Seems like everywhere you turn, someone is bashing banks for something. They’re not innovative enough, their customer service is lousy, or they’re the scourge of the earth and the single root cause of all of society’s ills (OK, so that’s just one man’s views).

I heard about a study that fintech vendor Pega conducted from tweets suggesting banks’ customer service capabilities were lacking and in need of improvement.

After seeing the results, I didn’t come to the same conclusion. In fact–based on the data–I concluded that not only is bank customer service just fine, but that banks have no need to innovate, and no reason to mention the word “omnichannel” ever again.

What Service Factors are Important to Banking Consumers?

According to the study, the three most important service factors are 1) Listening to and understanding my needs; 2) A representative with a courteous, patient and/or friendly attitude; and 3) Responding to inquiries in a timely/responsive fashion.

I took away three findings from this chart:

- Omnichannel is dead. Just 17% of consumers listed “consistent service regardless of channel” in their top three list, and 13% cited “multiple ways to contact.” So much for all that omnichannel nonsense, eh?

- Personalization can go away. Less than one in 10 consumers said “personalized service that knows my recent buying history and activities” was one of the three most important factors. In fact, when asked how much interaction they wanted with (or from) their bank, just one in four said “I’d like lots of proactive interaction from my bank with a personalized service.” So you may now completely ignore all those consultants preaching the importance of personalization.

- The real most important factor is missing. The answer that I would have given as the service factor that mattered the most wasn’t even on the list: Fixing the damn problem. I’ll take a rude rep who fixes the problem over a friendly clueless one, any day.

How Important is Customer Service?

It probably won’t come as much of a surprise to find out that customer service is an important consideration influencing consumers’ decisions to switch banks. It might, however, come as a surprise to find out that customer service isn’t a particularly important consideration influencing consumers’ decisions to switch banks.

Maybe I should explain.

When Pega asked consumers how big a factor customer service is when considering switching banks, one-third said it is the top factor, and half said it is an important factor.

However, when asked what would be the most likely cause of switching, only 13% said customer service issues. If you can explain the discrepancy, please do.

Oh, by the way, did you notice towards the bottom of the list in the chart above, that just 6% of consumers said that “innovative products and offerings” would cause them to switch banks?

I guess that’s bad news for all those fintech startups claiming to have more innovative products and services. The good news for them is that they apparently don’t have to worry about providing great customer service.

How Good is Bank Customer Service?

Overall, it appears banks’ customer service is pretty darn good. When asked what were the three things that annoyed them most about their bank’s customer service, just one in ten said “fails to listen to or understand my needs.”

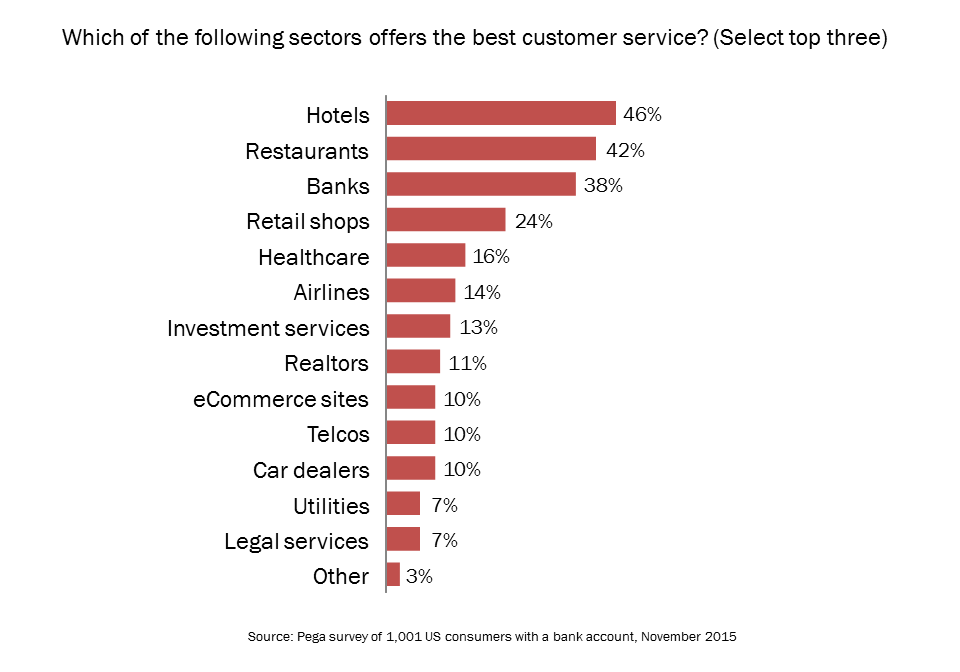

And how shabby could banks’ customer service be if consumers voted banks third in a ranking of industries’ level of customer service?

The Confused State of Bank Customer Service

What should the banking industry do about its customer service capabilities?

I don’t know. The data in the Pega study suggests that the answer is “do nothing.”

Of course, I’m sure I could find other studies that refute everything listed here about omnichannelness, personalcustomization, and innovativosity (you can see why I came up with Shevlin’s Law: For every data point you can find to support your point, I can find two to refute it).

Perhaps a better conclusion is this: We shouldn’t take consumers’ survey answers at face value.~