Now more than ever, banking needs to step out of its collective comfort zone, digitizing and diversifying in response to the changing consumer. While branches aren’t vanishing as quickly as some predicted, banking can no longer follow branch-centric models. Instead, the ‘Bank of the Future’ represents an omni-channel, client-centric, self-directed digital model that many banking executives admit may be beyond their scope.

A report from Oracle surveyed more than 100 executives at major retail banking institutions globally, which revealed a desire amongst banks to invest in digital strategies … but also stark differences in progress.

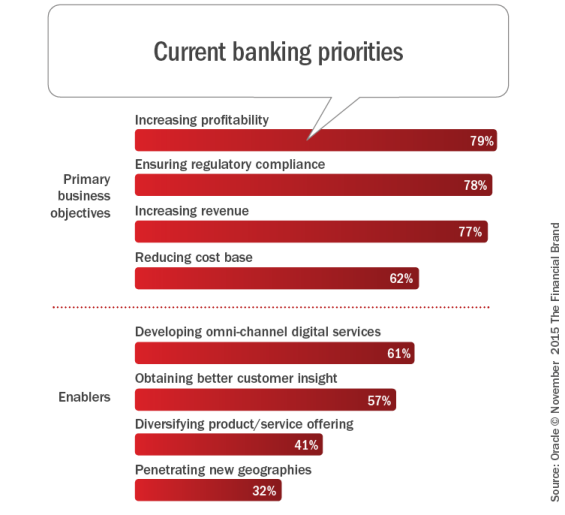

According to the report, digitization of the entire banking organization is viewed as the primary enabler of banks’ business objectives. Regardless of whether the focus is increasing revenues or profitability, decreasing costs or meeting regulatory guidelines, digitization is seen as a central investment priority.

Overall, 94% of banking executives interviewed say that having a digitized omni-channel customer engagement strategy is important to their future success, with 37% admitting that future success of their business is ‘entirely dependent’ on digital customer engagements. Despite the recognition that digital technology initiatives are urgently needed, 88% told Oracle they see significant challenges in moving toward digitization.

The Fintech Challenge

Every publication talks about the transformation of banking and that today’s retail banking competitive landscape is far removed from what existed a decade ago. Much of this change has been highlighted by the rising influence of new digital competitors that are impacting all levels of banking.

“No longer do retail banks simply vie for customers against other retail banks. Instead, we are witnessing an influx of new, tech-savvy, digital competitors – FinTechs – all eager for a piece of this lucrative financial pie,” the report said.

The foundation of these changes is caused by changing consumer demographics and expectations. “The world’s largest demographic, born after 1980, are now millennials. These customers have grown up in the era of Facebook and Amazon; an era of instant communication, one-click purchases and 24 hour delivery. If a supplier can’t provide a service, they don’t wait – they find someone else who can,” says the report.

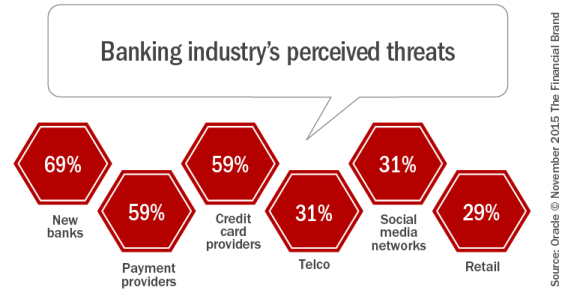

More than half believe that both private label banks, alternative payment providers and even credit card providers will be major competitive threats – a greater percentage than are worried about other traditional high street players.

The Digital Delivery Gap

The banking industry is not standing still as these changes in expectation and competitors occur. Most organizations recognize that digital customer engagement is the way to respond to the changes in the industry. Key services that are among the most important to adopt, as noted by the respondents in the report, include mobile payments and real time data synchronization, spend analytics and even digital advisory services.

Despite all being recognized as important by over 80% of banks, there appears to be a failure to commit to delivery of these services, with only 24% providing real-time synchronization, 19% providing location-driven services and only 30% currently providing real-time analytics. In other words, the gap between importance and ‘ability to deliver’ is more than 60% for three of these capabilities. And while the importance of providing mobile payments is viewed as the most important component of digital engagement, the gap in capabilities is still 50%.

Oracle believes one of the reasons for the lag in delivery of digital capabilities is the comfort of current relationships. While these relationships served banking well in the past, banking needs to change their underlying processes to accept these new forms of data specially in the content of real-time digital processing.

“Omni-channel customer engagement is not a ‘bolt-on’ product that can simply be added to existing systems to give a little bit more functionality”, says the study. “It needs to take a fresh perspective – wiping the established ‘offline’ board clean and asking ‘how should we be doing this in a digital world’?”

