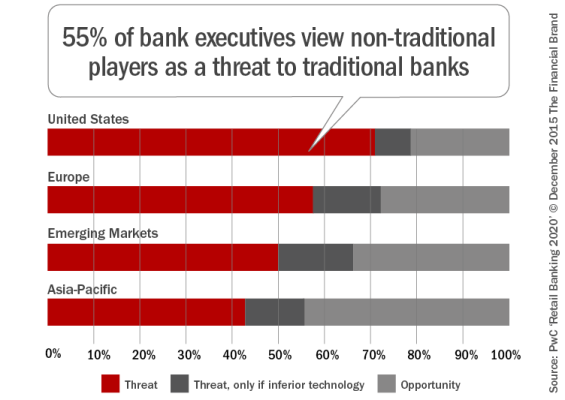

We’ve seen this occur with big players like JPMorgan and their investment in the popular mobile payments platform, Square, back in 2011. Just last year Wells Fargo launched a fintech accelerator program to coach young startups. However, in contrast to the public actions and investments that banks are taking when it comes to fintech companies, research conducted by PwC found that over half of senior retail banking executives view non-traditional financial services providers as a threat to traditional banks.

To better position themselves for the future, banks need to address three hurdles standing in the way of bank innovation:

- The rigidity of hierarchical organization

- An increasingly out-of-touch culture

- The ever-widening technology gap.

So, let’s take a deeper dive into why these are major obstacles and how banks can overcome these challenges.

Organization and Management

One of the biggest barriers to innovation in banking lies at the foundation of how traditional firms are built. Banks have a relatively rigid organizational structure of associates, analysts, various managers, directors, vice presidents and so on. Ideas easily get lost or forgotten in this complex chain of command. Simply put, a hierarchical management structure hinders creativity, agility and flexibility – all drivers of innovation.

Just recently, Deutsche Bank undertook significant changes including shuttering its presence in 10 counties, halving their investment banking customers and modernizing their technology which was outdated and disparate. As innovation almost always affects the revenue and performance of a business or product line within a bank, it needs to sit at the top of the agenda of the CEO and senior management.

Successful startup and technology companies often pride themselves on having flat organizational structures where communication between junior members and managers is often faster and more actionable. Instead of a purely top-down approach, fintech startups are open to more collaborative brainstorming – resulting in more ideas where employees feel empowered to suggest ideas and bring them to fruition.

Attitude and Culture

Innovation requires a culture of short cycle failures and improvement iterations, which have to be learned and accepted. These methodologies go against the typical long term planning found in banks.

Like startups, banks have to learn to “fail fast and fail often” without putting trillions of dollars at stake. There are inherent risks when constantly trying novel ideas especially since 90 percent of startups fail. Traditional banks do not have to entirely abandon their workplace culture, but need to make the environment appealing and stimulating to attract skilled workers who can reimagine the possibilities and capabilities of the industry.

Innovation requires a change in attitude from what the banks want to offer to what customers really need. This seems pretty obvious, but it is especially difficult to create in large revenue-oriented organizations. One additional reason American banking organizations are out of touch with their customers is that the demographics of banking executives has stayed relatively stagnant while customer profiles have changed significantly in recent decades.

Banks should actively seek to understand what customers are concerned about and develop solutions to address what customers are looking for. Incentivizing consumers for honest feedback with perks and deals can go a long way in fostering a better relationship.

Technology and Skills

Technology has evolved tremendously in the past 10 years, and big banking organizations have struggled to incorporate new features at scale with the required agility needed in a fast-paced environment. Banking technology systems are currently full of complex applications with redundant functionalities and limited connectivity. This makes it very difficult for banks to incorporate the product demands and tastes of millennial users in the necessary time to market.

Efficient real-time banking systems, with powerful middleware able to make the products and services accessible across internal channels (mobile, web, branches, ATMs) and third parties, are specifically difficult and costly to implement for banks. To do so requires a complete reengineering of current systems.

There is added difficulty because development and maintenance of current systems has been mostly outsourced and banks have trouble attracting skilled engineers, UX designers and agile trained technology workers due to competition from Silicon Valley. Over the last eight years, the percentage of Chicago MBAs working for technology firms has doubled from 6 percent to 12 percent. At Stanford, the number is close to a third. As mentioned by Chris Skinner in his Financial Services Club blog, banks must aggressively attract top technology talent to make new ideas a working reality.

While they might not be privy to the specifics of why banks are falling behind in technological innovation, many digital-first consumers are under the impression that fintech firms can offer better services, at a better price, than traditional banks and credit unions. This sentiment seems to be shared especially by high value customers.

According to a recent survey by Fintonic, one in five Americans who earn more than $80,000 a year believe technology companies such as Apple and Google could do a better job at banking transactions and customer service revealing trouble ahead for the future of traditional banks. As banks continue to fall behind in offering convenient products and services that complement the increasingly mobile and technology-driven world, consumer interest will erode as they turn to other options.

Future Options for Banking Innovation

Financial institutions are under immense pressure to evolve and usher in new technologies to make banking a more user-friendly and efficient experience. But the strategies that spur innovation cannot be introduced overnight. Rather, banks must commit time and financial resources to upgrade technology, hire talented workers, build a degree of flexibility into management and diversify.

Given the aforementioned challenges, banks should consider strategic acquisitions and partnerships with promising and successful fintech startups. By integrating innovative entities that are being created to meet the demands of the marketplace, banking institutions can more quickly meet the changing needs of their customers in new regions and in more ways.

How a bank approaches innovation will be the difference in whether it will flourish or struggle in comparison to their fintech competitors.