Despite a significant financial recovery from the global banking crisis, the banking industry faces decreasing margins and increasing competitive threats as fintech start-ups are positioned to steal lucrative retail and business customers, according to a report by McKinsey & Company. The report states that, “As digitization accelerates, banks will be in a battle for the customer that will define the industry for the next 10 years.”

McKinsey expects stable returns, with margins declining as interest rates remain low, competition intensifies and new fintech firms start to undermine banking’s economics. The ongoing digital revolution and growing regulation will have a significant impact on banking economics and business models.

According to McKinsey, “Driven by technology, non-banks, fintech firms, other more established tech companies and shadow banks are disrupting banks’ relationships with their customers and posing a significant threat to revenues.”

The Battle for the Digital Consumer

The digital revolution is impacting all industries, including banking. It is impacting the way consumers access their products, how products and services are delivered and purchased, and the underpinnings of the entire financial marketplace.

McKinsey research has found that consumers are willing to try fully digital product propositions for deposit and credit cards, with more than half saying they would switch banks if a fully digital provider made an attractive offer. While actual switching may not reach that level (due to massive friction and consumer lethargy), the interest is definitely there for ‘digital natives’.

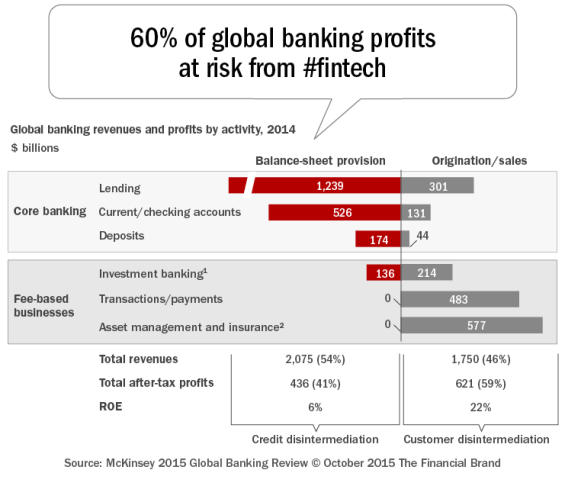

The chart from McKinsey below illustrates the economics of the basic banking business model. Fifty-nine percent of profits come from origination, sales and distribution of services with a 22% ROE.

McKinsey believes most new entrants are targeting the origination and sales components of banking, and estimate that in five major retail banking businesses – consumer finance, mortgages, lending to small and medium-sized enterprises (SME), retail payments and wealth management – from 10% to 40% of bank revenues will be at risk by 2025. Consequently, between 20% and 60% of profits from these businesses will be at risk, with consumer finance expected to be the most vulnerable line of business.

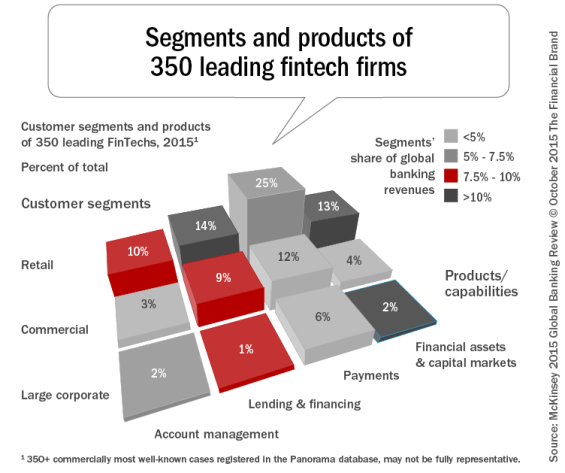

As shown below, the infiltration of fintech firms in different product categories is significant, especially in payments. The incentive for both start-ups and established technology companies is enormous, as capturing even a tiny fraction of the $1-trillion profit pool can mean a fortune to owners and investors.

While most (if not all) of these firms don’t want to become banks – with the associated compliance burden, they do want to gain scale by leveraging the customer relationship and related value. For traditional banking, the new competition has an upper hand since most are usually providing a better contextual customer experience, lower costs … or both.

The impact on banks’ economics will be widespread. Some tactical repricing may be possible, but over the long term, business models must change radically to reach a much lower CIR than banks have today.

Fintech Weaknesses

While it may look like the digital version of the wild, wild west for fintech firms, there are several challenges that could stand in the way of growth. The most important of these could be in the area of compliance and regulation. For the time being, most regulators have accepted the moderate amount of risk that has been associated with the new entrants. That could change as scalability increases and the industry is further disrupted.

Privacy and security is another critical factor that could negatively impact the influx of fintech firms. As more banking revenues move to digital, a big online breach could send consumers back to the same organizations they left, where security is more of a constant.

Finally, the long-term economics of the fintech sector has been untested during periods of rising interest rates, increased risk and a reduction in investment dollars. There is no doubt the fintech sector is white hot right now, but will the bubble burst if returns evaporate or default rates increase?

Banking’s Response

The banking industry is in a battle unlike any before. The best run banks continue to do well, but there are significantly more weaker institutions. To improve and sustain performance, banks and credit unions must embrace digital technology across the organization.

To win the battle against new entrants, financial institutions must mirror the traits of fintech firms, leveraging proprietary data to deliver personalized contextual consumer experiences. They must lower costs and be bible enough to respond to changing consumer expectations.

New start-ups and established innovative players are selectively separating customer segments from incumbents, hindering banks’ ability to cross-sell, stranding loss-leader businesses like basic lending. Even where fintech firms do not succeed in stealing customers, they are forcing banks to lower their prices, reducing already thin margins.

Banks need to capitalize fully on their biggest advantages – data and access to the customer – while also rebuilding trust. Banks that embrace the digital transformation can find success, holding off attackers with one hand and less nimble incumbents with the other.

The other option is to retreat, becoming specialists at the basic businesses of deposit warehousing and financing, allowing others to expand relationships. According to McKinsey, the window for making this choice is narrowing; banks must decide soon, probably within three years, or the choice will be made for them.

In the mean time, in order to compete effectively for the customer relationship against newcomers, the McKinsey report says banks must re-imagine the customer relationship and integrate digital approaches deeply into the bank. Specifically, banks need to:

- Shift their culture to embrace innovation and changing customer expectations

- Revamp their brands to build an emotional connection with the customer

- Re-imagine the customer experience so that it reflects and supports the new brand positioning

- Build digital at scale.

The stakes are high, according to McKinsey: “Those that do not seek to transform may well become somewhat digitized, but will likely be stuck in the middle – outwardly modern, inwardly struggling, and moving slowly toward extinction.”

Please Note: McKinsey does not advertise on The Financial Brand, and no compensation nor consideration was given to publish this story or provide the download link.