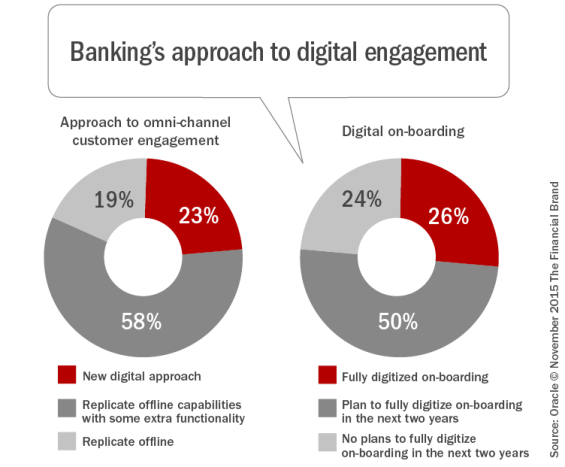

Unfortunately, only 23% are currently approaching omni-channel customer engagement with a fresh, digital mindset. Instead, a ‘bolt-on’ approach is how the majority of retail banks (77%) are approaching digital channel engagement, either replicating offline banking capabilities online, or adding a small amount of additional functionality. Change is happening however.

For instance, while 74% of banking organizations aren’t yet able to facilitate the digital on-boarding of customers currently, within the next two years this figure is expected to drop to 24%.

Challenge to Digitalization

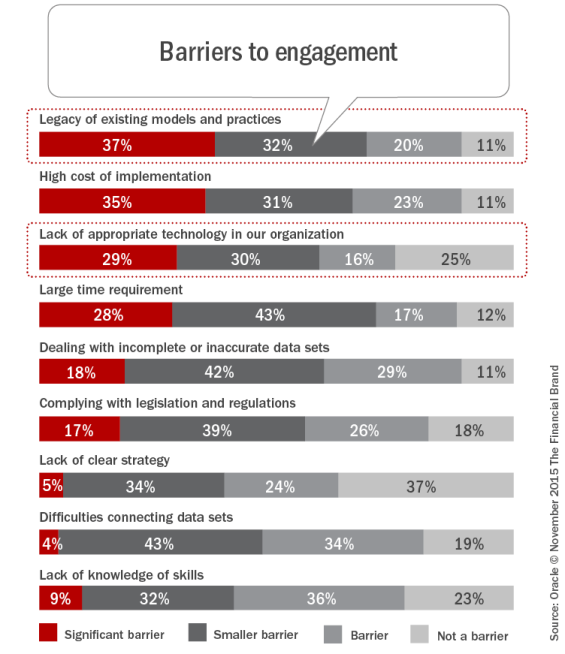

Why are so many banks yet to develop a real-time, digital customer engagement offering when there is an acknowledgment of the importance of this capability? The key challenge lies in legacy systems, with nearly all banks (89%) mentioning the challenge of overcoming their legacy systems as a barrier against omni-channel engagement. The high cost of implementation (89%) and lack of suitable technology (75%) were also seen as hindering efforts to become truly digitized.

Beyond the innovation and investment needed to change legacy systems, Oracle blames the banking industry’s defensive mindsets, with banks focusing on preventing customer defection, complying with legislation and reducing the cost base, rather than actively seeking growth and improvement. Currently, retention of customers is prioritized above revenue as the key impetus to digitization, with 83% claiming customer loss as a prime motivator.

Is Delivering the ‘Bank of the Future’ Possible?

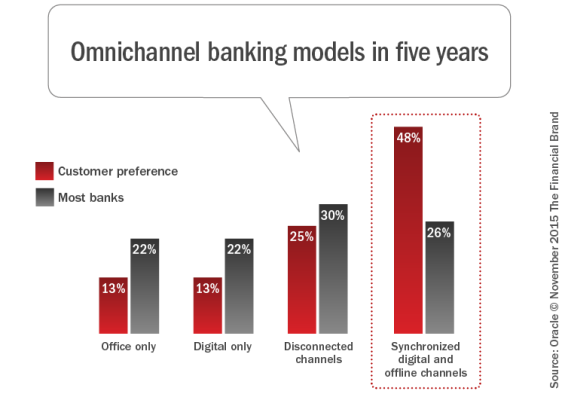

The banking model for the future will be customer-centric as opposed to being driven by products and services. This model will enable an information-driven and value centric relationship as opposed to being based on the bank’s needs. While 48% of the banks believe that customers in the future will want to use a bank where tasks can be completed in real-time across multiple synchronized digital and offline channels, there is only a limited belief that the industry will be able to live up to this challenge.

Nearly one third believe that most banks will be operating with disconnected digital channels in five years with 22% believing that most banks will have failed to adopt digital at all. The discrepancy between what banks think customers’ will want, and what the market will be able to deliver, is greatest in North America and the European markets, but no more than one third of banks in any region believe that banking will be able to provide truly synchronized, digital omnichannel banking within five years.

According to Oracle, “Failing to meet customers’ expectations is dangerous in any industry; it could be lethal in an environment where the competitive landscape is becoming ever-more congested.” While there is clarity of what is expected by the consumer, there is definitely less assuredness if banking will be able to keep pace with expectations given the level of investment and commitment required.