Today’s technology offers consumers access to more insight and choices than ever thought possible even five years ago. As a result, today’s consumer is more informed and more demanding of organizations they plan to do business with.

In financial services, new digital fintech start-ups, benefiting from lower barriers to entry, are offering solutions that are responding to these needs before many legacy banks can respond. Globally, entrepreneurs and even traditional banks are creating digital-only banks or neobanks that embrace a digital-first strategy.

Simple, Moven, BankMobile, Number26, Atom, ZenBanx and NuBank are just some of the firms testing the waters. These neobanks have digital technology at the core of their value proposition. Opportunities exist for existing organizations that can leverage the new technologies to engage an increasingly demand consumer in close to real-time, but legacy challenges are difficult to overcome.

In the white paper, Designing a Sustainable Digital Bank, IBM makes it clear that a great mobile app does not make a bank a ‘digital bank. Neither does closing branches. According to IBM, “A true digital bank is built on the value proposition that most products and services are delivered digitally. Its customers expect to use digital channels for their day-to-day banking activities. The digital bank’s infrastructure is optimized for real-time digital interactions and its culture embraces the rapid change of digital technologies.”

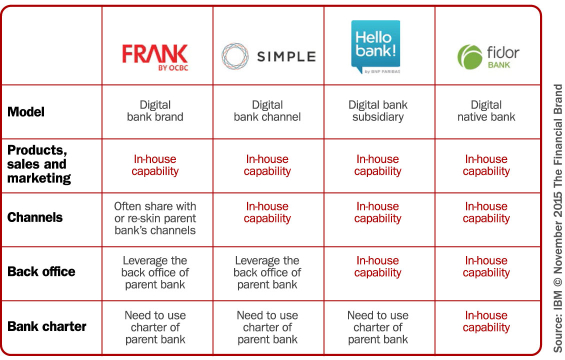

Digital Banking Models

In the IBM white paper, they divided the digital banking playing field into four banking models.

Model A – Digital Bank Brand. Legacy full-service banks are constantly trying to appeal to NextGen millennials who want a brand that is more digital and meets their unique needs. Rather than alienating existing customers, these banks establish a new brand with a unique value proposition and products designed to the younger segment. These digital banks usually leverage current infrastructure. Examples of this model are FRANK by OCBC in Singapore and LKXA of CaixaBank in Spain.

Model B – Digital Bank Channel. Unlike Model A digital banks, Model B organizations build a banking organization focused on an improved user experience. These firms usually use an existing banking organization’s back office and banking license, reselling insured products with an enhanced user interface. Examples of this model are Simple and Moven in the US.

Model C – Digital Bank Subsidiary. This model combines a differentiated digital user experience with a true end-to-end business model. Larger banks may find that existing back-office systems are too rigid and siloed to power a digital bank, while other organizations may believe the current silos and processes won’t support a digital bank model. Model C digital banks establish a completely separate organization, with more agile and modular back end systems to provide a better consumer experience. Examples of this model include Hello Bank by BNP Paribas.

Model D – Digital Native Bank. These banks build their entire value propositions around digital technologies. Digital native banking does not necessarily imply branchless banking. However, customers of these banks are expected to interact with the bank primarily through digital channels. Examples of this model are Fidor Bank of Germany and Tangerine of Canada.

Digital Banking Success Factors

A critical success factor for any of the models described is the ability to achieve economies of scale. Fintech start-ups that lack an already well-known brand and the reach of a legacy banking organization will struggle with success since new customer acquisition in an industry with a foundation of trust is very difficult.

The second most important success factor for a digital banking organization is the ability to design the right experience for target customers. According to the IBM white paper, “There is no shortage of direct banks – some started by entrepreneurs and others backed by major traditional banks – that have failed to take off due to low customer adoption.”

The third success factor noted in the IBM report is the ability to expand beyond basic deposit products into more complex products and fee-based income opportunities. Some of these products are more complex and difficult to sell in a completely digital model.

As is becoming more clear as the legacy banking organizations compete head-to-head with fintech start-ups, traditional banking organizations have the advantage of scale, brand, reputation and an existing branch network. That said, scale and legacy systems/mentality also can result in an inability to innovate and respond to market changes in an agile manner.

Designing a Sustainable Digital Bank

According to IBM, “Sustainable digital banks optimize customer interactions, products, processes and data around digital technologies. They are appealing on the front-end and digitally efficient on the back-end, taking advantage of mobile and digital technologies to lower customer service and enhance higher touch services. Designing a digital bank requires optimizing interactions, products, processes, insights and the organizational culture.”

Sustainable digital banking organizations will need to excel at both by providing the convenience of digital channels when convenience is needed, and engage with customers contextually and on a 1:1 basis when a personal touch is desired. To achieve this, IBM recommends optimizing each of the following five areas.

Digitally Optimized Interactions: Banks need to provide the basic transactional services through digital channels. Where services are more complex or require a personal touch, digital technologies should facilitate these interactions. The key will be to provide the best mix of digital convenience and digital enhanced personal touch.

Digitally Optimized Products: A digital bank’s products need to be easily purchased and serviced on digital channels. According to IBM, the following questions should be asked during the product development process:

- How do consumer first hear about the product?

- Where do consumers conduct research?

- Is it possible to purchase the products digitally?

- Can after-sale services be conducted digitally?

- How can issues and questions be resolved?

Digitally Optimized Processes: Most current back office systems are not equipped to provide an end-to-end view of the customer journey beyond digital interactions. This can start by digitizing user signatures and current paper documentation requirements. The goal is to eliminate the paper and human interaction as much as possible, moving these process to a digital platform,

Digitally Optimized Insights: Collecting enhanced consumer insights, banks can deliver contextual solutions that are highly personal. They want their financial institution to “Know me”, “Look out for me”, and “Reward me” in real-time. With this level of engagement, banks and credit unions can provide differentiating banking experiences and solutions … delivering the right product at the right time through the appropriate channel.

Digitally Optimized Organization: Probably the most difficult challenge in becoming a ‘digital bank’ is transforming the legacy culture and organization. A fintech start-up is more agile in adapting to ever-changing customer behaviors. This is why many legacy banking organizations create a subsidiary with new teams and fresh minds when starting a digital brand.

Next Steps

Moving to any of the digital banking models is much more than just a branding exercise or the replacement of branch offices with a mobile and online banking platform. The transformation requires the facilitation of face-to-face intimacy through digital interactions and adding digital convenience to basic transactions.

According to IBM, “Digital banking requires a deep transformation of the entire banking organization including the digitization of processes and extraction of insights from data. Even the bank’s strategy, business model and mindset should become more digitally oriented. Those that are most adept at harnessing digital technologies can become industry leaders.”

New technologies, fintech competitors, shifts in consumer expectations represent both challenges and opportunities for existing banking organizations. Those organizations who don’t move quickly may be left behind. The good news is that many of the digital solutions that have been introduced in the past few years could represent partnering opportunities as well as ways to reduce back office expenses.